Rachel Reeves has defended proposed changes to the UK welfare system that could tighten access to disability-related benefits, including Personal Independence Payment (PIP). The planned reforms focus on reviewing eligibility criteria for claimants, with ministers arguing that the current system no longer supports long-term economic sustainability.

The debate around Rachel Reeves disability reforms has intensified because many disabled people and caregivers rely on PIP to cover daily living costs, mobility support, and essential care needs.

Campaigners and disability advocates fear the proposed Rachel Reeves disability cuts could reduce financial support for vulnerable households and place additional pressure on unpaid caregivers and care providers.

Although Labour has not confirmed every detail of the reforms, Rachel Reeves disability benefit proposals have already triggered national discussion about fairness, healthcare access, and the future of disability support in the UK.

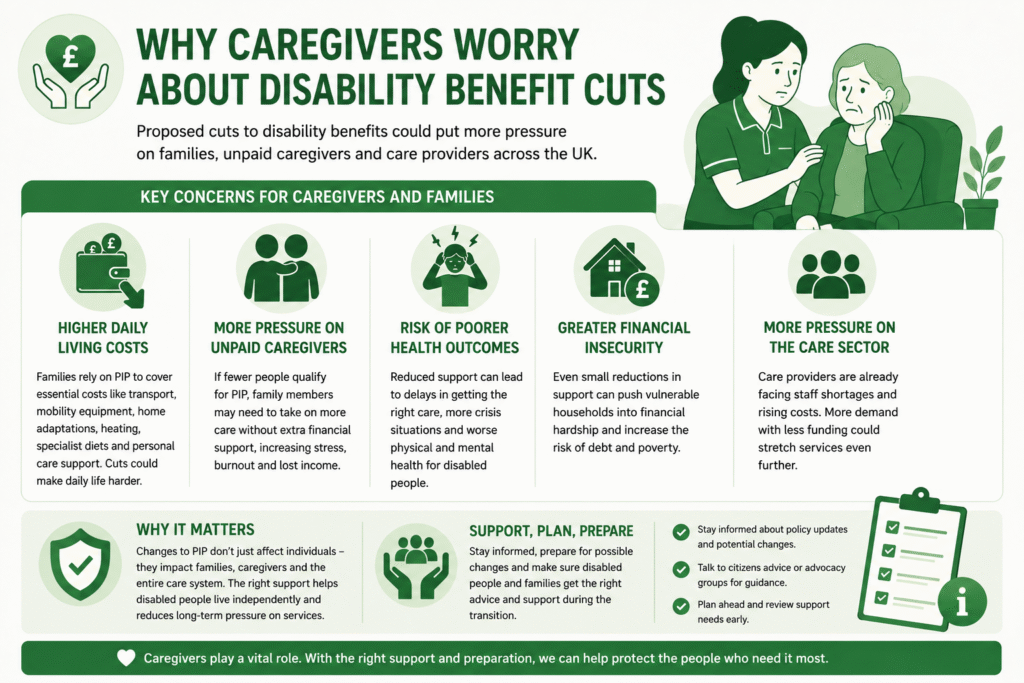

Many caregivers worry that the proposed Rachel Reeves disability benefit cuts could make daily life harder for disabled people who already struggle with rising living costs.

Families often use disability benefits to pay for transport, mobility equipment, home adjustments, heating, specialist diets, and personal care support. Even small reductions in support can create major disruptions for vulnerable households.

Care providers also fear that tighter eligibility rules could increase pressure on unpaid family caregivers. If fewer people qualify for PIP, relatives may need to take on more caring responsibilities without additional financial support.

That shift could increase emotional burnout, reduce household income, and affect the quality of care disabled people receive at home.

The latest Rachel Reeves disability news has also raised concerns across the social care sector because many providers already operate under staffing shortages and funding pressures.

Some caregivers believe the proposed reforms may push more people toward crisis support services instead of preventive care, increasing long-term pressure on the NHS and local authorities.

How Changes to PIP Could Affect Disabled People and Care Providers

Potential changes to Rachel Reeves disability PIP policies could affect far more than monthly benefit payments. Many disabled people use PIP to maintain independence, access transport, and continue living safely in their communities.

If the government tightens eligibility criteria, some claimants could lose access to financial support that helps cover mobility and daily living needs.

Concerns around Rachel Reeves disability cars discussions have also grown because thousands of disabled people rely on the Motability scheme for accessible transport.

Losing PIP eligibility could prevent some individuals from qualifying for Motability vehicles, making it harder to attend medical appointments, work, education, or social activities.

Care providers may also feel the impact quickly. Reduced financial support often increases demand for local care services, emergency support, and unpaid family care.

Home care agencies and community support workers could face higher caseloads as more families struggle to manage complex care needs without adequate funding.

What Rachel Reeves and Labour Have Said About Disability Reforms

Rachel Reeves Disability Benefits? 2026 Update

Rachel Reeves has defended the government’s approach by arguing that the welfare system needs reform to remain financially sustainable. Labour ministers say the current system does not effectively support people back into work and that the number of disability benefit claims has increased significantly since the pandemic.

Recent Rachel Reeves disability news coverage has focused on proposed changes to Personal Independence Payment assessments, particularly around stricter qualification criteria.

Reeves has stated that the government continues to review the rules for accessing PIP and may still adjust parts of the proposal following criticism from Labour MPs, disability groups, and campaigners.

Supporters of the reforms argue that Labour wants to balance financial responsibility with long-term support for vulnerable people.

Critics, however, believe the Rachel Reeves budget disability proposals could place disabled households under additional financial strain during an already difficult economic period.

