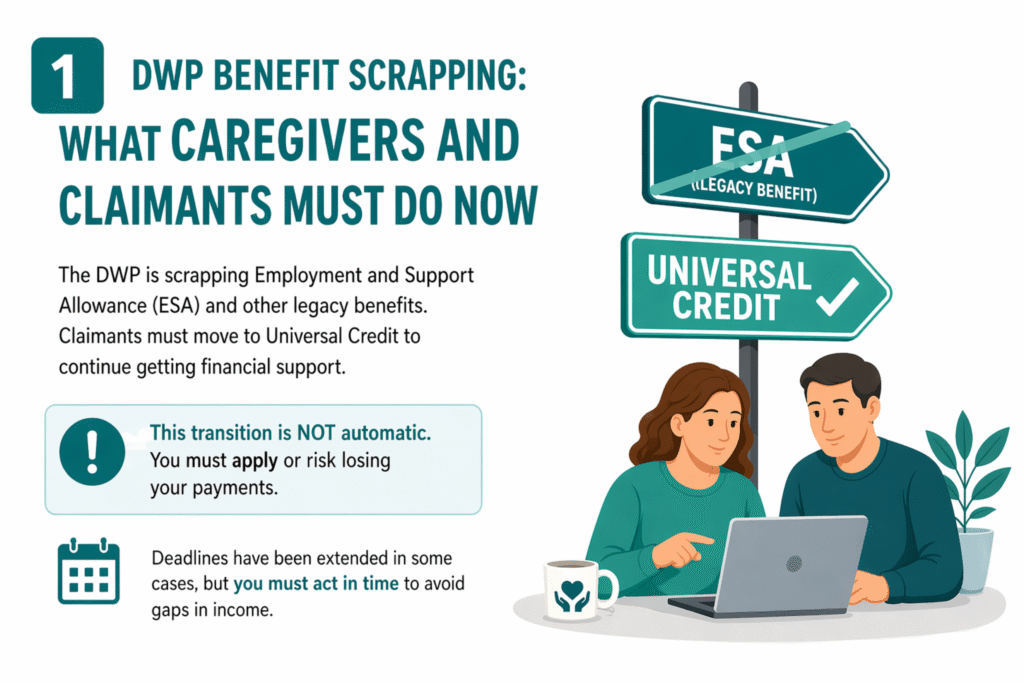

The Department for Work and Pensions (DWP) is scrapping Employment and Support Allowance (ESA) as part of a wider DWP benefit scrapping programme. Claimants must move to Universal Credit (UC) to continue receiving financial support, as the government phases out legacy benefits. This transition is not automatic; people must apply for Universal Credit or risk losing their payments.

The DWP has extended deadlines in some cases to support vulnerable claimants, but the responsibility still falls on individuals and caregivers to act in time. Care providers should identify clients receiving ESA and guide them through the transition early to avoid disruptions in income.

While this reform focuses on ESA, it also signals broader welfare changes. Many families are now asking whether other policies, such as the two child benefit cap, will also change under ongoing government reviews.

Key Takeaways

- The DWP is phasing out ESA as part of a wider DWP benefit scrapping programme

- Universal Credit will replace legacy benefits, but the switch is not automatic

- Claimants must apply on time or risk losing their payments completely

- Caregivers and care providers must actively support vulnerable clients through the transition

- Deadlines have been extended in some cases, but delays still carry financial risks

- Wider welfare reforms, including the two child benefit cap, remain under review and may affect families on Universal Credit

What DWP Benefit Scrapping Means for Care Providers and Families

The current wave of DWP benefit scrapping is not just a policy change; it directly affects how caregivers support vulnerable people every day.

If you run a care agency or support clients on ESA, you now carry a bigger responsibility. You must identify which clients still receive legacy benefits and help them transition to Universal Credit before deadlines pass. Many clients, especially elderly or disabled individuals, do not fully understand the process or may assume payments will continue automatically.

