The most accurate NHS pension calculator is the Total Reward Statement (TRS) or Annual Benefit Statement (ABS) available through ESR or My NHS Pension. These official tools use your actual NHS service record, pensionable pay, and scheme membership to estimate how much pension you could receive in retirement.

For caregivers, nurses, and NHS staff, understanding your pension matters just as much as understanding your salary. Your NHS banding, years of service, and pension scheme all directly affect your retirement income.

Key Takeaways

- The official NHS pension calculator is available through ESR, your Total Reward Statement (TRS), or My NHS Pension.

- Your pension estimate depends on your NHS pension scheme, pensionable pay, and total years of service.

- Staff in higher NHS banding levels, such as Band 6 NHS pay and Band 7 NHS pay, usually build larger pension benefits over time.

- The 1995, 2008, and 2015 NHS pension schemes all calculate benefits differently.

- Many caregivers use both an NHS salary calculator and an NHS pension calculator to compare take-home pay with long-term retirement income.

- The NHS Pension calculator UNISON tools and official NHS calculators can help staff model retirement scenarios and early retirement options.

- Understanding the NHS pension scheme April 2025 changes can help caregivers plan their future contributions and retirement age more effectively.

What Is the Most Accurate NHS Pension Calculator?

The most accurate NHS pension calculator is your official Annual Benefit Statement (ABS) or Total Reward Statement (TRS), available through ESR or My NHS Pension. These tools calculate your pension using your real NHS employment history, pensionable earnings, and current scheme membership.

Many NHS workers search for terms like:

- Nhs pension calculator gov uk

- NHS Pension calculator UNISON

- Nhs pension calculator 2022

However, official NHS records almost always provide the most reliable estimate because they include:

- your actual years of service

- pension contributions

- salary progression

- scheme transfers

- retirement age calculations

Where NHS Staff Can Access Their Pension Estimate

| Tool | Best For | Accuracy |

| ESR Total Reward Statement (TRS) | Current NHS staff | Highest |

| My NHS Pension | Non-ESR users | High |

| UNISON NHS Pension Calculator | Quick estimates | Moderate |

| NHS Ready Reckoner Tools | General projections | Moderate |

Why Caregivers Should Check Their Pension Regularly

Many caregivers focus on monthly earnings and overtime but overlook long-term retirement income. Your pension can become one of your most valuable financial benefits throughout your NHS career.

For example, a nurse on Band 6 NHS pay 2025 may contribute thousands of pounds yearly into the NHS pension scheme while also receiving significant employer contributions.

Checking your pension regularly helps you:

- understand your projected retirement income

- plan early retirement options

- track contribution growth

- compare pension value against current take-home pay

- prepare for future changes in the NHS pension scheme

The NHS pension scheme remains one of the most valuable public sector pension schemes in the UK for long-term healthcare workers and caregivers.

