You may be able to claim Universal Credit compensation DWP if a DWP mistake, delay, poor service, or incorrect advice caused you financial loss, serious inconvenience, distress, or hardship.

This does not mean every reduced Universal Credit payment leads to compensation. You need to show what went wrong, when it happened, and how it affected the claimant.

For carers and family members, this matters because vulnerable claimants may not always spot an error quickly. Someone you support may miss a journal message, misunderstand a decision letter, struggle with the Universal Credit log in, or feel too overwhelmed to challenge DWP.

There are different routes depending on the problem. Some people may qualify for the Successful Legacy Appeals Compensation Scheme if they lost money after moving from legacy benefits to Universal Credit because of a decision that later turned out to be wrong. Others may need to use the DWP complaints process and ask for financial redress.

The key question is simple: did DWP’s action or failure cause a real loss or unfair hardship? If yes, it may be worth checking whether a Universal Credit compensation DWP claim or complaint applies.

When Can DWP Pay Universal Credit Compensation?

DWP may pay compensation when its own error or poor service causes a claimant to lose money, face avoidable hardship, or suffer serious inconvenience. This can happen if DWP gives incorrect advice, delays action, misses evidence, sends confusing information, or handles a Universal Credit claim badly.

However, compensation is different from normal Universal Credit back pay. If DWP simply underpaid someone, it should correct the award and pay the money owed. Compensation usually applies when the claimant suffered extra loss or distress because of the way DWP handled the case.

There are three common routes:

- A corrected benefit decision — DWP pays arrears after fixing a wrong Universal Credit decision.

- Financial redress for poor service — DWP considers compensation for maladministration, delay, wrong advice, distress, or financial loss.

- A specific scheme — some claimants may qualify under the Successful Legacy Appeals Compensation Scheme.

If you searched for Universal Credit compensation DWP 2025, check the latest rules before acting, because compensation schemes and benefit rates can change. For most people, the best first step is to gather evidence and make a formal complaint before considering whether to escalate further.

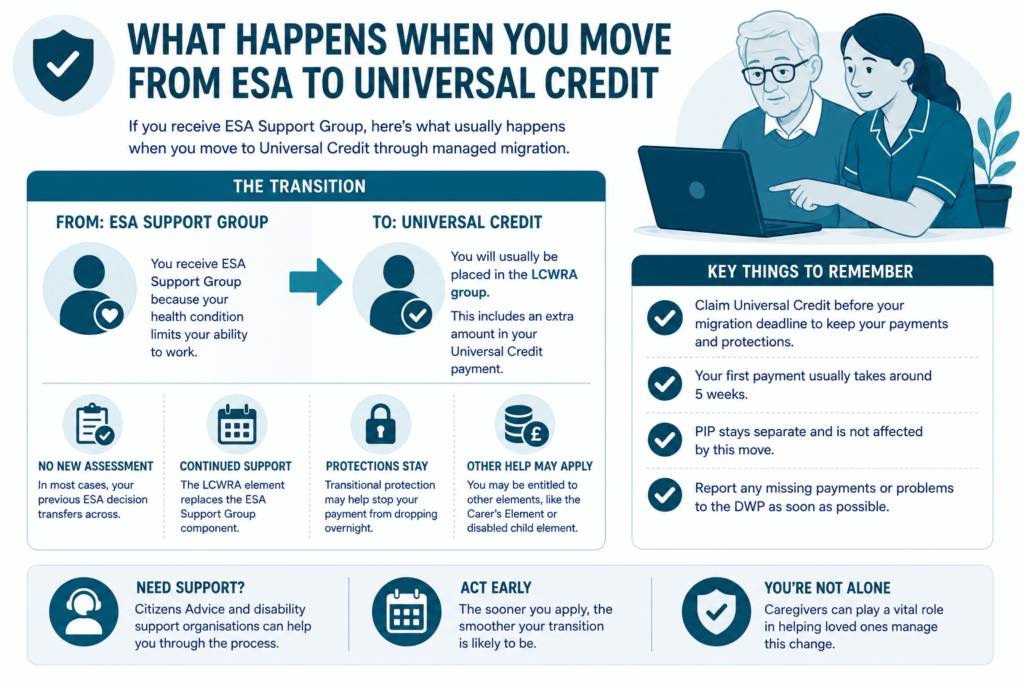

RELATED: Moving From ESA Support Group to Universal Credit: What You Need to Know in 2026

