If you’re do dementia sufferers have to pay care home fees, the answer is yes. Many dementia sufferers do have to pay care home fees in the UK, because dementia care is usually classified as social care rather than medical care. This means the cost of a dementia care home is typically assessed through a financial (means) test carried out by the local authority.

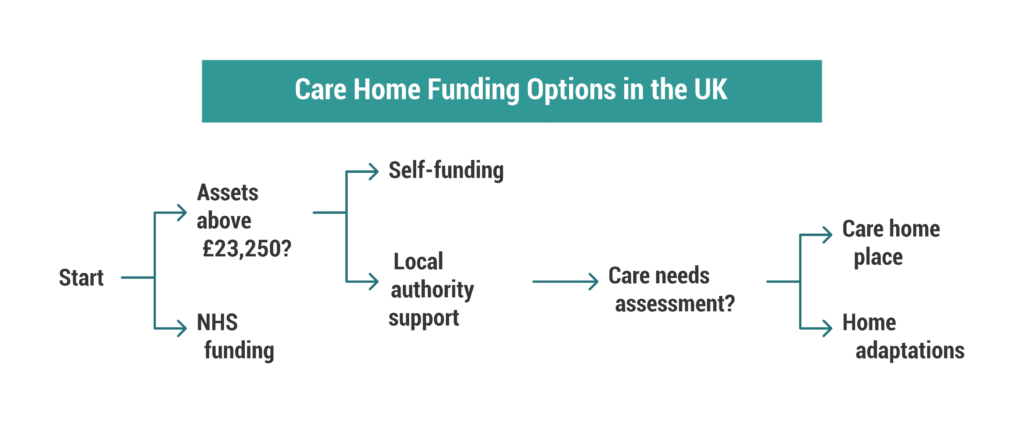

If a person’s savings, income, or assets exceed certain thresholds, they usually have to pay for their own care home fees, either fully or partly. In England, for example, people with more than £23,250 in assets are generally expected to fund their own care.

However, some people with dementia may receive financial support or fully funded care, depending on their circumstances.

Key points families should know:

- Self-funding is common. Many families pay privately for dementia care homes when savings or property exceed the means-test threshold.

- Local authorities may contribute. If assets fall below the upper threshold, the council may help with care home fees.

- NHS Continuing Healthcare (CHC) may cover the full cost of care if the person’s needs are primarily medical rather than social.

- NHS-Funded Nursing Care (FNC) may pay a weekly contribution if the person lives in a nursing home and needs care from registered nurses.

Because of these rules, dementia care home costs in the UK vary widely. Some families pay the full price of long-term care, while others receive partial or full funding depending on their financial situation and health needs.

Understanding how the system works is the first step toward finding help with care home fees for dementia patients and planning the right level of support.

Why dementia care home costs in the UK are often high

Many families feel shocked when they first see dementia care home costs in the UK. Unlike standard residential care, dementia care requires specialist support, higher staffing levels, and a secure environment, all of which increase the overall cost of care homes.

People living with dementia often need help throughout the day and night. Care teams support residents with memory loss, confusion, mobility problems, and changes in behaviour. As the condition progresses, care homes may provide enhanced dementia care, which includes:

- 24-hour supervision and support

- Staff trained specifically in dementia care

- Secure layouts to prevent wandering

- Structured routines and therapeutic activities

- Specialist nursing care for complex health needs

These additional services make dementia care homes more resource-intensive than many other forms of residential care.

Location also plays a major role in the cost of an old people’s home. Care homes in cities or areas with higher staffing costs often charge significantly more than homes in rural regions. Facilities that provide specialist dementia units, private rooms, or advanced medical care may also charge higher fees.

For caregivers searching online for dementia care homes near me or a care home for dementia near me, the price can vary dramatically depending on the level of support required. Families often discover that dementia care involves not just accommodation but round-the-clock professional care, which is why the price of long-term care can feel overwhelming at first.

Understanding these factors helps families prepare for the financial side of dementia care and explore available funding options before making long-term decisions.