RELATED: PIP and ADP Insider Tips for 2026: Everything You Need to Know

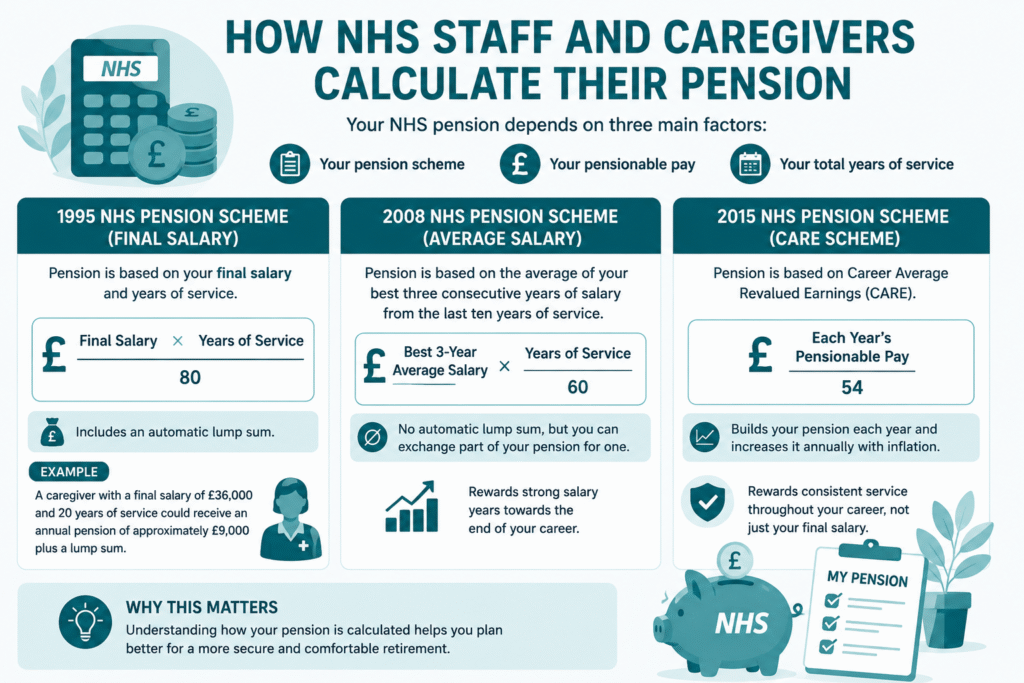

How NHS Staff and Caregivers Calculate Their Pension

Your NHS pension depends on three main factors:

- your pension scheme

- your pensionable pay

- your total years of service

Many caregivers ask:

“How much NHS pension will I get after 20 years?”

The answer varies based on whether you belong to the 1995, 2008, or 2015 NHS pension scheme.

NHS Pension Calculator 1995 Section

The 1995 scheme calculates pension using your final salary and years of service.

Final Salary×Years of Service80\frac{\text{Final Salary}\times \text{Years of Service}}{80}80Final Salary×Years of Service

This scheme also includes an automatic lump sum.

Example

A caregiver with:

- final salary of £36,000

- 20 years of service

could receive an annual pension of approximately £9,000 plus a lump sum.

2008 NHS Pension Scheme

The 2008 section uses the average of your best three consecutive years of salary from the last ten years of service.

Best 3-Year Average Salary×Years of Service60\frac{\text{Best 3-Year Average Salary}\times \text{Years of Service}}{60}60Best 3-Year Average Salary×Years of Service

This scheme does not automatically include a lump sum, although members can usually exchange part of their pension for one.

2015 NHS Pension Scheme (CARE)

The 2015 scheme uses a Career Average Revalued Earnings (CARE) model.

Each Year’s Pensionable Pay54\frac{\text{Each Year’s Pensionable Pay}}{54}54Each Year’s Pensionable Pay

Each year, the NHS adds a portion of your pensionable earnings to your pension pot and adjusts it annually for inflation.

This structure benefits many long-term caregivers because it rewards consistent service across an entire career rather than only focusing on final salary.

Why Your Salary Matters

Your pension grows alongside your earnings. Staff progressing through Agenda for Change pay scales often see pension growth as they move through different NHS bands.

For example:

- Band 5 NHS pay builds a smaller pension than Band 6

- Band 6 NHS pay and Band 7 NHS pay usually generate larger retirement benefits due to higher pensionable earnings

That is why many staff use both an NHS pay calculator and an NHS pension calculator together when planning their finances.

How NHS Banding and Salary Affect Your Pension

Your NHS pension increases as your salary increases. Higher earnings usually lead to higher pension contributions and larger retirement benefits over time.

Many caregivers and nurses move gradually through different levels of NHS banding during their careers. Each promotion can improve both monthly earnings and future pension income.

How Agenda for Change Pay Scales Influence Pension Growth

The NHS uses Agenda for Change pay scales to determine salary bands for most healthcare staff. As your salary rises, your pensionable pay also rises.

For example:

- a healthcare assistant on Band 4 NHS salary

- a nurse on Band 5 NHS pay

- a senior nurse on Band 6 NHS pay

- or a manager on Band 7 NHS pay

will all build different pension values based on their earnings and years of service.

Band 6 NHS Pay and Pension Impact

Many caregivers search for:

- nhs band 6 salary

- band 6 nhs pay 2025

- nurse earnings uk

because Band 6 often marks a major jump in both salary and pension growth.

A higher pensionable salary means:

- larger yearly pension accrual

- higher employer contributions

- stronger retirement income projections

For many NHS workers, pension growth accelerates after progressing beyond Band 5.