For families, the impact can be immediate. A missed application can stop income entirely. That creates stress, increases dependency on care providers, and can even affect a person’s ability to afford basic needs like housing, food, and medication.

Care providers must also prepare for increased workload. You may need to:

- Explain benefit changes in simple terms

- Help clients gather documents

- Support online applications

- Follow up on claims and deadlines

This shift also connects to wider welfare concerns. Families already dealing with limits like the 2 child cap UK rules may face additional financial pressure as benefits change. When combined with ongoing uncertainty around policies like the two child benefit cap, the risk of financial instability grows.

In short, DWP benefit scrapping turns caregivers into frontline support for both care and financial guidance. Acting early protects your clients and reduces crisis situations later.

RELATED: Scotland PIP ADP Update 2026: What Care Businesses and Claimants Must Know

Why ESA and Other Legacy Benefits Are Being Scrapped

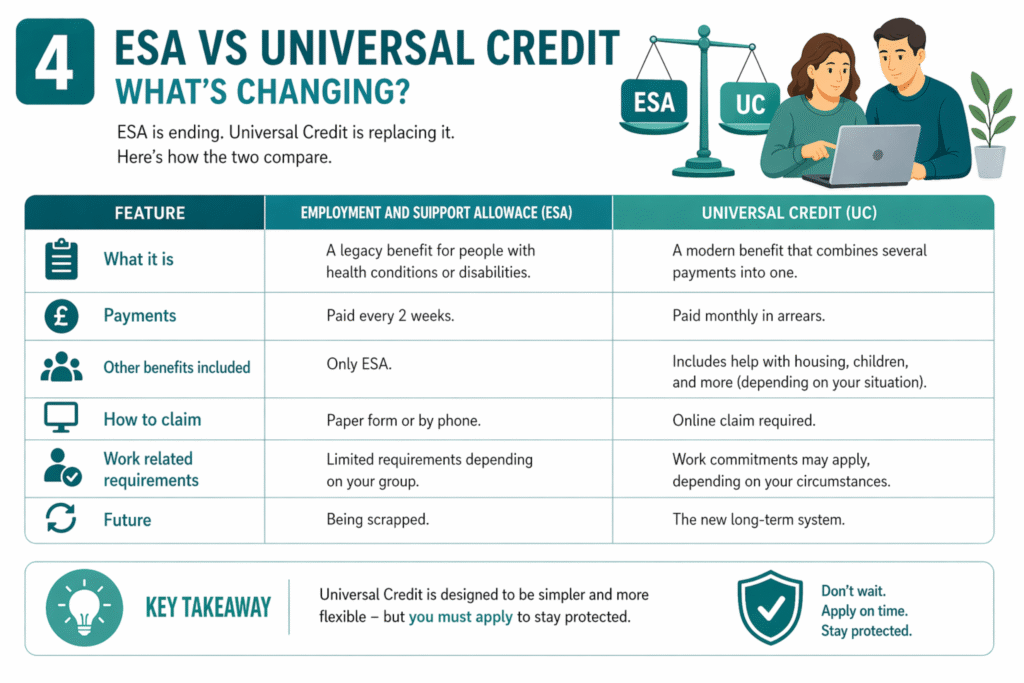

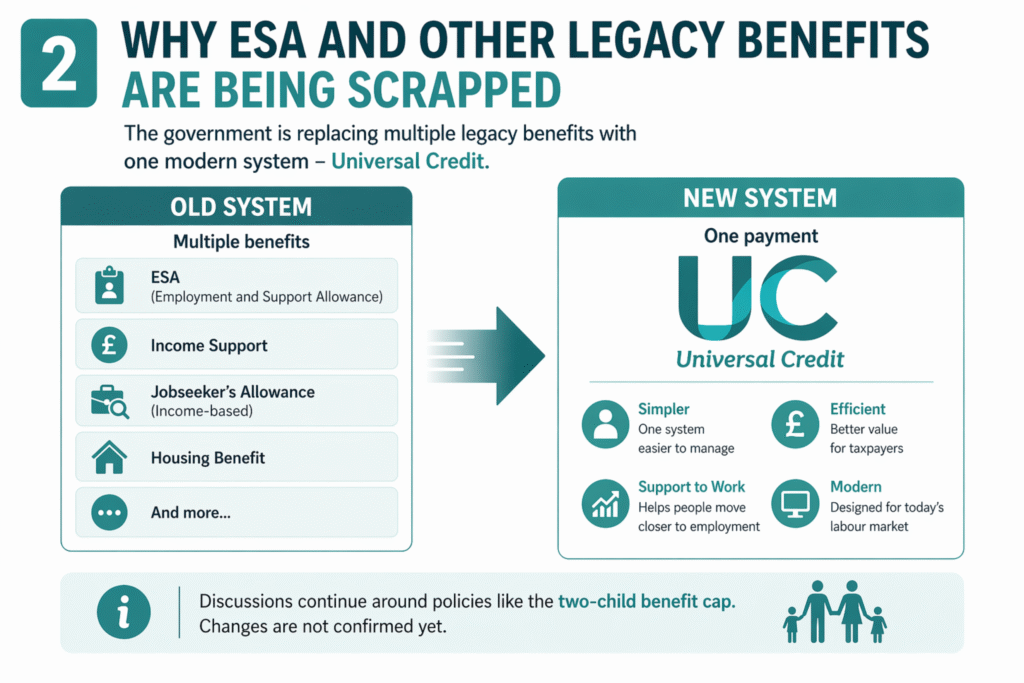

The DWP is scrapping ESA and other legacy benefits to replace them with a single system: Universal Credit. This move forms a key part of the wider DWP benefit scrapping programme aimed at simplifying welfare and encouraging people to move closer to work where possible.

Universal Credit combines several older benefits, including ESA, Income Support, and income-based Jobseeker’s Allowance, into one monthly payment. The government argues that this system better reflects today’s labour market and provides clearer pathways into employment.

Universal Credit is designed to replace multiple legacy benefits with a single payment that adjusts based on income, employment status, and personal circumstances.

From a policy standpoint, the goal is efficiency. Instead of managing several separate benefits, the DWP wants one streamlined system that is easier to administer and monitor. However, for many claimants and caregivers, the transition creates confusion and risk, especially because the process requires action.