Why Campaigners and Disability Advocates Oppose the Proposed Changes

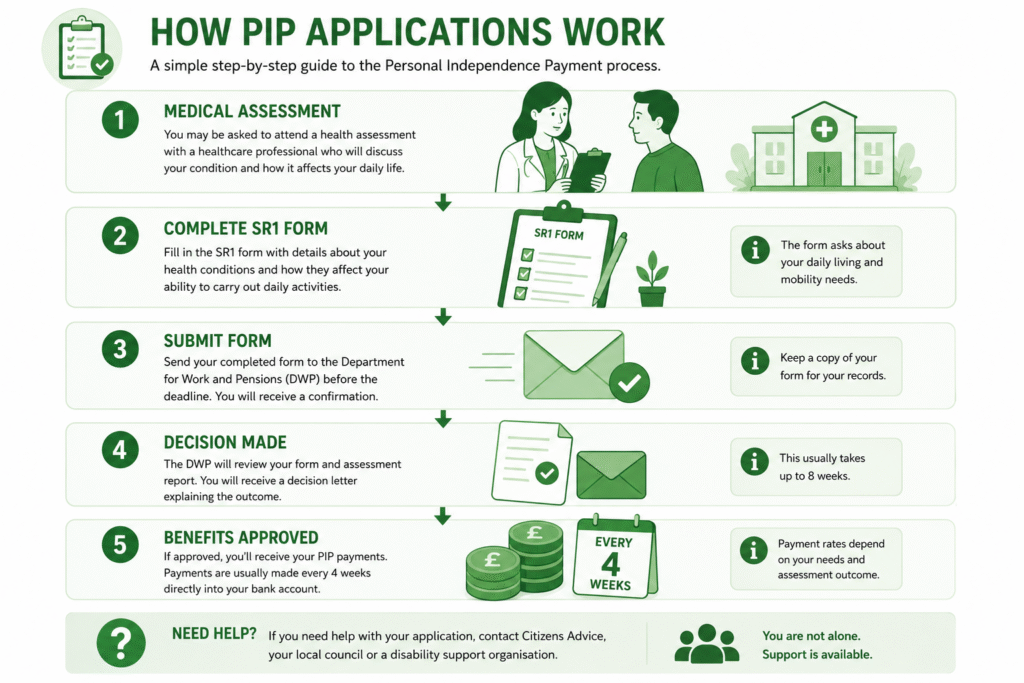

How PIP applications work

Disability campaigners and advocacy groups strongly oppose the proposed reforms because they believe the changes could reduce independence and financial security for disabled people.

Many critics argue that tighter eligibility rules may unfairly affect people with invisible illnesses, mental health conditions, and fluctuating disabilities that already prove difficult to assess through the current system.

Advocates also warn that reducing access to PIP could increase poverty levels among vulnerable households. Many disabled people depend on disability benefits to cover additional living costs that non-disabled households may not face, including specialist transport, medical equipment, higher utility bills, and personal support services.

Some campaigners have linked the wider public reaction to growing frustration around Labour’s welfare direction, especially as online discussions continue around questions like “will Rachel Reeves resign” and “why is Rachel Reeves crying.”

While those conversations often reflect broader political tensions, disability organizations continue to focus mainly on the long-term impact the reforms could have on disabled people and caregivers across the UK.

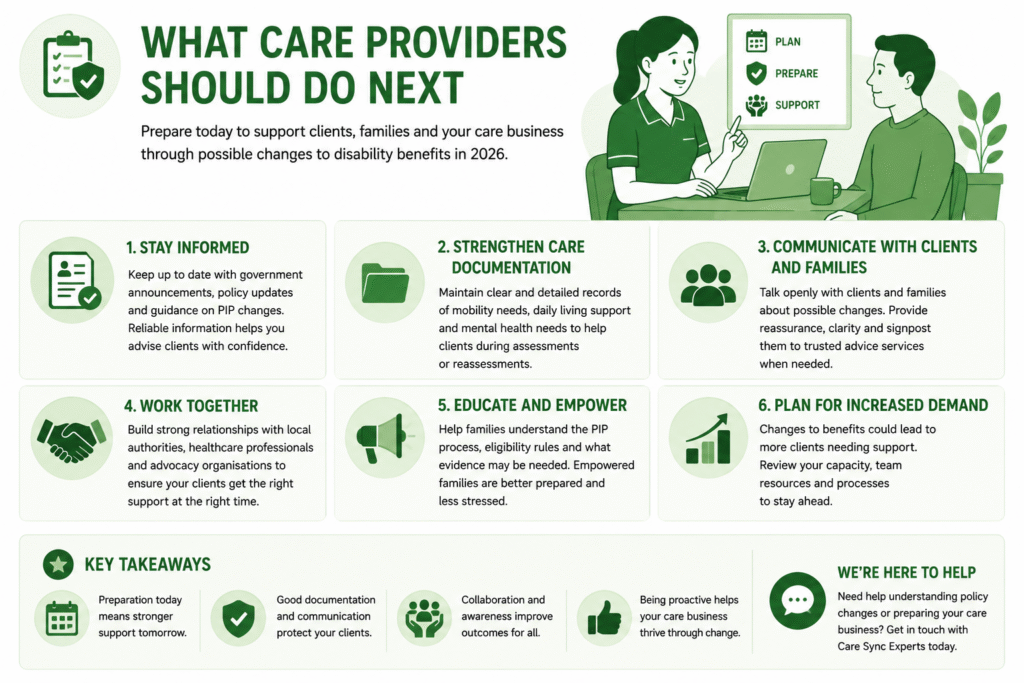

Care providers should prepare early for possible changes to disability benefit assessments and eligibility rules. Many families may need additional guidance if the government introduces new PIP requirements or reassessment processes in 2026.

Providers who stay informed and communicate clearly with clients will place themselves in a stronger position to offer support during periods of uncertainty.

Home care agencies and support workers should also strengthen care documentation and maintain accurate client records. Clear evidence of mobility challenges, daily living needs, and mental health support can help families during benefit reviews or reassessments.

Providers may also need to work more closely with local authorities, advocacy groups, and healthcare professionals as demand for support services increases.

Caregiver businesses can also play an important role by educating families about policy updates, signposting trusted advice services, and helping vulnerable clients avoid unnecessary stress during the ongoing Rachel Reeves disability debate.