The Successful Legacy Appeals Compensation Scheme Explained

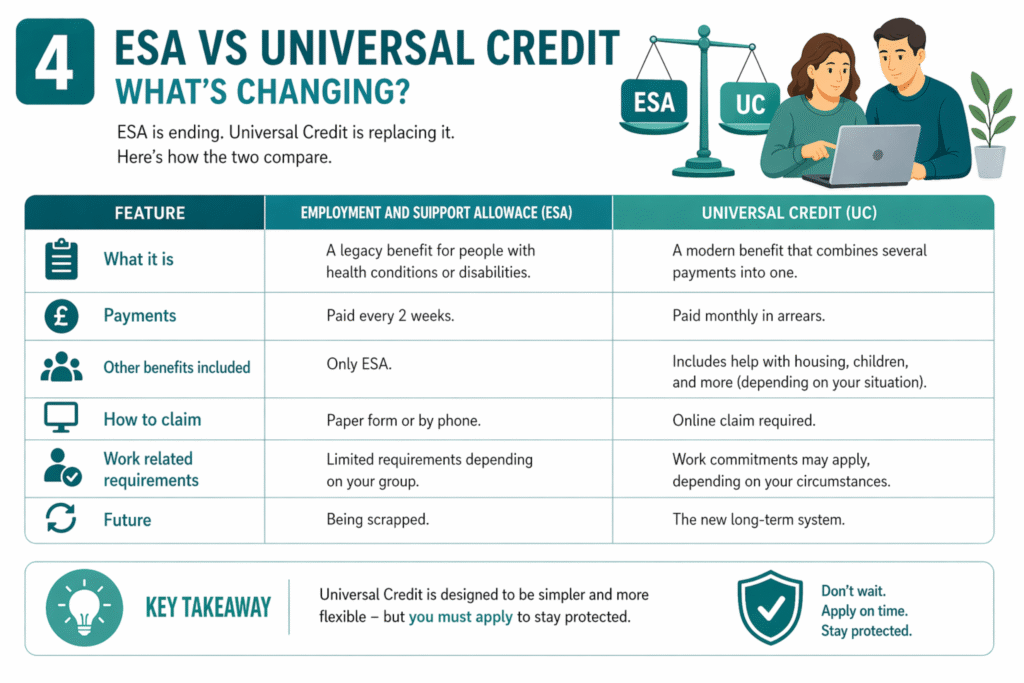

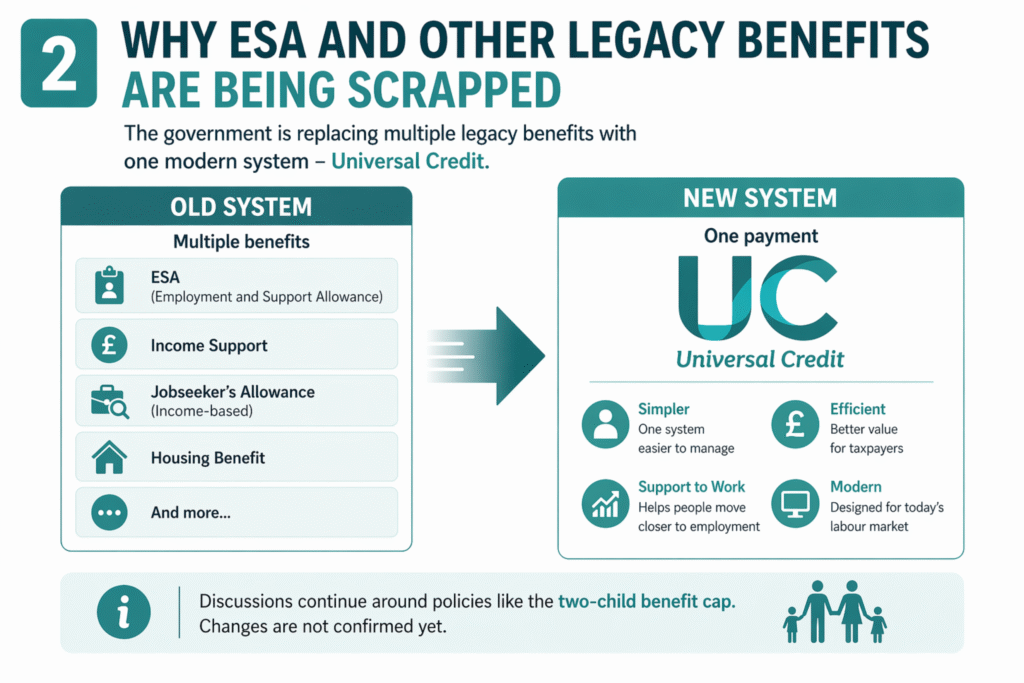

The Successful Legacy Appeals Compensation Scheme helps a specific group of people who lost money after moving from legacy benefits to Universal Credit.

This may apply if DWP stopped someone’s old benefit, the person claimed Universal Credit within one month, and they later won an appeal that showed the old benefit should not have ended. Because they had already moved to Universal Credit, they could not return to the legacy benefit, even though the original decision was wrong.

To qualify, the claimant must usually show that:

- they received a means-tested legacy benefit, such as income-related ESA, income-based JSA, Income Support, Housing Benefit, Child Tax Credit, or Working Tax Credit