READ MORE: What Is a Care Needs Assessment? (England Guide for Families and Caregivers)

How much are dementia care home costs in the UK?

The cost of care homes for dementia in the UK varies widely depending on the type of care, the location, and the level of support required. However, most families can expect dementia care to cost more than standard residential care, because specialist support and supervision are often needed.

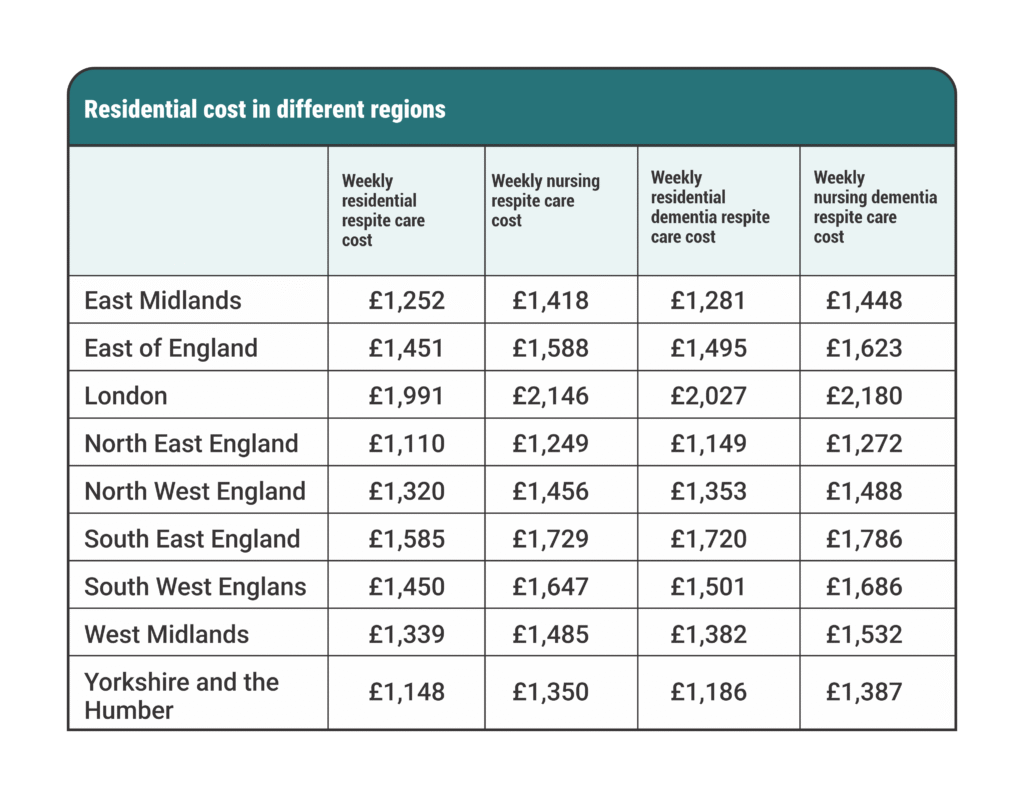

On average, weekly dementia care home costs in the UK are approximately:

- Residential dementia care: around £1,200 – £1,500 per week

- Nursing dementia care: around £1,400 – £1,700 per week

These figures represent the typical price of long-term care, but the final cost depends on several factors.

What affects the cost of care homes?

Several factors influence how much families pay for care home fees, including:

- Location: Care homes in London and major cities often charge more than those in smaller towns.

- Level of care required: Residents who need specialist nursing or behavioural support may face higher costs.

- Facilities and services: Private rooms, specialist dementia units, and enhanced dementia care programs can increase fees.

- Availability of care homes: In some areas, limited supply means higher prices.

For families searching online for “dementia care homes near me”, prices can vary significantly even within the same region. Some homes focus on standard residential support, while others offer specialist dementia care homes with trained staff and secure environments designed specifically for memory conditions.

Because of these variations, the cost of an old people’s home or dementia care home can differ greatly from one provider to another. This is why many families first research local options before deciding whether to fund care privately or apply for financial support.