Conclusion

The debate around Rachel Reeves disability reforms has become one of the most closely watched welfare discussions in the UK. While Labour argues that changes to disability benefits aim to create a more sustainable welfare system, many caregivers, disabled people, and advocacy groups remain concerned about the possible impact on financial stability, independence, and access to care.

For care providers, the conversation goes beyond politics. Any major change to PIP or disability support could directly affect families, unpaid caregivers, and frontline care services already working under pressure.

Providers who stay informed, support vulnerable clients, and prepare for possible policy changes will place themselves in a stronger position to respond effectively in 2026.

At Care Sync Experts, we help caregiver businesses stay ahead of regulatory, operational, and industry changes affecting the UK care sector.

From compliance support and tender guidance to policy-focused insights for care providers, our team works closely with organizations that want to grow sustainably while delivering high-quality care.

FAQ

Is Parkinson’s considered a disability in the UK?

Yes. Parkinson’s disease can qualify as a disability in the UK if it significantly affects a person’s ability to complete daily activities or move independently. Many people living with Parkinson’s may qualify for support such as Personal Independence Payment (PIP), depending on how the condition impacts their everyday life.

Is arthritis a disability?

Arthritis may qualify as a disability when it causes long-term physical limitations, chronic pain, or mobility difficulties that affect normal daily activities. Severe arthritis often impacts a person’s ability to work, walk, dress, cook, or manage personal care without support.

What are the top 3 disabilities?

The most commonly reported disabilities often include mobility impairments, mental health conditions, and musculoskeletal disorders such as arthritis or chronic back pain. However, disability experiences vary widely, and many conditions can affect people differently depending on severity and support needs.

What actor has Down syndrome?

Several actors with Down syndrome have gained recognition in film and television. One well-known example is Zack Gottsagen, who starred in The Peanut Butter Falcon. In the UK entertainment industry, actors and advocates with Down syndrome continue to help improve disability representation in media and public life.

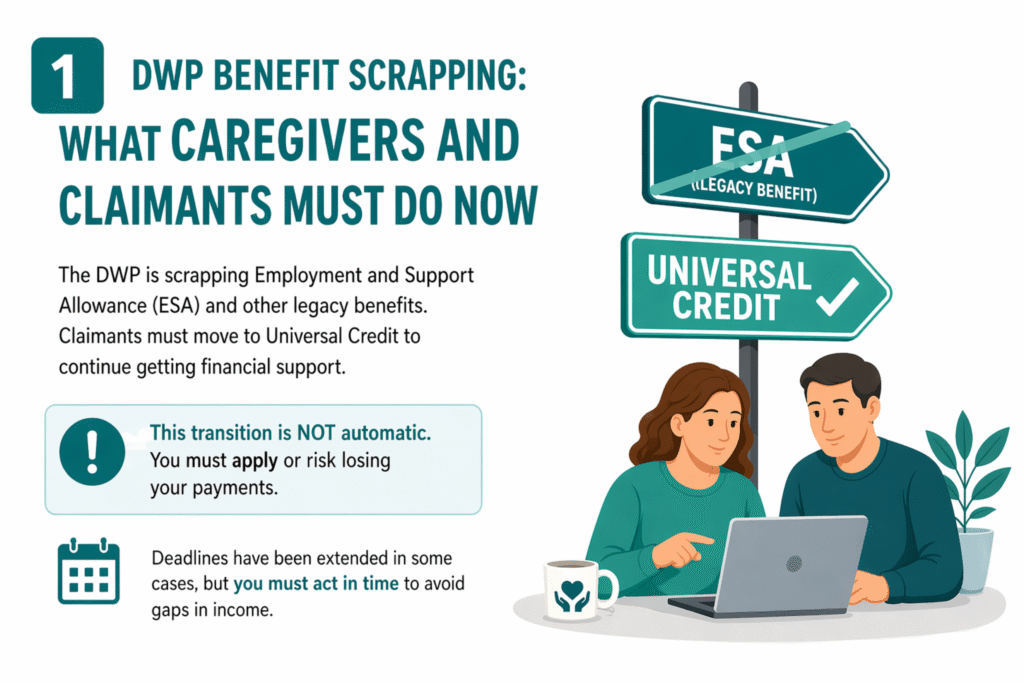

The Department for Work and Pensions (DWP) is scrapping Employment and Support Allowance (ESA) as part of a wider DWP benefit scrapping programme. Claimants must move to Universal Credit (UC) to continue receiving financial support, as the government phases out legacy benefits. This transition is not automatic; people must apply for Universal Credit or risk losing their payments.

The DWP has extended deadlines in some cases to support vulnerable claimants, but the responsibility still falls on individuals and caregivers to act in time. Care providers should identify clients receiving ESA and guide them through the transition early to avoid disruptions in income.

While this reform focuses on ESA, it also signals broader welfare changes. Many families are now asking whether other policies, such as the two child benefit cap, will also change under ongoing government reviews.

The current wave of DWP benefit scrapping is not just a policy change; it directly affects how caregivers support vulnerable people every day.

If you run a care agency or support clients on ESA, you now carry a bigger responsibility. You must identify which clients still receive legacy benefits and help them transition to Universal Credit before deadlines pass. Many clients, especially elderly or disabled individuals, do not fully understand the process or may assume payments will continue automatically.

For families, the impact can be immediate. A missed application can stop income entirely. That creates stress, increases dependency on care providers, and can even affect a person’s ability to afford basic needs like housing, food, and medication.

Care providers must also prepare for increased workload. You may need to:

Explain benefit changes in simple terms

Help clients gather documents

Support online applications

Follow up on claims and deadlines

This shift also connects to wider welfare concerns. Families already dealing with limits like the 2 child cap UK rules may face additional financial pressure as benefits change. When combined with ongoing uncertainty around policies like the two child benefit cap, the risk of financial instability grows.