- DWP made a decision that ended that benefit

- they claimed Universal Credit within one month of that decision

- Universal Credit paid less than the old benefit

- they challenged the decision and won

This scheme does not cover every Universal Credit complaint. It focuses on people who lost money because an incorrect legacy benefit decision pushed them onto Universal Credit. For carers, the key job is to help the claimant find old letters, appeal decisions, payment statements, and dates, because those details can prove whether a Universal Credit compensation DWP claim fits this route.

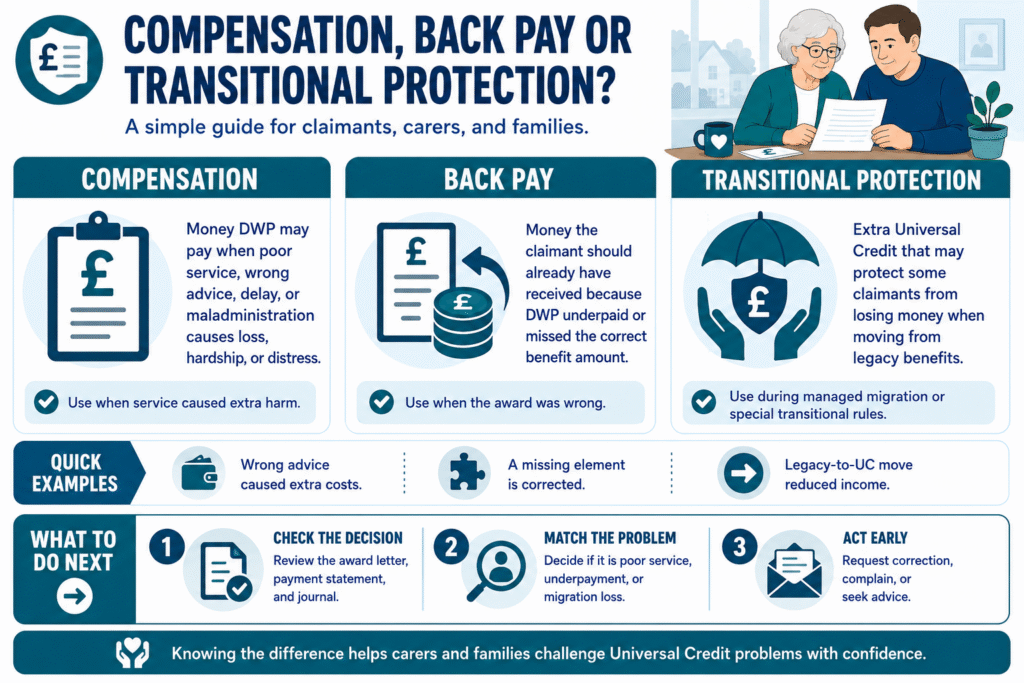

Compensation, Back Pay and Transitional Protection: What Is the Difference?