Who pays dementia care home fees in the UK?

In most cases, who pays care home fees depends on a financial (means) assessment carried out by the local authority. This assessment looks at the person’s income, savings, and assets to determine whether they must pay for their care themselves or qualify for financial support.

Many people with dementia end up paying some or all of their care home fees, particularly if they have savings or property above the government thresholds.

The financial assessment explained

Before funding any care placement, the local council will usually complete two assessments:

- Needs assessment – Determines what type of care the person requires (home care, residential care, or nursing care).

- Financial assessment – Calculates how much the person should contribute toward the cost of care homes.

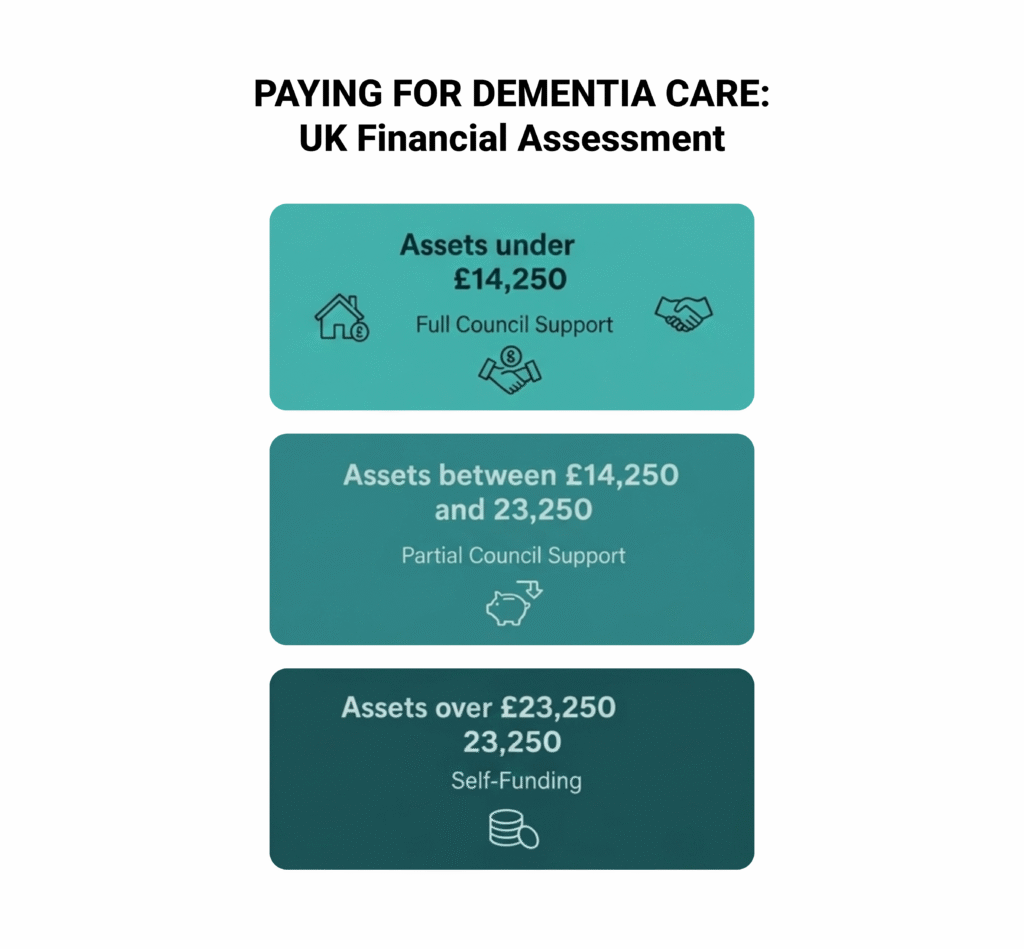

In England, the main capital limits currently work as follows:

- Over £23,250 in assets: The person normally pays the full dementia care home costs UK privately (self-funding).

- Between £14,250 and £23,250: The person contributes toward care costs, and the local authority may help pay the rest.