In short, DWP benefit scrapping turns caregivers into frontline support for both care and financial guidance. Acting early protects your clients and reduces crisis situations later.

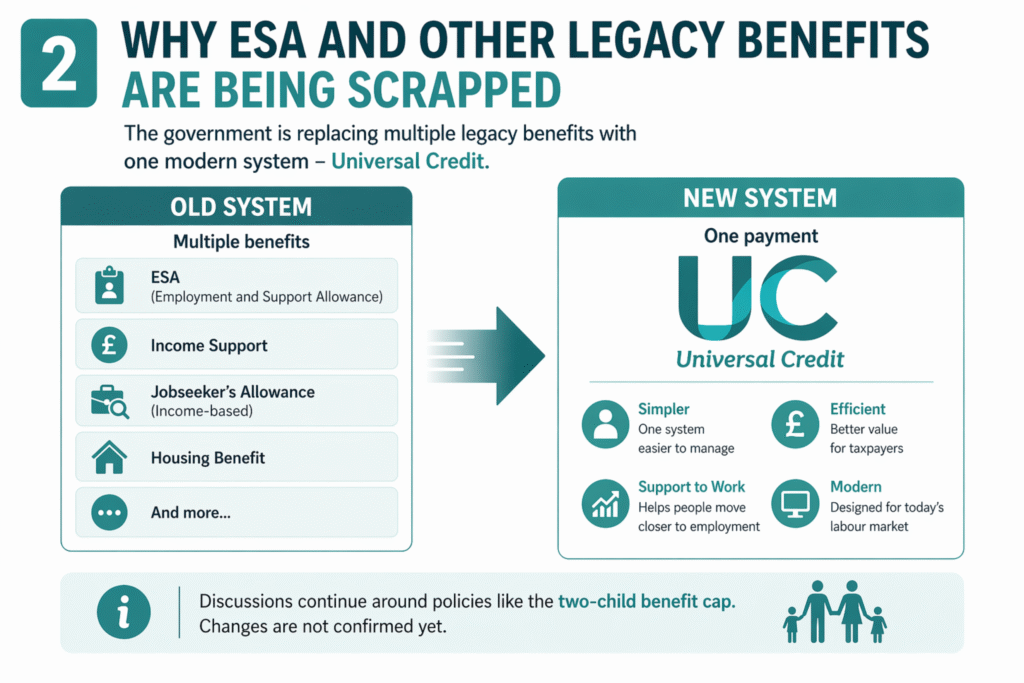

Why ESA and Other Legacy Benefits Are Being Scrapped

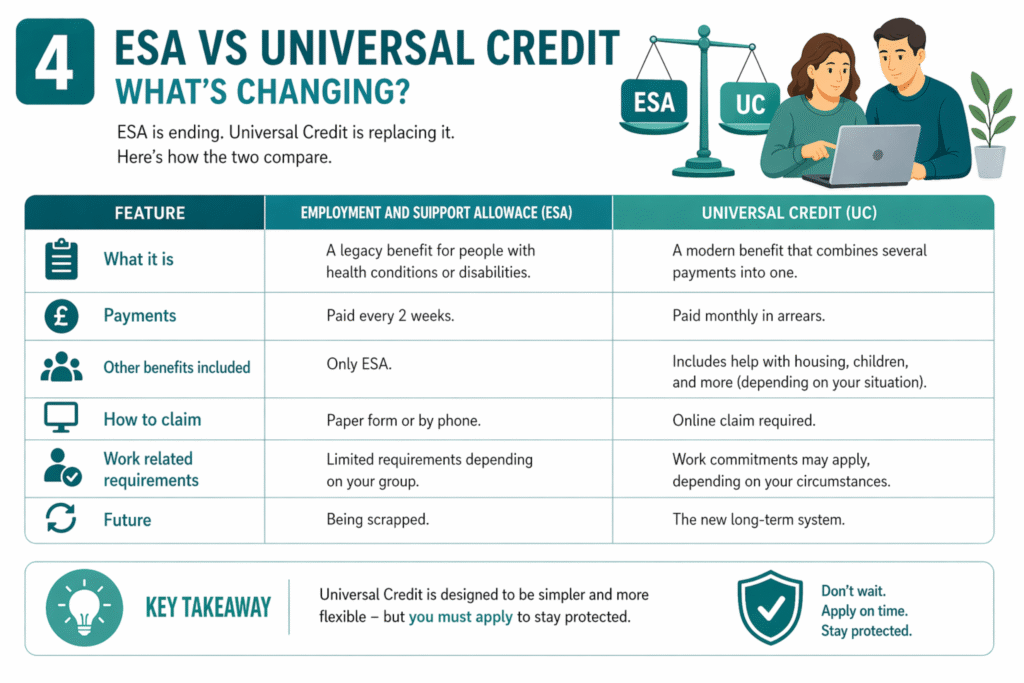

The DWP is scrapping ESA and other legacy benefits to replace them with a single system: Universal Credit. This move forms a key part of the wider DWP benefit scrapping programme aimed at simplifying welfare and encouraging people to move closer to work where possible.

Universal Credit combines several older benefits, including ESA, Income Support, and income-based Jobseeker’s Allowance, into one monthly payment. The government argues that this system better reflects today’s labour market and provides clearer pathways into employment.

Universal Credit is designed to replace multiple legacy benefits with a single payment that adjusts based on income, employment status, and personal circumstances.

From a policy standpoint, the goal is efficiency. Instead of managing several separate benefits, the DWP wants one streamlined system that is easier to administer and monitor. However, for many claimants and caregivers, the transition creates confusion and risk, especially because the process requires action.

This change also raises broader questions about the future of welfare limits. Many families now ask whether policies like the two-child benefit cap will change alongside these reforms. While discussions continue, particularly around whether the two-child benefit cap will be lifted or adjusted under future budgets, no universal change has been confirmed yet.

For now, the priority remains clear: ESA is ending, and Universal Credit is replacing it. Care providers must treat this as an active transition, not a passive update.

