The HICBC child benefit rule change UK families continue to face in 2026 still affects thousands of care workers, NHS staff, and caregiver households across the country. HMRC raised the High Income Child Benefit Charge threshold from £50,000 to £60,000 in the 2024/25 tax year, while full withdrawal of Child Benefit now applies once adjusted net income reaches £80,000.

Under the current rules, families repay 1% of their Child Benefit for every £200 earned above £60,000. For many caregivers who regularly work overtime, bank shifts, or agency hours, the updated child benefit changes 2026 rules reduce the tax hit but still create important decisions around Child Benefit claims, National Insurance credits, and household finances.

What Changed Under the High Income Child Benefit Charge Rules?

The biggest child benefit changes threshold 2025 to 2026 families noticed came from HMRC’s decision to raise the High Income Child Benefit Charge threshold to £60,000 and extend the taper range to £80,000.

Before these changes, families started paying the charge once one partner earned more than £50,000, and they lost the full benefit at £60,000.

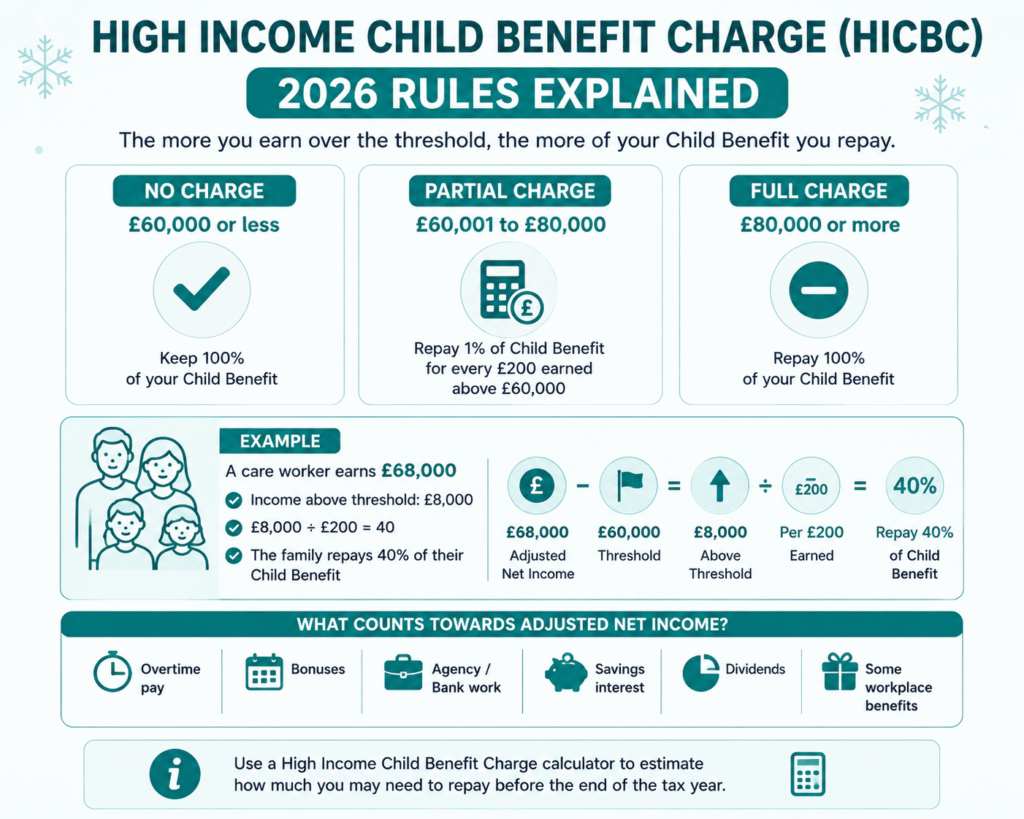

Under the current child benefit high income charge 2024/25 rules:

- No charge applies if the highest earner makes £60,000 or less

- Families repay 1% of Child Benefit for every £200 earned above £60,000

- Full repayment only applies once income reaches £80,000

- HMRC can now collect the charge automatically through PAYE for some employees

For many healthcare workers and caregivers, this update reduced the financial pressure caused by the previous system. However, overtime pay, night shifts, NHS bank work, and agency contracts can still push earnings above the threshold unexpectedly.