Why NHS Staff Use Salary and Pension Calculators Together

An NHS salary calculator or NHS take home pay calculator helps staff estimate monthly pay after tax and pension deductions.

An NHS pension calculator helps estimate long-term retirement income.

Using both tools together gives caregivers a clearer financial picture because:

- take-home pay affects current lifestyle

- pension contributions affect future retirement security

This balance matters even more as staff prepare for:

- the NHS pay rise July 2025

- pension contribution adjustments

- and wider NHS pension scheme April 2025 changes.

READ MORE: End of Life Care at Home: What to Expect in 2026, Costs, and Family Support

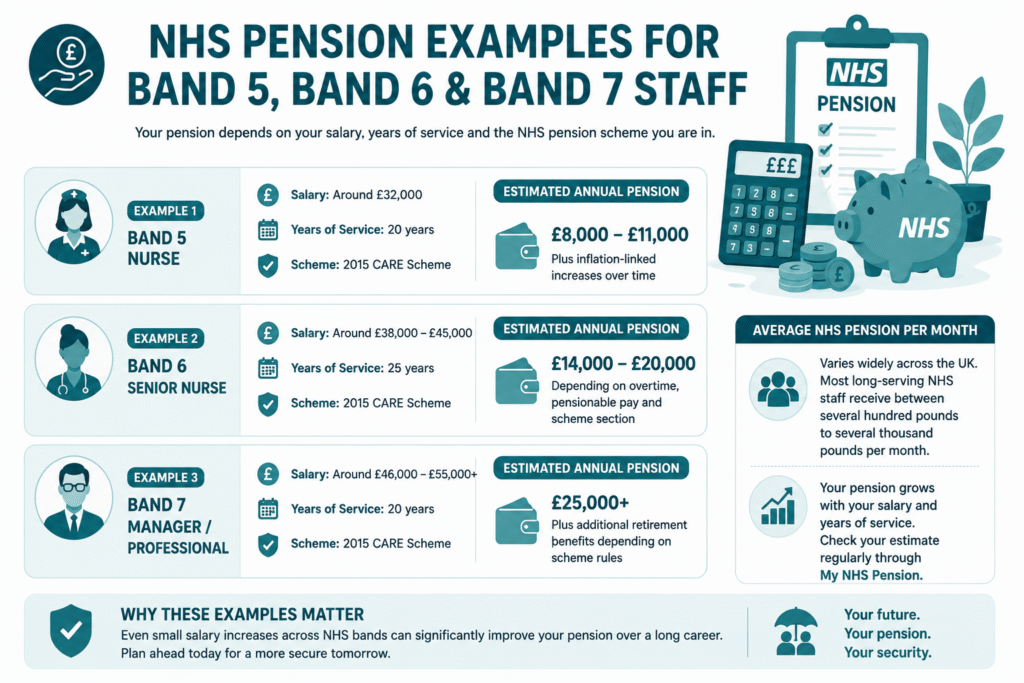

NHS Pension Examples for Band 5, Band 6, and Band 7 Staff

Real-life pension examples help caregivers understand how salary and years of service affect retirement income. These estimates are not official figures, but they show how the NHS pension scheme can build long-term financial security.

Example 1: Band 5 Nurse

A nurse earning approximately £32,000 under Band 5 NHS pay with 20 years of NHS service could build a pension worth several thousand pounds yearly, depending on their scheme membership and retirement age.

Under the 2015 CARE scheme, consistent yearly contributions and salary progression could produce:

- an estimated pension of £8,000–£11,000 annually

- plus inflation-linked increases over time

Example 2: Band 6 NHS Salary

A caregiver or senior nurse on Band 6 NHS pay 2025 earning around £38,000–£45,000 may build significantly higher benefits over the same career period.

After 25 years of service, many Band 6 staff could potentially receive:

- £14,000–£20,000 yearly pension income

- depending on overtime, pensionable pay, and scheme section

This is one reason many NHS workers closely monitor their pension growth through My NHS Pension and ESR statements.

Example 3: Band 7 NHS Pay

Staff on Band 7 NHS pay often contribute more into the scheme because of higher pensionable earnings.