What You Must Do Before ESA Is Scrapped

Checklist Before ESA transitions

If you or someone you support still receives ESA, you must act now. The DWP will not move you automatically. You must apply for Universal Credit before your deadline to keep receiving financial support.

The move to Universal Credit is not automatic. Claimants must apply or risk losing their payments completely.

Follow these steps to stay protected:

Check eligibility immediately Confirm whether you receive income-related ESA or another legacy benefit being replaced

Watch for official DWP letters The DWP sends a migration notice with a deadline to apply

Apply for Universal Credit early Do not wait until the last minute—processing delays can affect payments

Prepare required information Gather ID, bank details, housing costs, and medical evidence if needed

Seek support if needed Care providers, local councils, and support organisations can guide you through the process

For caregivers, this step is critical. Many vulnerable clients may ignore letters, misunderstand instructions, or struggle with online applications. You should actively monitor their situation and assist with submissions to prevent missed deadlines.

This transition also connects to wider concerns about benefit limits. Families moving to Universal Credit often ask whether policies like the two child benefit cap will change or whether the benefit cap is being lifted on Universal Credit. While these questions remain under review, they do not affect the immediate requirement to apply.

Act early, stay organised, and ensure every affected claimant completes their application before the deadline.

What Happens If You Don’t Move to Universal Credit

If a claimant does not switch in time, the DWP will stop their ESA payments. The system does not transfer benefits automatically, and missing the deadline can leave people without income.

If you do not apply for Universal Credit before your deadline, your ESA payments will end and you may not receive backdated support.

This situation creates serious risks, especially for vulnerable individuals. Without a successful application:

Monthly income stops completely

Housing payments may be affected

Bills and essential costs become harder to manage

Reapplying later can cause delays and financial gaps

For caregivers, this is where proactive support matters most. You must not assume clients will act on their own. Many people miss deadlines because they:

Ignore DWP letters

Do not understand the process

Struggle with digital applications

From a wider perspective, these risks add to existing financial pressure on families already affected by limits like the 2 child cap UK rules. Questions such as “is the benefit cap being lifted for everyone?” or whether support will increase do not change the immediate reality, missing the migration deadline leads to lost payments.

Acting early prevents crisis. Waiting increases the chance of financial hardship.

Will the Two-Child Benefit Cap Be Scrapped in 2026? Latest Updates

dwp benefit changes

The current wave of DWP benefit scrapping has pushed more families to ask a bigger question: Will the two-child benefit cap be scrapped in 2026?

Right now, the policy remains in place. The two child benefit cap limits financial support to the first two children in most households claiming benefits like Universal Credit. Families with more than two children do not receive additional payments for extra children under this rule.

The two-child benefit cap restricts Universal Credit and tax credit payments to a maximum of two children in most cases.

Recent discussions, especially around the autumn budget 2025 2 child cap and political debates involving figures like Rachel Reeves child benefit cap proposals—have increased expectations that the policy could change. Some reports suggest a possible UK two-child limit abolition, but no confirmed timeline exists.

Here’s what we know so far:

The policy is still active across the UK

No official confirmation of a full removal yet

Ongoing debate continues within government and policy circles

Any change would likely come through a future budget announcement

Many families also search for:

“when will the 2 child benefit cap be scrapped”

“when does the 2 child cap end”

“two-child benefit cap scrapped”

At this stage, these remain unanswered. No confirmed date has been announced.

For caregivers, this matters because families transitioning to Universal Credit may expect increased support that does not yet exist. Managing expectations is critical. You should clearly explain that while discussions continue, the policy still applies today.

In short, while the two-child benefit cap will be lifted remains a possibility in future reforms, caregivers and claimants must plan based on current rules, not speculation.

2 Child Benefit Cap Lifted: How Much Will Families Get?

dwp benefit scrapping

Many families moving to Universal Credit ask the same question: “If the 2 child benefit cap is lifted, how much will I get?”

Right now, there is no confirmed change. The two-child benefit cap still limits payments to the first two children in most households. That means families do not receive additional Universal Credit amounts for a third or subsequent child under current rules.

If the two-child benefit cap is lifted, eligible families would receive additional Universal Credit payments for each extra child, increasing their total monthly income.

To understand the impact, here’s what would change if the policy were removed:

Families with more than two children would qualify for extra child elements under Universal Credit

Monthly payments would increase based on the number of additional children

Financial pressure on larger families would reduce significantly

For example, when people search:

“2 child benefit cap lifted how much will I get”

“2 child benefit cap lifted how much will I get universal credit”

They are trying to estimate how much extra support they could receive. While exact figures depend on individual circumstances, each additional child element in Universal Credit is worth thousands of pounds per year. Removing the cap would therefore create a meaningful increase in household income.

However, it’s important to stay grounded in current policy. There is no automatic payment or confirmed rollout yet. Questions like “will the 2 child benefit cap be automatically paid” or “will the 2 child benefit cap be backdated” remain speculative.

For caregivers and support workers, this is where clear communication matters. Many clients may expect immediate financial relief due to ongoing debates or media headlines. You must explain that:

The cap is still in place today

No confirmed payment increase has been announced

Any future change would likely require a formal policy update

Until then, families should plan based on existing Universal Credit rules, not future expectations.

Care Provider Checklist: How to Support Clients Through Benefit Changes

Why legacy benefits are being replaced

Care providers play a critical role during this period of DWP benefit scrapping. You are often the first point of support when clients feel confused, overwhelmed, or at risk of losing income.

Use this checklist to stay proactive and protect your clients:

Identify At-Risk Clients

Review your records and flag anyone receiving ESA or other legacy benefits. Prioritise clients with disabilities, limited digital skills, or no family support.

Communicate Early and Clearly

Explain the changes in simple terms. Tell clients:

ESA is ending

They must apply for Universal Credit

Missing deadlines can stop payments

Avoid assumptions, many clients do not understand official letters.