This change also raises broader questions about the future of welfare limits. Many families now ask whether policies like the two-child benefit cap will change alongside these reforms. While discussions continue, particularly around whether the two-child benefit cap will be lifted or adjusted under future budgets, no universal change has been confirmed yet.

For now, the priority remains clear: ESA is ending, and Universal Credit is replacing it. Care providers must treat this as an active transition, not a passive update.

What You Must Do Before ESA Is Scrapped

If you or someone you support still receives ESA, you must act now. The DWP will not move you automatically. You must apply for Universal Credit before your deadline to keep receiving financial support.

The move to Universal Credit is not automatic. Claimants must apply or risk losing their payments completely.

Follow these steps to stay protected:

- Check eligibility immediately

Confirm whether you receive income-related ESA or another legacy benefit being replaced - Watch for official DWP letters

The DWP sends a migration notice with a deadline to apply - Apply for Universal Credit early

Do not wait until the last minute—processing delays can affect payments - Prepare required information

Gather ID, bank details, housing costs, and medical evidence if needed - Seek support if needed

Care providers, local councils, and support organisations can guide you through the process

For caregivers, this step is critical. Many vulnerable clients may ignore letters, misunderstand instructions, or struggle with online applications. You should actively monitor their situation and assist with submissions to prevent missed deadlines.

This transition also connects to wider concerns about benefit limits. Families moving to Universal Credit often ask whether policies like the two child benefit cap will change or whether the benefit cap is being lifted on Universal Credit. While these questions remain under review, they do not affect the immediate requirement to apply.