- Below £14,250: The local authority usually covers most care costs, although income such as pensions may still contribute.

Assets considered in the financial assessment can include:

- Savings and investments

- Property (in some cases)

- Pensions or regular income

However, the value of a home may not always be included in the assessment. For example, if a spouse or dependent relative still lives in the property, the council may disregard its value.

Local authority funding for care

If someone qualifies financially and meets eligibility criteria, the council may provide local authority funding for care in your own home or help cover the cost of a residential placement.

Families often start researching how to get help with care home fees once they understand the outcome of the financial assessment. The council may either arrange the placement directly or provide a personal budget to support the person’s care needs.

Understanding how the financial assessment works can help families plan ahead and explore the options available for help with care home fees for dementia patients.

SEE ALSO: Attendance Allowance Pitfalls (2026): Best Guide to Claim AA Successfully

Is there free care home funding for dementia patients?

Many families ask whether there is free care home funding for dementia patients in the UK. In most situations, dementia care is not automatically free, because the system treats it primarily as social care rather than healthcare. However, some people with dementia may qualify for funding that covers part or all of their care home fees.

Two NHS funding routes can help reduce dementia care home costs in the UK.

NHS Continuing Healthcare (CHC)

NHS Continuing Healthcare is a package of care fully funded by the NHS. If someone qualifies, the NHS pays the full cost of care, including accommodation and nursing support in a care home.

Eligibility does not depend on savings or assets. Instead, assessors decide whether the person has a “primary health need.” This means their care needs mainly involve medical supervision rather than personal support.

Some people with advanced dementia qualify for CHC when they experience complex needs such as:

- Severe cognitive impairment

- High levels of behavioural distress

- Complex mobility problems

- Significant medical supervision needs

Although families sometimes assume dementia automatically qualifies for CHC, this is not always the case. Each person must go through a detailed assessment conducted by healthcare professionals.

For those who meet the criteria, CHC effectively provides free care for dementia patients in the UK, because the NHS covers the full cost of care.

NHS-Funded Nursing Care (FNC)

If someone lives in a nursing home but does not qualify for CHC, they may still receive NHS-Funded Nursing Care.

Under this scheme, the NHS pays a weekly contribution toward the nursing element of care. The payment goes directly to the care home and helps reduce the overall care home fees families must pay.

FNC does not cover accommodation or personal care costs, but it can still provide meaningful financial support for people living in specialist dementia care homes that require registered nursing staff.

Understanding these funding options helps families determine whether they can access help with care home fees for dementia patients, particularly when dementia progresses, and care needs become more complex.

Are next of kin responsible for care home fees?

Many families worry that they might personally inherit the care home fees of a loved one with dementia. In most cases, next of kin are not legally responsible for paying care home fees.

The person receiving care usually remains responsible for their own dementia care home costs in the UK. Local authorities or the NHS may contribute depending on the outcome of the needs and financial assessments, but family members do not automatically become liable for the bill.

However, there are a few situations where a relative may agree to pay part of the cost.

When families may contribute to care home fees

A family member may become financially involved if they choose to:

- Sign a contract with the care home agreeing to pay part of the fees

- Provide a third-party top-up payment if they select a more expensive home than the local authority normally funds

- Manage finances on behalf of the person through Lasting Power of Attorney

For example, if a council agrees to fund care up to a certain amount but the family prefers a more expensive care home for dementia near me, they may choose to pay the difference as a top-up.

What families should understand

In most cases:

- Next of kin are not automatically responsible for care home fees.

- The financial assessment focuses on the assets and income of the person receiving care.

- Families should carefully review any agreements before signing documents with a care home.

Understanding this distinction can reduce anxiety for caregivers who already face emotional and practical challenges when supporting someone living with dementia.

MORE: Council Care Cost Inheritance: Who Pays for Care Home Fees 2026?