Example

A domiciliary care manager earns £68,000 after overtime and additional weekend shifts.

- Income above threshold: £8,000

- £8,000 ÷ £200 = 40

- The family repays 40% of their Child Benefit through the High Income Child Benefit Charge

Many parents now use a child benefit tax calculator or high income child benefit charge calculator to estimate how much they may need to repay before the end of the tax year.

Alongside these HICBC updates, many families also saw a child benefit increase 2025 adjustment in their monthly payments. HMRC child benefit changes 2026 discussions continue to focus on whether the system should eventually move to a household-income model instead of the current highest-earner approach.

RELATED: Children’s DLA Rates: Who Qualifies, and What to Claim in 2026

Why Many Care Workers Still Lose Child Benefit Despite Modest Household Income

Many caregiver families support the latest HICBC child benefit rule change UK updates because the higher threshold reduced penalties on middle-income households. However, the system still creates challenges for care workers whose income changes throughout the year.

In the care sector, earnings rarely stay predictable. A support worker may accept extra shifts during staffing shortages. An NHS employee may work bank holidays or overnight hours. A domiciliary care worker may combine agency contracts with full-time employment to manage rising living costs.

These additional earnings can quickly push one partner above the High Income Child Benefit Charge threshold, even when the household does not feel “high income.”

This issue explains why many families continue to debate whether the High Income Child Benefit Charge should be scrapped or replaced with a fairer household-income system.

Under the current rules, a single parent earning £62,000 may repay part of their Child Benefit, while a couple earning £59,000 each may keep the full amount despite having a much higher combined household income.

For many healthcare and caregiver households, this creates frustration because:

- overtime often counts toward adjusted net income

- one-income caregiving households face higher pressure

- inflation and childcare costs continue to rise

- some families already rely on universal credit or other support alongside employment income

The government previously discussed moving to a household-income model as part of wider child benefit changes 2026 reforms. However, no full reform or confirmed plan to scrap the high income child benefit charge currently exists.

Care workers should also remember that adjusted net income includes more than salary alone. HMRC may include:

- overtime pay

- bonuses

- savings interest

- dividends

- some workplace benefits

Because of this, many families only discover they crossed the threshold after the tax year ends.

READ MORE: CHC Funding: A Caregiver’s Step-by-Step Guide (2026)

Should Caregivers Still Claim Child Benefit After the HICBC Changes?