Many people mix up compensation, back pay, and transitional protection, but they do not mean the same thing.

| Term | What it means |

| Compensation | Money DWP may pay when poor service, delay, wrong advice, or maladministration causes loss, distress, or serious inconvenience |

| Back pay | Money DWP already owed because the claimant should have received more Universal Credit or another benefit |

| Transitional protection | Extra Universal Credit that may protect some people from losing money when they move from legacy benefits under managed migration |

| Personal injury compensation | Legal compensation for an injury, which may affect means-tested benefits if not handled correctly |

This matters because the next step depends on the problem. If DWP calculated the award wrongly, the claimant may need a correction or appeal. If DWP handled the case badly, they may need to complain and ask for financial redress. If the issue involves migration from legacy benefits, they may need to check transitional protection or the legacy appeals scheme.

For carers, the safest approach is to separate the facts: what DWP should have paid, what DWP actually paid, and what extra harm the error caused. That makes any Universal Credit compensation DWP complaint clearer and harder to ignore.

READ MORE: Band C Council Tax Per Month: What You Should Know in 2026

What Evidence Should Carers and Families Gather?

Before you complain, gather evidence. Do not rely on memory alone. DWP will look at dates, decisions, payment records, messages, and what impact the mistake had on the claimant.

Start with the claimant’s Universal Credit log in. Check the journal, payment statements, deductions, housing costs, reported earnings, decision notices, and any messages from work coaches or case managers. Take screenshots or download records where possible.

Carers and families should collect:

- Universal Credit journal messages

- decision letters

- mandatory reconsideration notices

- appeal decisions

- bank statements showing missing or reduced payments

- dates of phone calls or appointments

- names of DWP staff, if available

- evidence of extra costs, rent arrears, debt, hardship, or distress

- medical or caring evidence if the claimant struggled to manage the claim

Also keep the Universal Credit number and any reference numbers close by when contacting DWP.

Strong evidence helps you explain what happened clearly: what DWP did, what should have happened, how much money the claimant lost, and why compensation or financial redress may be reasonable.

How Earnings and Work Allowance Can Affect Universal Credit

Earnings can reduce Universal Credit, so a lower payment does not always mean DWP made a mistake. If the claimant works, DWP usually looks at monthly earnings and adjusts the award for that assessment period.

The Universal Credit work allowance is the amount some people can earn before their Universal Credit starts to reduce. A claimant may get a work allowance if they have responsibility for a child or have limited capability for work. After that allowance, Universal Credit reduces through the earnings taper.

This is why people often ask, “how much Universal Credit will I get if I earn 1000 a month,” “how much Universal Credit will I get if I earn 1500 a month,” or “how much Universal Credit will I get if I earn 2000 a month.” The answer depends on the person’s Universal Credit standard allowance, rent, children, disability elements, caring responsibilities, deductions, savings, and work allowance.

For carers, always check the payment statement before assuming DWP owes compensation. If the statement shows the wrong earnings, missing housing costs, incorrect deductions, or a missing element, challenge the calculation first. Compensation only becomes relevant if DWP’s error, delay, or poor service caused extra loss or hardship.

SEE ALSO: Income Taxation UK: A Simple Guide for Care Businesses (2026)

Savings, ISAs, Pensions and Compensation Payments

Savings and lump sums can affect Universal Credit because it is a means-tested benefit. This means DWP looks at income, savings, investments, and some types of capital when working out entitlement.

In most cases, savings over £6,000 can reduce Universal Credit, and savings over £16,000 can stop entitlement. So, if you are asking how much savings are you allowed on Universal Credit or how much saving can you have on Universal Credit, those two figures matter.

ISAs usually count as savings, so the answer to do ISAs count as savings for Universal Credit is normally yes. DWP can also ask for bank statements or evidence of accounts, so families often ask, can Universal Credit check my savings account? DWP can request financial information when checking entitlement or investigating a claim.

Pension income can also affect Universal Credit. If someone asks, does State Pension affect Universal Credit, the answer is yes: pension income can reduce entitlement. A pension lump sum may also affect Universal Credit if the claimant keeps it as capital, so ask for welfare advice if you are unsure how long does a pension lump sum affect Universal Credit.