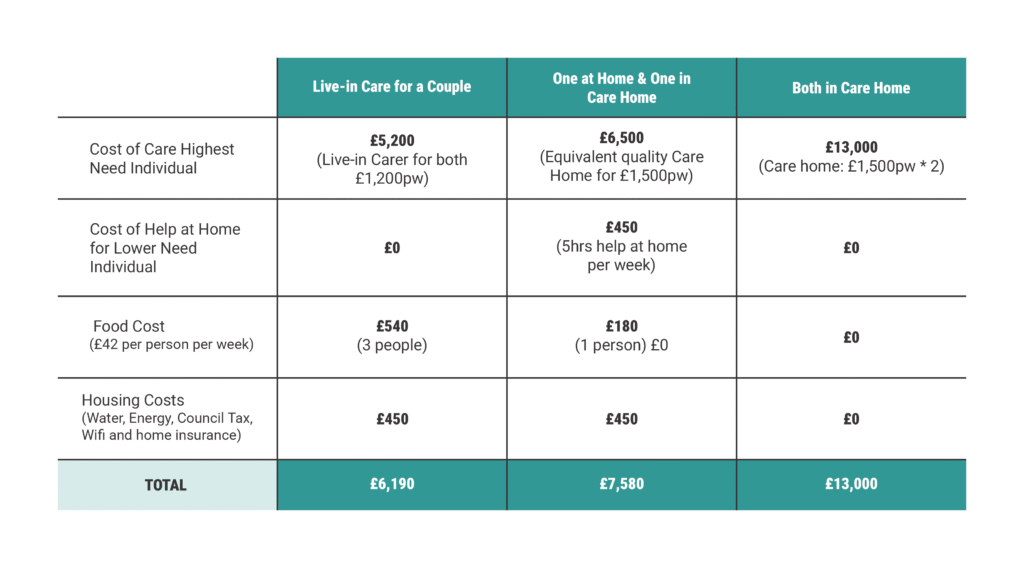

What about home care instead of a care home?

Not every person with dementia needs to move into a care home immediately. Many families first explore care at home, especially in the early or moderate stages of dementia. Understanding home care services cost can help caregivers decide whether staying at home is a practical alternative.

How much does home care cost per hour in the UK?

The cost of home care services depends on the level of support required and the region where you live. On average:

- Home care services: around £20–£35 per hour

- Live-in carer cost: roughly £900–£1,600 per week depending on care needs

- Private nursing care: higher costs if medical support is required

Families often search questions such as “how much does home care cost per hour UK” or “how much does a home nurse cost” when deciding whether home care might be more affordable than residential care.

When home care may work better

Home care can be a suitable option when a person with dementia:

- Can still live safely in familiar surroundings

- Needs help with daily tasks such as washing, dressing, or medication

- Benefits from routine and familiar environments

In some situations, the local authority may also provide local authority funding for care in your own home after completing a needs and financial assessment.

When residential care becomes necessary

As dementia progresses, some people eventually require 24-hour supervision or specialist dementia support. At that stage, families may start exploring dementia care homes near me or a care home for dementia near me that offers structured care and specialist staff.

Understanding the differences between home care and residential care helps families make informed decisions about the cost of care homes, the price of long-term care, and the level of support their loved one truly needs.

How to get help with care home fees for dementia patients

Many families feel overwhelmed when they first learn about dementia care home costs in the UK. The good news is that several funding routes may help reduce or cover care home fees, depending on the person’s financial situation and care needs.

If you are wondering how to get help with care home fees, the process usually begins with two important assessments arranged through your local authority.

1. Request a care needs assessment

Start by asking your local council for a care needs assessment. A trained professional will evaluate the person’s condition and decide what level of support they require. This assessment determines whether the person needs:

- Home care support

- Specialist dementia care

- A residential or nursing care home

The results help the council decide what type of support they can provide.

2. Complete a financial assessment

If the person needs residential care, the council will then carry out a financial (means) assessment to determine who pays for the care.

The assessment considers:

- Savings and investments

- Income, such as pensions

- Property ownership

- Other financial assets

Depending on the results, the local authority may contribute toward the cost of care homes, or the person may need to self-fund their care.