Support the Application Process

Help clients:

Create Universal Credit accounts

Upload required documents

Complete identity checks

Where possible, sit with them during the application to avoid errors.

Track Deadlines and Follow Up

Set reminders for each client’s migration deadline. Check progress regularly and confirm that applications have been submitted successfully.

Manage Expectations Around Policy Changes

Clients may ask about:

“when will the two child benefit cap be lifted”

“two-child benefit cap removed”

“is child benefit going up”

Be clear: these changes are not confirmed yet. Focus clients on what they must do now, not what might happen later.

Monitor Financial Stability

Watch for early signs of financial stress:

Missed rent

Reduced food spending

Anxiety about bills

Step in early and connect clients with additional support if needed.

Stay Updated on Policy Changes

Welfare rules continue to evolve. Follow updates on:

Universal Credit changes

Potential reforms like the 2 child cap

Budget announcements affecting benefits

By following this checklist, you move from reactive support to proactive care. You protect your clients from sudden income loss, and strengthen your role as a trusted guide during uncertain policy changes.

Conclusion

The current wave of DWP benefit scrapping is already changing how caregivers support clients across the UK. ESA is ending, Universal Credit is replacing it, and the transition requires action, not assumptions.

For care providers, this is more than a policy update. It directly affects your clients’ financial stability, well-being, and trust in your service. Acting early, guiding clearly, and staying informed will prevent avoidable crises.

At the same time, wider reforms, like ongoing debates around the two-child benefit cap, continue to shape expectations. But until confirmed, the priority remains simple: help every affected client complete their transition on time.

Care Sync Experts helps you manage applications, compliance, and updates with confidence.

FAQ

Can DWP check your bank account?

The DWP does not routinely monitor your bank account, but it can request access to financial information if it suspects fraud or needs to verify a claim. In some cases, they may work with banks or use data-sharing powers to confirm income and savings.

Can the DWP just stop my benefits?

Yes, the DWP can stop your benefits if you fail to meet eligibility rules, miss a required action (like moving to Universal Credit), or do not respond to official requests. Payments can also stop if your circumstances change and you do not report it.

What triggers a DWP bank check?

A bank check may be triggered by: Suspected fraud or incorrect claims – Unreported income or savings – Data mismatches between government systems – Random compliance reviews

Keeping your information accurate and up to date reduces the risk of checks.

Will I lose my PIP if I inherit money?

No, inheriting money does not automatically stop Personal Independence Payment (PIP). PIP is not means-tested, so it does not depend on your savings or income. However, if your condition improves or your circumstances change, the DWP may review your claim.