Personal injury compensation needs extra care. If someone asks does personal injury compensation affect benefits or can DWP take my compensation, get specialist advice before spending or moving the money. A properly handled compensation payment may receive different treatment, but mistakes can affect means-tested benefits.

Does Universal Credit Affect Credit Score or Tax?

Universal Credit does not usually appear as borrowing on a credit report, so receiving it should not directly damage a credit score. However, money problems linked to a reduced or delayed payment can still affect someone’s credit record. For example, missed rent, unpaid bills, overdrafts, loans, or debt arrangements may show on a credit file.

So, if you ask does Universal Credit affect credit score, the benefit itself is not the main issue. The real risk comes when a claimant cannot pay essential bills because their Universal Credit stops, drops, or arrives late.

Universal Credit is also not taxable. So, if you ask is UC taxable, the answer is no. Claimants do not pay income tax on Universal Credit.

For carers, this matters because financial stress can build quickly. Check payment dates, deductions, rent support, and journal messages early, especially if the claimant already struggles with bills, debt, or budgeting.

MORE: Wheelchair Parking Permit UK: Who Qualifies for a Blue Badge in 2026?

Severe Disability Premium and Universal Credit

Some claimants lost money when they moved from legacy benefits to Universal Credit, especially if their old award included a Severe Disability Premium. This issue matters because Severe Disability Premium gave extra support to some disabled people who lived alone, received a qualifying disability benefit, and did not have someone claiming Carer’s Allowance or the carer element for looking after them.

So, who qualifies for Severe Disability Premium Universal Credit? Universal Credit does not include Severe Disability Premium in the same way legacy benefits did. Instead, some people may receive transitional protection or a transitional element if they moved across under certain rules.

Carers should check the claimant’s old benefit letters, disability benefit awards, living situation, and Universal Credit migration history. Do not assume the award is correct just because DWP calculated it. If the claimant lost Severe Disability Premium after moving to Universal Credit, ask DWP to explain the calculation and whether any transitional protection applies.