3. Ask about NHS funding options

Families should also ask for an assessment for NHS Continuing Healthcare (CHC) if the person has complex health needs. If approved, CHC can cover the full cost of care, including accommodation in a care home.

If CHC is not granted but the person lives in a nursing home, they may still qualify for NHS-Funded Nursing Care, which contributes toward the nursing portion of care home fees.

4. Check benefits and financial support

Some people with dementia may qualify for additional financial help, including:

- Attendance Allowance

- Personal Independence Payment (PIP) for people under pension age

- Pension Credit

- Council tax reductions for severe mental impairment

These benefits can help cover daily expenses and reduce the overall price of long-term care.

5. Explore deferred payment schemes

If the person owns a home but does not want to sell it immediately, the local authority may offer a deferred payment agreement. This allows care fees to be paid later, usually when the property is eventually sold.

Understanding these steps helps families access help with care home fees for dementia patients and navigate the financial side of care with more confidence.

LEARN MORE: How a Domiciliary Care Agency Can Prepare for 2026 and Grow Faster

Finding dementia care homes near you

When dementia progresses, and care needs increase, many families begin searching online for dementia care homes near me or a care home for dementia near me. Choosing the right home can feel overwhelming, but taking a structured approach can make the process easier.

Start with local authority directories

Your local council usually keeps a list of approved providers and can help you identify government funded care homes near me that meet required standards. If the local authority funds part of the placement, they may suggest care homes that work within their funding arrangements.

However, families can still explore other dementia care homes if they prefer a different location or service. In some cases, this may involve paying a top-up fee if the chosen home costs more than the council normally covers.

Check care quality ratings

Before choosing a care home, review the inspection ratings from the relevant regulator:

- CQC (Care Quality Commission) in England

- Care Inspectorate Wales (CIW) in Wales

- RQIA in Northern Ireland

- Care Inspectorate in Scotland

Inspection reports can reveal important details about safety, staffing levels, and the quality of dementia care provided.

Visit care homes in person

Whenever possible, visit several dementia care homes near you before making a decision. Pay attention to:

- Staff interactions with residents

- Safety and cleanliness

- Activities designed for people with dementia

- Secure layouts for residents who may wander

Many homes offer specialist enhanced dementia care, including memory-friendly environments, trained staff, and structured daily routines.

Consider care needs and future progression

Dementia is a progressive condition, so it is important to choose a home that can support increasing care needs over time. Some homes provide both residential and nursing care, which allows residents to remain in the same environment as their condition changes.

Taking time to research and visit care homes for dementia near you helps families make confident decisions and ensures their loved one receives the level of care and support they truly need.

Key facts about dementia care home fees

If you are supporting someone with dementia, understanding how care home fees work can make the financial side of care much less confusing. The most important points families should remember include the following:

- Many people with dementia pay for their own care. Dementia care is usually treated as social care, which means funding depends on a financial assessment rather than being automatically covered by the NHS.

- Local authorities may help with the cost of care homes. If a person’s savings and assets fall below the capital thresholds, the council may contribute toward their care.

- NHS funding is sometimes available. People with complex medical needs may qualify for NHS Continuing Healthcare, which can cover the full cost of care.

- NHS-Funded Nursing Care may reduce costs. If someone lives in a nursing home but does not qualify for full NHS funding, the NHS may contribute a weekly amount toward the nursing element of care.

- Home care can be an alternative in earlier stages. Some families explore options such as live-in carers or hourly support before moving to residential care.

Understanding these key facts can help families plan ahead, explore help with care home fees for dementia patients, and make informed decisions about the best care options for their loved ones.

New rules for care home payments in the UK (2026 update)

Families often ask whether the government has introduced new rules for care home payments that could reduce the price of long-term care. The UK government has discussed several reforms to the social care system in recent years, but the way care home fees work largely remains the same for most families.

The proposed care cost cap

A major reform previously planned was a cap on lifetime care costs, which would have limited how much individuals pay for personal care over their lifetime. The proposed cap was set at £86,000.