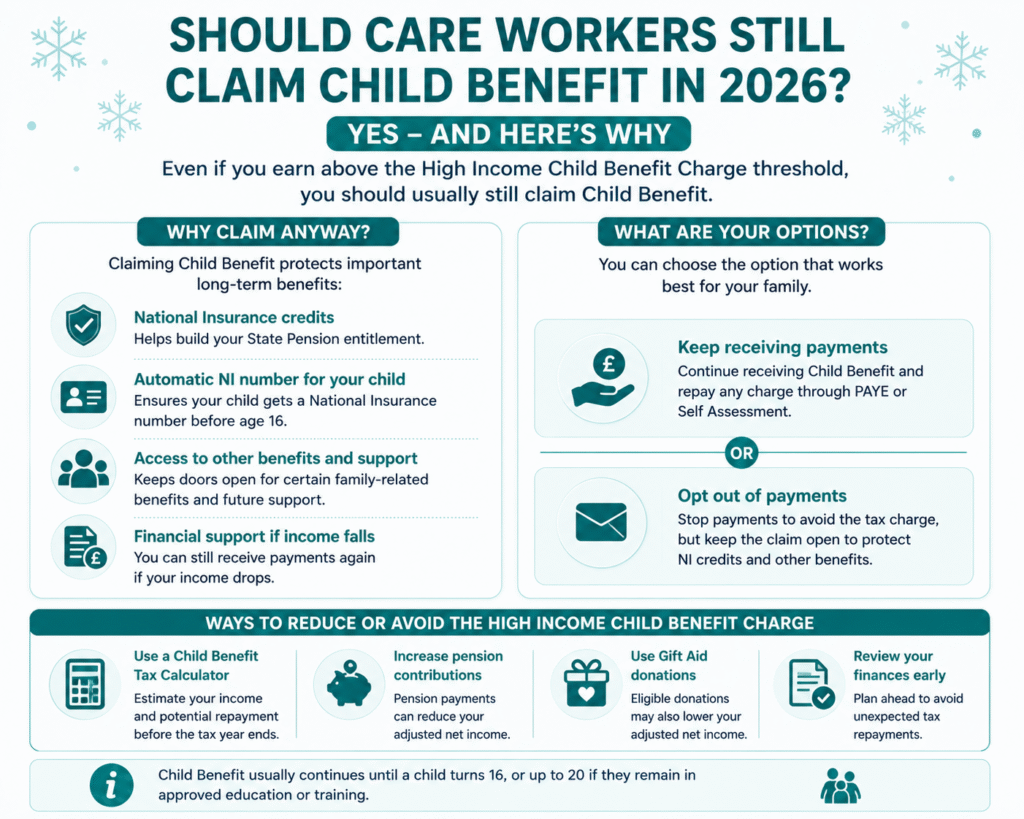

Yes, most caregiver families should still claim Child Benefit, even if the highest earner exceeds the High Income Child Benefit Charge threshold.

Many parents wrongly assume Child Benefit stops automatically once income passes £60,000. In reality, families can continue claiming while choosing whether to receive payments or opt out to avoid the tax charge.

This distinction matters because claiming Child Benefit still protects important long-term benefits, including:

- National Insurance credits that count toward the State Pension

- automatic National Insurance numbers for children before age 16

- access to certain family-related benefits and records

- financial support if household income later falls

This issue affects many care workers, especially parents who reduce working hours to provide care at home or balance childcare responsibilities with demanding shift patterns.

When does Child Benefit stop?

Child Benefit usually continues until a child turns 16, or up to age 20 if they remain in approved education or training. The High Income Child Benefit Charge does not automatically stop Child Benefit entitlement; it only creates a tax repayment obligation for higher earners.

For some caregiver households, opting out of payments may still make sense. Others prefer receiving the payments and repaying part of the amount later through PAYE or Self Assessment. Many families now use a child benefit tax calculator before making that decision.

Parents should also review whether pension contributions or Gift Aid donations could reduce adjusted net income below the threshold. In some cases, additional pension contributions may lower or completely remove the high income child benefit charge.

Families who already receive universal credit or previously claimed child tax credit 2025 support should carefully assess how Child Benefit interacts with their wider household finances before opting out completely.