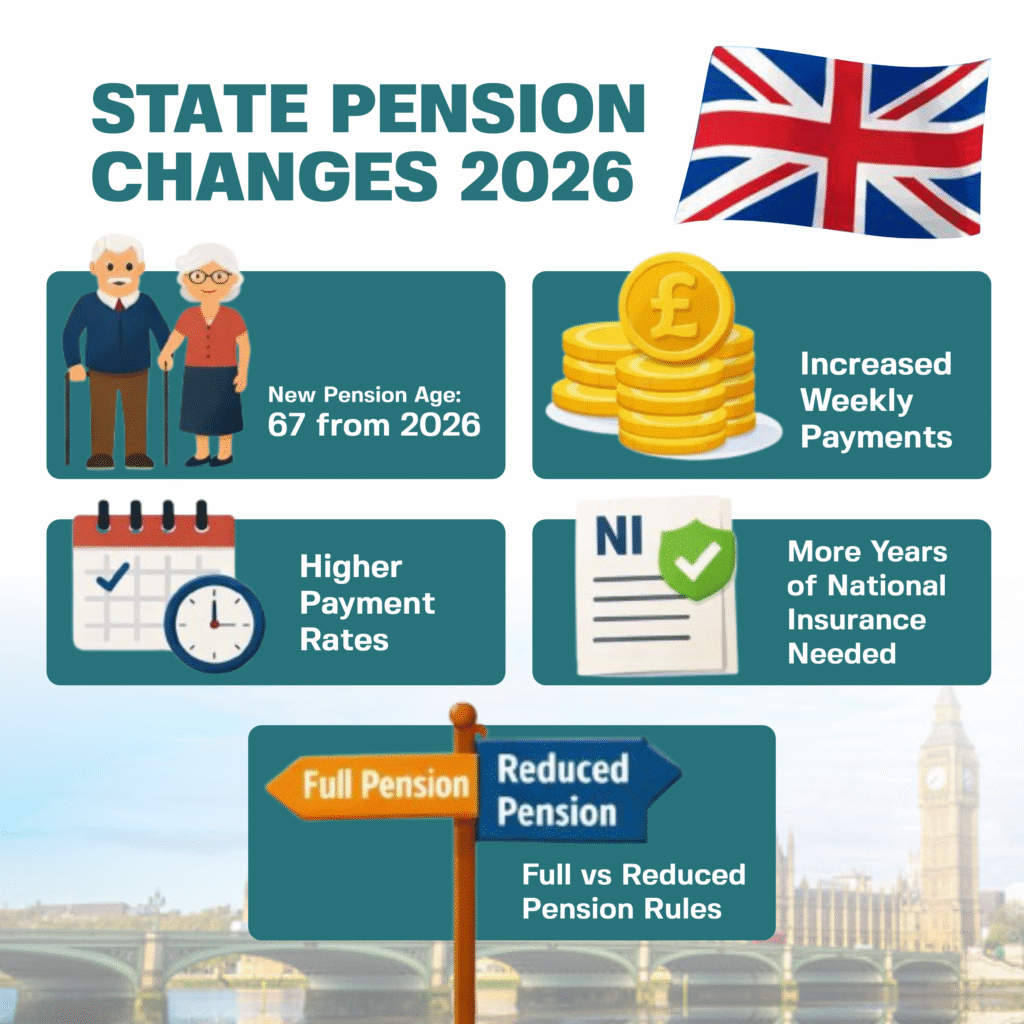

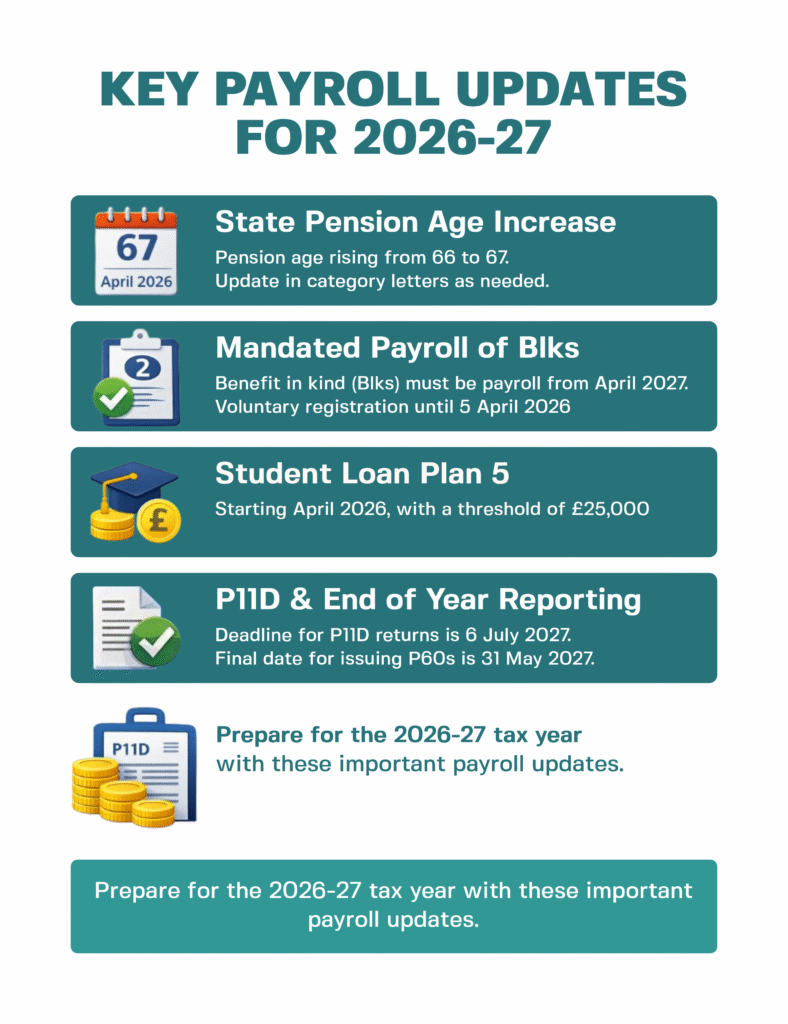

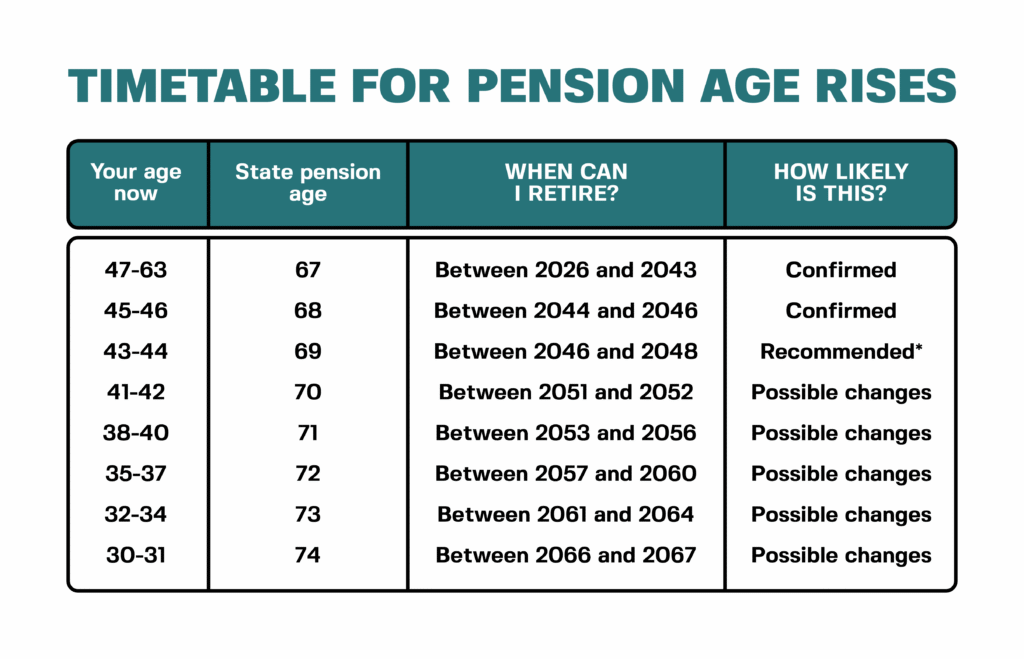

The UK State Pension age increase 2026 will raise the retirement age from 66 to 67 between April 2026 and April 2028. This change affects people born on or after 6 April 1960, meaning they will retire at age 67 instead of 66, depending on their exact birth date. The government introduced this state pension age increase to reflect longer life expectancy and reduce long-term pension costs.

If you’re asking “when can I retire?”, the answer now depends on your date of birth. The increase does not apply all at once, it rolls out gradually over two years, so some people will wait a few extra months, while others will wait the full year.

For care providers and their staff, this means many workers will remain in employment longer, making it essential to understand how the UK state pension age increase 2026 affects retirement planning and workforce decisions.

The state pension age increase 2026 affects anyone born on or after 6 April 1960. If an employee falls into this group, they will not receive their State Pension at 66. Instead, they will need to wait until they reach age 67, depending on their exact birth date.

The increase does not apply equally to everyone. The government is rolling it out in phases between April 2026 and April 2028. For example, someone born in April 1960 may wait only a few extra months, while someone born later in the year could wait much longer.