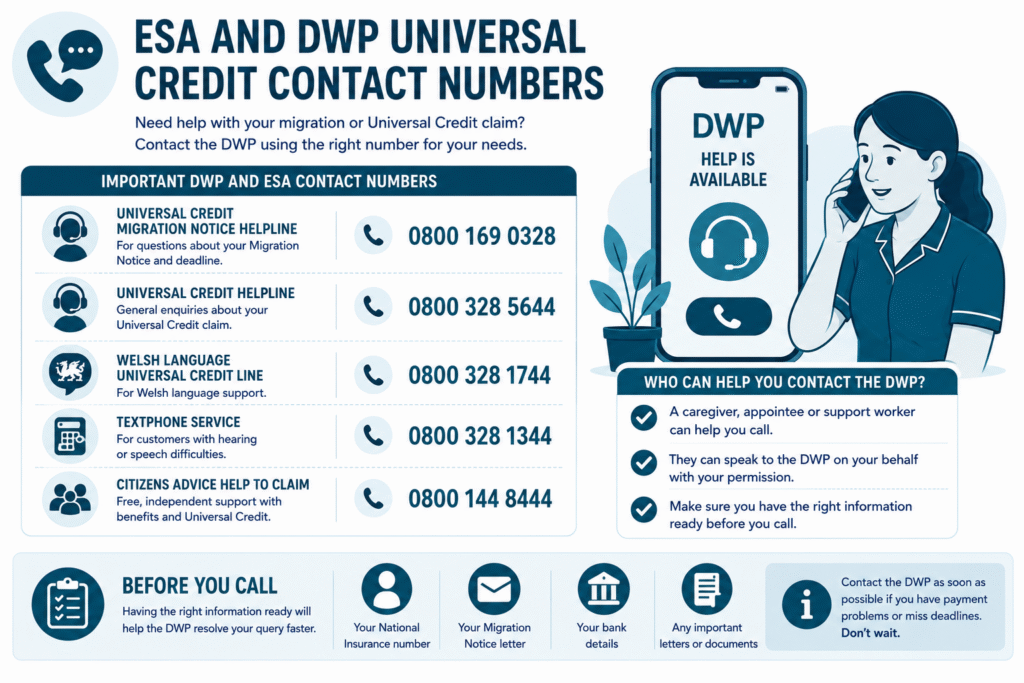

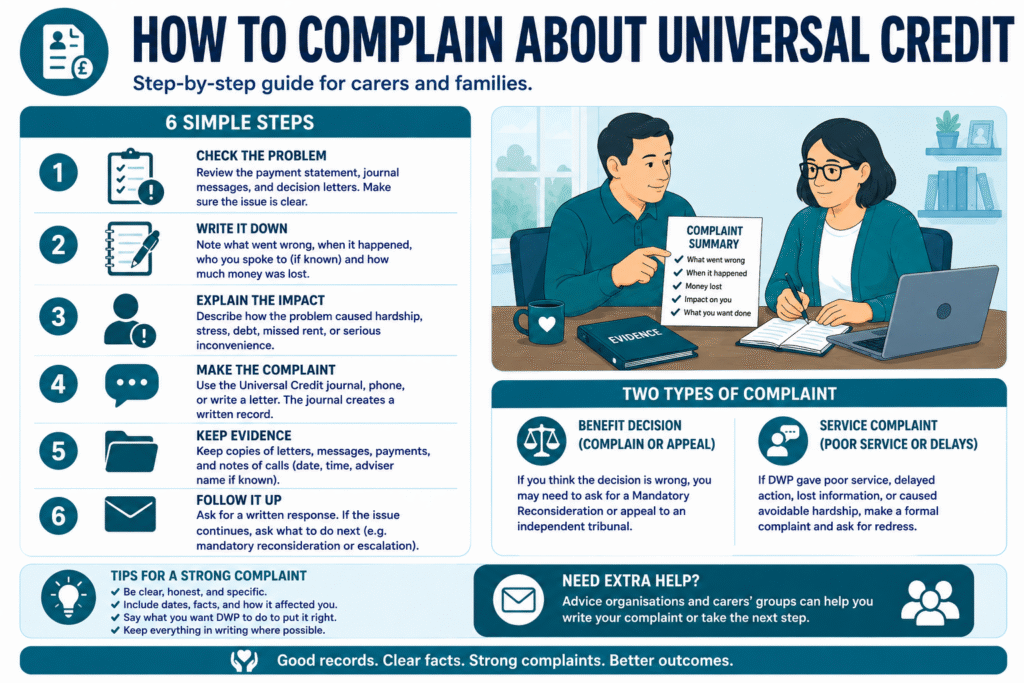

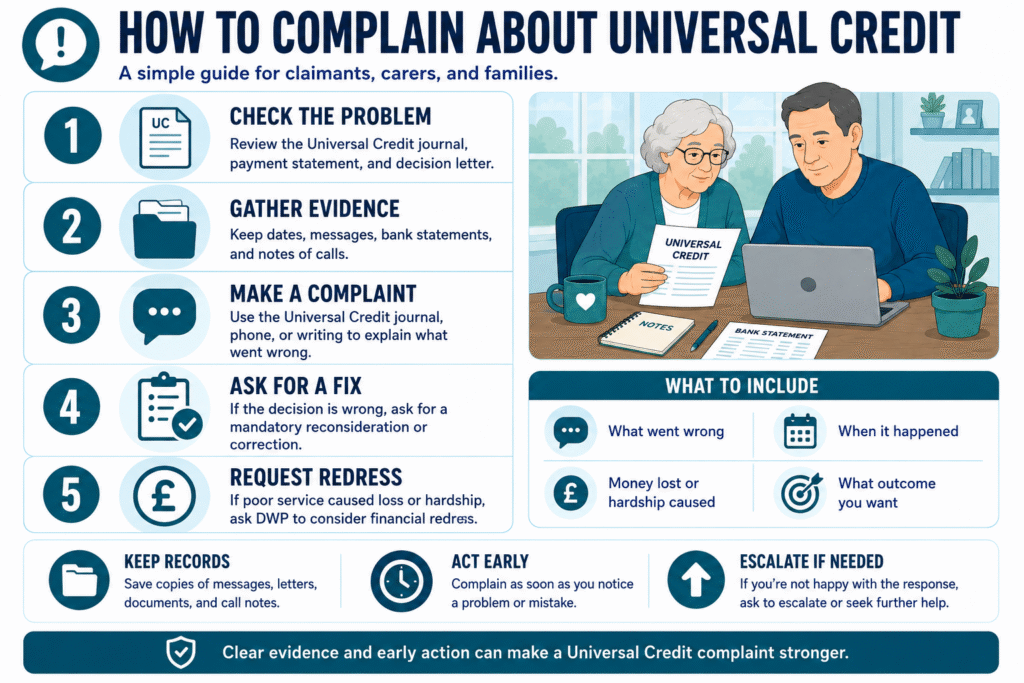

How to Complain About Universal Credit

If you believe DWP made a mistake or handled a Universal Credit claim badly, start by checking the payment statement, journal messages, and decision letters. Make sure the issue is clear before you complain.

To complain about Universal Credit, write down:

- what went wrong

- when it happened

- who you spoke to, if known

- how much money the claimant lost

- how the problem caused hardship, stress, debt, missed rent, or serious inconvenience

- what you want DWP to do next

You can complain through the Universal Credit journal, by phone, or in writing. Use the journal if the claimant can access their account, because it creates a written record. If you call, write down the date, time, and what the adviser said.

When asking how to complain about Universal Credit, remember this difference: if DWP made a wrong benefit decision, you may need a mandatory reconsideration or appeal. If DWP gave poor service, delayed action, lost information, or caused avoidable hardship, you can make a formal complaint and ask DWP to consider financial redress.

For a strong Universal Credit compensation DWP complaint, keep the message clear: explain the error, show the evidence, state the impact, and ask for a written response.

Final Thoughts…

If you support someone who struggles with forms, online accounts, phone calls, memory, disability, mental health, or complex paperwork, your help can make a real difference. Many Universal Credit problems become harder to fix when nobody checks the journal, reads decision letters, or challenges errors early.

Start with the basics. Check the claimant’s payment statement every month, keep copies of important messages, and write down dates when payments change. If something looks wrong, ask DWP to explain it clearly.

Do not ignore reduced payments, missing elements, unexplained deductions, or sudden changes after savings, earnings, PIP, pension payments, or compensation settlements. These issues can affect the claimant’s income quickly.