SEE ALSO: Scottish Pension Age Winter Heating Payment (PAWHP): 2026 Update

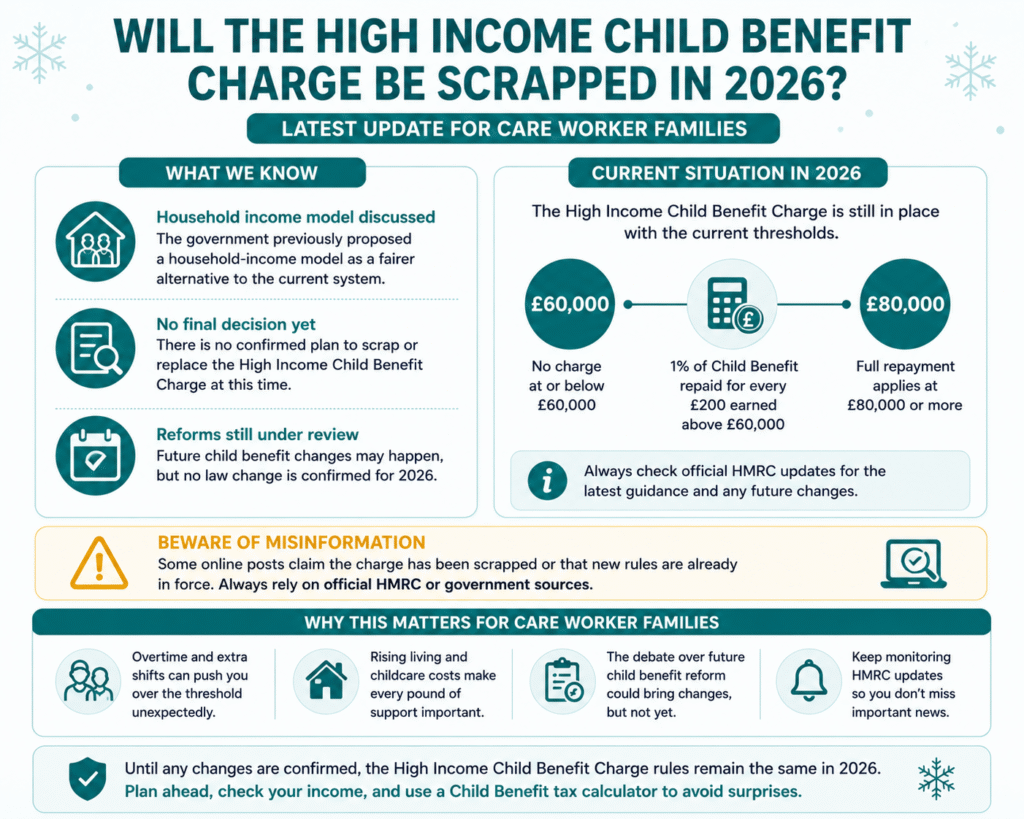

Will the High Income Child Benefit Charge Be Scrapped in 2026?

Many parents continue searching for updates about whether the High Income Child Benefit Charge will be scrapped as pressure grows over the fairness of the current system.

The government previously announced plans to explore a household-income model instead of the existing highest-earner approach. Under that proposal, HMRC would assess combined household income rather than focusing only on the highest individual earner. Many caregiver families supported the idea because it would reduce the imbalance between single-income households and dual-income couples.

However, as of 2026, the government has not confirmed a full replacement or abolition of the High Income Child Benefit Charge. Current HMRC child benefit changes 2026 discussions still focus mainly on improving administration, tax collection, and fairness within the existing framework.

Care workers should therefore avoid relying on online claims suggesting:

- the High Income Child Benefit Charge has already been scrapped

- all new Child benefit rules october 2025 reforms are fully active

- HMRC confirmed child benefit will increase starting april 2026 for every household regardless of income

Some reports and social media posts mix confirmed policy changes with political proposals or early discussions. Families should always verify updates directly through HMRC or trusted financial guidance before making decisions about Child Benefit claims.

At the same time, many households did receive a child benefit payment increase UK 2025 adjustment following annual uprating changes. Additional discussions around wider welfare reform, including benefit payment timing and support changes, also increased public attention on family benefits throughout 2025 and 2026.

For caregiver families already managing rising childcare costs, housing expenses, and irregular shift income, the debate around future child benefit changes 2026 remains highly important.

MORE: Bank Holiday Early Benefit Payments DWP: May 2026 Update

Example: How the 2026 HICBC Rules Affect a Care Worker Family

Sarah works as a registered care manager for a domiciliary care provider in Manchester. Her basic salary sits at £58,000, but regular overtime, emergency weekend cover, and holiday shifts increased her adjusted net income to £66,400 during the tax year.