A Band 7 healthcare professional with:

- 30 years of NHS service

- salary progression through multiple pay points

- stable pension contributions

could potentially build:

- annual pension income above £25,000

- plus additional retirement benefits depending on scheme rules

Average NHS Pension Per Month

The average NHS pension per month varies widely across the UK because retirement income depends on:

- career length

- salary history

- pension scheme membership

- retirement age

Many long-serving NHS workers and caregivers receive monthly pensions ranging from several hundred pounds to several thousand pounds after retirement.

That is why checking your pension estimate regularly matters, especially if your salary changes or you move into higher NHS bands.

ALSO SEE: HICBC Child Benefit Rule Change UK: What Care Workers Need to Know in 2026

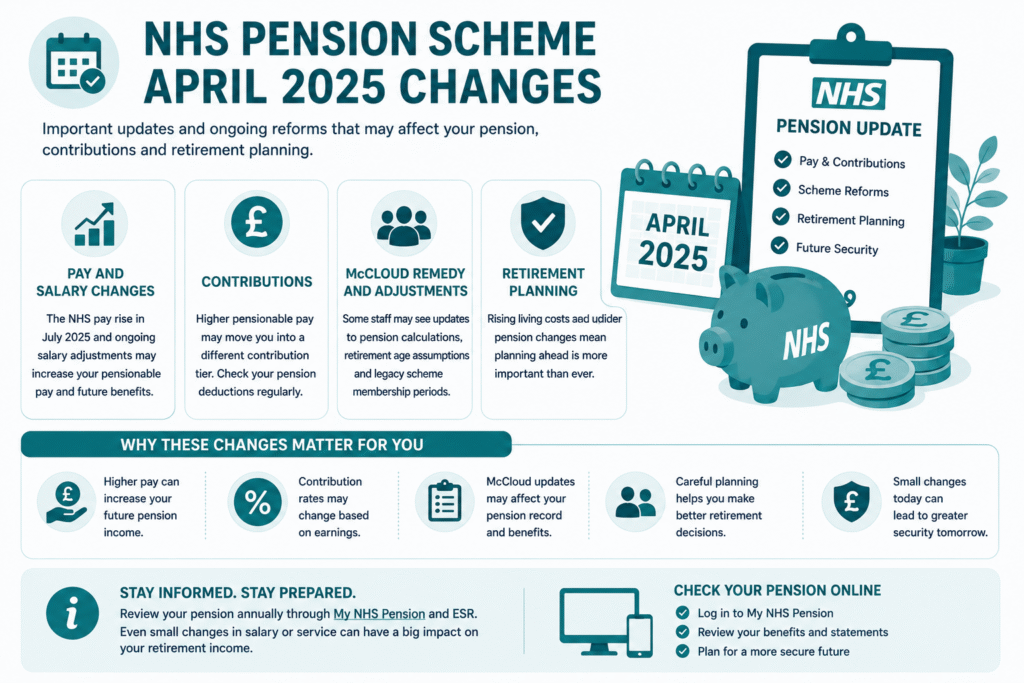

NHS Pension Scheme April 2025 Changes Caregivers Should Know

Recent updates to the NHS pension scheme continue to affect how caregivers, nurses, and healthcare staff plan for retirement. Understanding these changes can help you make better decisions about contributions, retirement timing, and long-term financial planning.

Pension Contribution and Pay Changes

The NHS pay rise July 2025, and ongoing salary adjustments across NHS bands may increase pensionable pay for many staff. Higher pensionable earnings can improve future pension benefits, but they may also move some workers into higher contribution tiers.

Caregivers should regularly review:

- contribution rates

- pension deductions

- updated pay bands

- retirement projections

especially after promotions or salary increases.

McCloud Remedy and Scheme Adjustments

Many NHS workers still review how the McCloud remedy affects their pension records and retirement estimates. Some staff may see updates to:

- pension calculations

- retirement age assumptions

- legacy scheme membership periods

This especially affects workers with service spanning multiple NHS pension schemes.

Retirement Planning Matters More Than Ever

Rising living costs and wider retirement concerns, including discussions around UK pensioner cash withdrawal changes 2025, have encouraged many healthcare workers to pay closer attention to pension planning.