Act early, stay organised, and ensure every affected claimant completes their application before the deadline.

READ MORE: What is the Work Capability Assessment? 2026 Update for Care Businesses

What Happens If You Don’t Move to Universal Credit

If a claimant does not switch in time, the DWP will stop their ESA payments. The system does not transfer benefits automatically, and missing the deadline can leave people without income.

If you do not apply for Universal Credit before your deadline, your ESA payments will end and you may not receive backdated support.

This situation creates serious risks, especially for vulnerable individuals. Without a successful application:

- Monthly income stops completely

- Housing payments may be affected

- Bills and essential costs become harder to manage

- Reapplying later can cause delays and financial gaps

For caregivers, this is where proactive support matters most. You must not assume clients will act on their own. Many people miss deadlines because they:

- Ignore DWP letters

- Do not understand the process

- Struggle with digital applications

From a wider perspective, these risks add to existing financial pressure on families already affected by limits like the 2 child cap UK rules. Questions such as “is the benefit cap being lifted for everyone?” or whether support will increase do not change the immediate reality, missing the migration deadline leads to lost payments.

Acting early prevents crisis. Waiting increases the chance of financial hardship.

Will the Two-Child Benefit Cap Be Scrapped in 2026? Latest Updates

The current wave of DWP benefit scrapping has pushed more families to ask a bigger question:

Will the two-child benefit cap be scrapped in 2026?

Right now, the policy remains in place. The two child benefit cap limits financial support to the first two children in most households claiming benefits like Universal Credit. Families with more than two children do not receive additional payments for extra children under this rule.

The two-child benefit cap restricts Universal Credit and tax credit payments to a maximum of two children in most cases.

Recent discussions, especially around the autumn budget 2025 2 child cap and political debates involving figures like Rachel Reeves child benefit cap proposals—have increased expectations that the policy could change. Some reports suggest a possible UK two-child limit abolition, but no confirmed timeline exists.

Here’s what we know so far:

- The policy is still active across the UK

- No official confirmation of a full removal yet

- Ongoing debate continues within government and policy circles

- Any change would likely come through a future budget announcement

Many families also search for:

- “when will the 2 child benefit cap be scrapped”

- “when does the 2 child cap end”

- “two-child benefit cap scrapped”

At this stage, these remain unanswered. No confirmed date has been announced.

For caregivers, this matters because families transitioning to Universal Credit may expect increased support that does not yet exist. Managing expectations is critical. You should clearly explain that while discussions continue, the policy still applies today.

In short, while the two-child benefit cap will be lifted remains a possibility in future reforms, caregivers and claimants must plan based on current rules, not speculation.

SEE ALSO: What is a Discretionary Housing Payment? 2026 Update for Care Business

2 Child Benefit Cap Lifted: How Much Will Families Get?

Many families moving to Universal Credit ask the same question: “If the 2 child benefit cap is lifted, how much will I get?”

Right now, there is no confirmed change. The two-child benefit cap still limits payments to the first two children in most households. That means families do not receive additional Universal Credit amounts for a third or subsequent child under current rules.

If the two-child benefit cap is lifted, eligible families would receive additional Universal Credit payments for each extra child, increasing their total monthly income.

To understand the impact, here’s what would change if the policy were removed:

- Families with more than two children would qualify for extra child elements under Universal Credit

- Monthly payments would increase based on the number of additional children

- Financial pressure on larger families would reduce significantly

For example, when people search:

- “2 child benefit cap lifted how much will I get”

- “2 child benefit cap lifted how much will I get universal credit”

They are trying to estimate how much extra support they could receive. While exact figures depend on individual circumstances, each additional child element in Universal Credit is worth thousands of pounds per year. Removing the cap would therefore create a meaningful increase in household income.