Her partner works part-time while caring for their two children.

Under the current high income child benefit charge rules:

- Sarah earns £6,400 above the £60,000 threshold

- £6,400 ÷ £200 = 32

- The family must repay 32% of their Child Benefit through the High Income Child Benefit Charge

Before the latest hicbc child benefit rule change uk updates, Sarah would have faced a much larger repayment because the old system started tapering at £50,000 and removed the full benefit at £60,000.

Like many care workers, Sarah originally considered stopping her Child Benefit claim completely. However, after reviewing the rules and using a high income child benefit charge calculator, she decided to continue claiming while keeping the National Insurance credits linked to the benefit.

This situation now affects many healthcare and caregiver households because:

- overtime can trigger the charge unexpectedly

- staffing shortages often increase annual earnings

- additional agency work may push income above the threshold

- fluctuating income makes tax planning harder

Families should also remember to keep HMRC records updated. If bank details change, parents can usually update their child benefit change bank details or family allowance change bank details information through HMRC’s online services to avoid delayed payments.

Key Takeaways for Care Workers and Families

- The hicbc child benefit rule change uk increased the income threshold from £50,000 to £60,000

- Families now lose the full Child Benefit amount only once adjusted net income reaches £80,000

- The High Income Child Benefit Charge removes 1% of Child Benefit for every £200 earned above £60,000

- Many care workers still cross the threshold because of overtime, bank shifts, and agency work

- Most families should still claim Child Benefit to protect National Insurance credits and future State Pension entitlement

- A child benefit tax calculator or high income child benefit charge calculator can help families estimate repayments before the tax year ends

- No confirmed policy currently exists to fully scrap the High Income Child Benefit Charge in 2026

- Parents should monitor HMRC child benefit changes 2026 updates carefully as future reforms may still affect caregiver households

Final Thoughts…

The latest child benefit changes 2026 updates brought welcome relief for many working families, but the High Income Child Benefit Charge still creates confusion for thousands of care workers, NHS staff, and caregiver households across the UK.

Overtime, agency work and unpredictable shift patterns can quickly change a family’s tax position, making it more important than ever to understand how the current rules affect your income and benefits.

For most families, the smartest approach is not to stop claiming Child Benefit altogether, but to understand how the system works, monitor adjusted net income carefully, and plan ahead before the tax year ends.

At Care Sync Experts, we help care businesses, healthcare professionals, and caregiver families stay informed about the latest compliance, funding, tax, and operational changes affecting the UK care sector.

Whether you run a domiciliary care agency, manage a care team, or simply want practical guidance that makes complex government updates easier to understand, our expert insights help you make confident decisions in a fast-changing industry.

FAQ

Can I claim Child Benefit if I earn over £50,000 in the UK?

Yes. Families can still claim Child Benefit even if one partner earns above £50,000 or the current £60,000 HICBC threshold. However, the highest earner may need to repay some or all of the benefit through the High Income Child Benefit Charge depending on their adjusted net income.

How much is UK Child Benefit per month?

Child Benefit rates usually change every tax year. In 2026, families receive weekly payments for each eligible child, with a higher amount paid for the eldest or only child. The exact monthly amount depends on the number of children you claim for and the latest HMRC uprating figures.

What happens to Child Benefit when your eldest child turns 18?

Child Benefit normally stops on 31 August after a child turns 16 unless they continue in approved education or training. If they remain eligible, payments can continue until they turn 20. Once the eldest child no longer qualifies, families usually receive the lower payment rate for younger children still on the claim.

What is the tax trap in the UK for childcare?

Many families describe the High Income Child Benefit Charge as part of the UK “childcare tax trap” because parents can lose benefits quickly once income crosses certain thresholds.

Care workers who regularly earn overtime or agency income may unexpectedly move into higher repayment bands, reducing the real value of additional earnings.

Leave a Reply