For caregivers and NHS staff, reviewing your pension annually can help you:

- avoid retirement surprises

- understand projected income

- prepare for early retirement decisions

- maximise long-term pension value

Even small salary increases across NHS bands can significantly affect retirement income over a long healthcare career.

MORE: Is There a Senility Test? 2026 Guide to Dementia Screening Tools

Should You Use an NHS Salary Calculator or Pension Calculator?

An NHS salary calculator and an NHS pension calculator serve different purposes. Most caregivers and NHS workers benefit from using both together.

An NHS salary tool estimates:

- monthly take-home pay

- tax deductions

- National Insurance

- pension deductions

An NHS pension tool estimates:

- future retirement income

- yearly pension growth

- projected benefits after retirement

When to Use an NHS Salary Calculator

An NHS pay calculator or NHS take home pay calculator helps staff understand how much money reaches their bank account each month.

This becomes especially useful when:

- moving between NHS bands

- checking overtime impact

- reviewing salary increases

- comparing new job offers

For example, staff moving from Band 5 NHS pay to Band 6 NHS pay often use salary calculators to estimate changes in take-home income before accepting a new role.

When to Use an NHS Pension Calculator

An NHS pension calculator helps caregivers plan for long-term financial security.

You should check your pension estimate when:

- your salary changes

- you change NHS bands

- you plan early retirement

- you approach retirement age

- pension rules change

Official tools through ESR or My NHS Pension usually provide the most accurate estimates because they use your real employment and contribution records.

Why Both Tools Matter

Many NHS workers focus heavily on present income but underestimate the long-term value of the NHS pension scheme.

Using both calculators together helps caregivers:

- balance current income with future retirement planning

- understand how pension contributions affect take-home pay

- make better career and retirement decisions

For long-serving healthcare staff, the NHS pension can become one of the most valuable financial benefits they ever receive.

Conclusion

The NHS pension scheme remains one of the strongest retirement benefits available to healthcare workers and caregivers in the UK. Whether you work under Band 5 NHS pay, Band 6 NHS pay, or Band 7 NHS pay, your salary, years of service, and pension scheme all directly shape your future retirement income.

Using an official NHS pension calculator through ESR or My NHS Pension gives you the clearest picture of what you may receive in retirement. Combining this with an NHS salary calculator or NHS take home pay calculator can also help you balance present earnings with long-term financial security.

For caregivers and NHS staff, regular pension reviews are no longer optional. Understanding your pension today can help you make smarter career, salary, and retirement decisions for the future.

Need Help Navigating NHS Career, Compliance, or Workforce Support?

At Care Sync Experts, we help caregivers, care providers, and healthcare organisations stay informed about the latest NHS workforce developments, compliance updates, funding opportunities, and operational best practices.

Whether you run a care business or work within the NHS, our resources and expert guidance can help you make more confident financial and professional decisions in 2026 and beyond.

FAQ

Is an NHS pension a good pension?

Many financial experts consider the NHS pension one of the strongest public sector pension schemes in the UK. The scheme includes employer contributions, inflation-linked benefits, and long-term retirement security that many private pensions do not fully match.

For long-serving caregivers and NHS workers, the pension can become a major part of their retirement income.

What percentage of my NHS pension do I pay?

NHS pension contributions vary based on your pensionable salary. Lower earners pay a smaller percentage, while higher earners contribute more through tiered contribution rates.

Contribution rates typically range from around 5% to over 12% depending on:

– NHS banding

– pensionable pay

– current contribution thresholds

Your employer also contributes a significant percentage toward your pension.

What happens to my NHS pension if I leave the NHS?

If you leave the NHS before retirement, your pension usually remains in the scheme as a deferred pension. It will normally continue to increase in value over time until you reach retirement age.

Your options may include:

– leaving the pension where it is

– transferring it to another pension scheme

– returning to NHS employment later and continuing contributions

The best option depends on your career plans and length of NHS service.

What are the disadvantages of taking your pension at 55?

Taking your NHS pension early can reduce your yearly retirement income because the scheme expects to pay benefits for a longer period.

Early retirement may lead to:

– permanently reduced pension payments

– lower lifetime pension value

– reduced lump sum options

– fewer contribution years

Many caregivers choose to compare early retirement estimates carefully before making a final decision.