A strong Universal Credit compensation DWP complaint needs evidence, dates, and a clear explanation of the harm caused. As a carer or family member, your role is not to fight blindly. Your role is to organise the facts, protect the claimant’s wellbeing, and help them ask the right questions before the problem becomes a crisis.

Need Help Understanding Care and Benefit Decisions?

Universal Credit issues, DWP errors, and care costs can quickly affect a vulnerable person’s stability at home.

Care Sync Experts helps caregivers, families, and care providers make clearer, safer decisions around care, support, and household pressures.

Before problems grow, check the claimant’s payments, keep evidence, and act early.

Plan better support with practical, caregiver-focused guidance from Care Sync Experts.

FAQ

Will I lose benefits if I get compensation?

Not always. It depends on the type of compensation, how much money you receive, and whether the payment counts as savings or capital for means-tested benefits like Universal Credit.

Some compensation payments may receive special treatment if handled correctly, especially personal injury compensation placed into a trust. Always get welfare or legal advice before moving or spending a large compensation payment.

Who is eligible for Universal Credit in the UK?

To claim Universal Credit, a person usually needs to live in the UK, be on a low income or out of work, accept a claimant commitment, and have savings below the capital limit. Some students, carers, disabled people, self-employed workers, and people in work can also qualify depending on their circumstances.

How much can I earn and still get Universal Credit?

There is no single earnings limit because Universal Credit changes based on rent, children, disability elements, caring responsibilities, and the Universal Credit work allowance. Some people still receive Universal Credit while working full-time, while others may see their award reduce quickly as earnings rise.

Will Universal Credit know if I inherit money?

Yes, DWP expects claimants to report inheritance money because inheritance can affect means-tested benefits like Universal Credit.

If the inheritance pushes savings above the capital limit, the claimant’s award may reduce or stop. Carers and families should report changes quickly to avoid overpayments or future disputes.