However, it’s important to stay grounded in current policy. There is no automatic payment or confirmed rollout yet. Questions like “will the 2 child benefit cap be automatically paid” or “will the 2 child benefit cap be backdated” remain speculative.

For caregivers and support workers, this is where clear communication matters. Many clients may expect immediate financial relief due to ongoing debates or media headlines. You must explain that:

- The cap is still in place today

- No confirmed payment increase has been announced

- Any future change would likely require a formal policy update

Until then, families should plan based on existing Universal Credit rules, not future expectations.

MORE: What Is an Enhanced DBS CRB Check? 2026 Update for Care Homes

Care Provider Checklist: How to Support Clients Through Benefit Changes

Care providers play a critical role during this period of DWP benefit scrapping. You are often the first point of support when clients feel confused, overwhelmed, or at risk of losing income.

Use this checklist to stay proactive and protect your clients:

- Identify At-Risk Clients

Review your records and flag anyone receiving ESA or other legacy benefits. Prioritise clients with disabilities, limited digital skills, or no family support.

- Communicate Early and Clearly

Explain the changes in simple terms. Tell clients:

- ESA is ending

- They must apply for Universal Credit

- Missing deadlines can stop payments

Avoid assumptions, many clients do not understand official letters.

- Support the Application Process

Help clients:

- Create Universal Credit accounts

- Upload required documents

- Complete identity checks

Where possible, sit with them during the application to avoid errors.

- Track Deadlines and Follow Up

Set reminders for each client’s migration deadline. Check progress regularly and confirm that applications have been submitted successfully.

- Manage Expectations Around Policy Changes

Clients may ask about:

- “when will the two child benefit cap be lifted”

- “two-child benefit cap removed”

- “is child benefit going up”

Be clear: these changes are not confirmed yet. Focus clients on what they must do now, not what might happen later.

- Monitor Financial Stability

Watch for early signs of financial stress:

- Missed rent

- Reduced food spending

- Anxiety about bills

Step in early and connect clients with additional support if needed.

- Stay Updated on Policy Changes

Welfare rules continue to evolve. Follow updates on:

- Universal Credit changes

- Potential reforms like the 2 child cap

- Budget announcements affecting benefits

By following this checklist, you move from reactive support to proactive care. You protect your clients from sudden income loss, and strengthen your role as a trusted guide during uncertain policy changes.

Conclusion

The current wave of DWP benefit scrapping is already changing how caregivers support clients across the UK. ESA is ending, Universal Credit is replacing it, and the transition requires action, not assumptions.

For care providers, this is more than a policy update. It directly affects your clients’ financial stability, well-being, and trust in your service. Acting early, guiding clearly, and staying informed will prevent avoidable crises.

At the same time, wider reforms, like ongoing debates around the two-child benefit cap, continue to shape expectations. But until confirmed, the priority remains simple: help every affected client complete their transition on time.

Support your clients through benefit changes, without delays or mistakes.

Care Sync Experts helps you manage applications, compliance, and updates with confidence.

FAQ

Can DWP check your bank account?

The DWP does not routinely monitor your bank account, but it can request access to financial information if it suspects fraud or needs to verify a claim. In some cases, they may work with banks or use data-sharing powers to confirm income and savings.

Can the DWP just stop my benefits?

Yes, the DWP can stop your benefits if you fail to meet eligibility rules, miss a required action (like moving to Universal Credit), or do not respond to official requests. Payments can also stop if your circumstances change and you do not report it.

What triggers a DWP bank check?

A bank check may be triggered by:

Suspected fraud or incorrect claims

– Unreported income or savings

– Data mismatches between government systems

– Random compliance reviews

Keeping your information accurate and up to date reduces the risk of checks.

Will I lose my PIP if I inherit money?

No, inheriting money does not automatically stop Personal Independence Payment (PIP). PIP is not means-tested, so it does not depend on your savings or income. However, if your condition improves or your circumstances change, the DWP may review your claim.

Leave a Reply