However, the government later delayed these reforms, meaning the current funding system still relies mainly on the means-tested financial assessment used by local authorities.

What this means for families today

For now, most people entering a care home will still follow the existing system:

- People with assets above the upper capital limit usually self-fund their care.

- Those with fewer assets may receive local authority support.

- NHS funding remains available through Continuing Healthcare or NHS-Funded Nursing Care for those who qualify.

Because policy changes can happen over time, families should always check the latest government guidance or speak with their local authority before making long-term financial decisions about care.

Understanding these rules can help caregivers plan ahead and better prepare for the cost of care homes or specialist dementia care homes in the future.

Conclusion

Understanding whether dementia sufferers have to pay care home fees can feel confusing at first, especially when families face emotional and financial pressure at the same time. In the UK, dementia care is usually treated as social care, which means many people pay for some or all of their care home fees depending on their financial situation.

The amount someone pays depends on several factors, including their savings, property, and the outcome of a local authority financial assessment. Some people qualify for support from the council, while others may receive NHS funding through Continuing Healthcare or NHS-Funded Nursing Care if their needs are primarily medical.

Because dementia care home costs in the UK can be significant, families benefit from understanding the funding process early. Requesting a care needs assessment, exploring financial support options, and reviewing care home choices carefully can make the transition into long-term care much easier to manage.

Planning ahead also helps caregivers make informed decisions about the cost of care homes, home care alternatives, and the best level of support for their loved one.

If you are supporting someone with dementia and need guidance navigating care home fees, funding assessments, or NHS Continuing Healthcare applications, Care Sync Experts can help.

We work with families and care professionals to review funding eligibility, explain the assessment process clearly, and help present care needs accurately so you can access the financial support available for dementia care and avoid the common mistakes that delay or reduce funding.

FAQ

Do dementia patients do better at home or in a nursing home?

It depends on the stage of dementia and the level of support the person needs. In the early stages, many people with dementia do well at home because familiar surroundings can reduce confusion and anxiety. Family support, home care services, and structured routines often help maintain independence for longer.

However, as dementia progresses, some individuals require 24-hour supervision, specialist dementia care, or nursing support. At this stage, a dementia care home or specialist nursing home may provide a safer environment with trained staff, structured activities, and secure facilities designed to support memory-related conditions. The best option depends on the person’s safety, medical needs, and the level of support available at home.

How fast can dementia progress?

Dementia progresses at different speeds depending on the type of dementia, the person’s age, and their overall health. Some people experience slow progression over many years, while others may decline more quickly.

On average, many people live between 4 and 10 years after diagnosis, although some individuals live much longer. Certain forms of dementia, such as vascular dementia, may progress in noticeable steps, while Alzheimer’s disease typically causes a gradual decline. Regular medical reviews, supportive care, and early intervention can sometimes help slow the impact of symptoms.

What are the signs dementia is getting worse?

As dementia progresses, symptoms usually become more noticeable and begin to affect daily life more significantly. Families often notice changes in memory, behaviour, and independence.

Common signs that dementia may be worsening include:

– Increasing memory loss and confusion

– Difficulty recognising familiar people or places

– Problems with communication or finding words

– Changes in behaviour or mood, such as agitation or anxiety

– Difficulty managing everyday tasks like dressing, cooking, or taking medication

– Greater need for supervision and personal care

When these signs appear, families may start considering additional support such as home care services or specialist dementia care.

What are four common behaviours that people with dementia often exhibit?

People living with dementia often experience changes in behaviour because the condition affects memory, reasoning, and emotional regulation. While symptoms vary from person to person, several behaviours commonly occur.

Four common behaviours seen in people with dementia include:

Memory loss – forgetting recent events, appointments, or conversations

Confusion or disorientation – becoming lost in familiar places or forgetting the date or time

Mood or personality changes – increased anxiety, irritability, or withdrawal

Repetitive actions or questions – asking the same question repeatedly or repeating activities

These behaviours usually develop gradually as the condition progresses. Understanding them can help caregivers respond with patience and choose the right level of support for the person living with dementia.