From a caregiver business perspective, this change directly impacts your workforce:

Many experienced caregivers will stay in employment longer

Retirement timelines will become less predictable

Workforce planning will require closer tracking of staff age and retirement expectations

The DWP state pension age change 2026 also means employers can no longer assume that staff in their mid-60s will retire soon. Instead, care providers should expect a gradual shift, where older employees remain active in the workforce for an extended period.

Understanding who is affected by the UK state pension age increase allows care businesses to plan staffing levels, manage expectations, and avoid sudden workforce gaps.

When Can You Retire Now? (Use the Official Calculator)

State Pension Changes 2026- New Payment Rates and Age Rules

If you’re asking “when can I retire?”, the answer now depends entirely on your date of birth. The state pension age increase 2026 means there is no single retirement age anymore; each person has a specific date.

The easiest way to check is by using the official UK State Pension age calculator on GOV.UK. This tool gives you your exact retirement date based on current legislation.

Quick Answer:

Your State Pension age depends on your date of birth, and you should use the official UK State Pension age calculator to confirm when you can retire.

How to check your pension age:

Go to the GOV.UK pension calculator

Enter your date of birth

View your exact State Pension age and date

You can also check a state pension forecast to see how much you’re likely to receive under the New State Pension 2026 rules.

Caregiver businesses should encourage staff, especially those aged 55+, to use the UK State Pension calculator. This helps:

Set realistic retirement expectations

Prevent sudden staffing gaps

Support better workforce planning

Because of the UK state pension age increase 2026 calculator results, two employees of the same age may now retire at different times. Care providers must account for this variation when planning schedules, hiring, and succession.

How Much Is the State Pension in 2026/27?

The state pension increase 2026/27 raises payments by 4.8%, in line with average earnings under the triple lock policy. This means higher weekly income for pensioners starting from April 2026.

Current Rates:

New State Pension 2026:

£241.30 per week (£12,547.60 per year)

Basic State Pension (pre-2016 retirees):

£184.90 per week (£9,614.80 per year)

The New State Pension in 2026 will pay up to £241.30 per week, depending on your National Insurance record.

To receive the full amount, individuals typically need 35 years of qualifying National Insurance contributions. Those with fewer years will receive a reduced amount.

How much is the state pension for a woman?

The amount is the same for men and women under the current system. What matters is the individual’s National Insurance record, not gender.

Understanding the state pension increase 2026 helps care businesses:

Support staff with retirement planning

Explain income expectations to older employees

Reduce uncertainty around financial readiness

Many caregivers may rely heavily on the New State Pension 2026, especially if they do not have private pensions. Encouraging staff to check their state pension forecast ensures they understand what they will actually receive and whether they need to work longer.

The UK state pension age increase 2026 will directly affect how care providers manage their workforce. As employees delay retirement, your staffing model will shift, both positively and negatively.

Quick Insight:

The state pension age increase means more experienced caregivers will stay in the workforce longer, but it also increases the risk of burnout and workforce imbalance.

1. Longer Staff Retention

Many caregivers who planned to retire at 66 will now continue working until 67.

This can benefit your business:

You retain experienced staff longer

You reduce short-term recruitment pressure

You maintain continuity of care for clients

2. Increased Burnout Risk

Older caregivers may:

Struggle with physically demanding roles

Experience fatigue or reduced mobility

This creates a real operational risk if not managed properly.

3. Workforce Planning Becomes Critical

The UK pension age reform impact means you must actively plan for:

Gradual retirement timelines

Flexible working options

Succession planning

You can no longer assume when staff will leave. Instead, you must track and manage retirement expectations.

4. Recruitment Strategy Must Evolve

With delayed retirement:

Fewer roles may open up immediately

Younger workers may face slower entry into the sector

Care providers should balance:

Retaining experienced staff

Bringing in new talent

What smart care providers are doing

Forward-thinking providers are already:

Offering flexible shifts for older staff

Reducing physically demanding tasks

Encouraging staff to check their state pension forecast

Staying updated with pension news and DWP changes

The state pension age increase is not just a policy change, it is a workforce shift. Care providers who adapt early will maintain stability, reduce risk, and stay competitive.

Should Care Providers Adjust Workforce Planning Now?

UK Payroll Updates- 2026_27 Changes and Compliance

Yes, care providers should start adjusting workforce planning now. The state pension age increase 2026 will delay retirement for many employees, which changes how you manage staffing, scheduling, and long-term growth.

Care providers should adjust workforce planning now if they rely on older staff, because the state pension age increase will delay retirement and change workforce availability.

When you SHOULD adjust now

You should act immediately if:

A large portion of your workforce is aged 55+

You rely heavily on experienced caregivers

You expect staff to retire soon based on old assumptions

In these cases, the state pension age increase will directly affect your staffing timeline.

When adjustment is less urgent

You may not need immediate changes if:

Your workforce is mostly younger (under 50)

You already have strong recruitment pipelines

You use flexible or agency staffing models

Practical steps care providers should take

To adapt effectively:

Review staff age profiles and expected retire at age timelines

Encourage employees to check when can I retire using official tools

Offer flexible roles for older staff

Introduce succession planning early

Train younger staff to prepare for future leadership roles

The risk of doing nothing

If you ignore the state pension age increase 2026, you may face:

Unexpected staff shortages

Burnout among older employees

Poor workforce planning decisions

The state pension age increase is already underway. Care providers who respond early will maintain stability, support their staff better, and avoid operational disruptions.

Future Pension Changes You Should Watch (2025–2046)

The state pension age increase 2026 is only one part of a wider shift in UK pension policy. Care providers should stay informed about upcoming changes, because these updates will continue to affect workforce planning and staff expectations.

Quick Insight:

The UK government plans to increase the State Pension age to 68 in the future, and ongoing policy reviews could bring further changes.

1. Planned Increase to Age 68

The government has already scheduled another state pension age increase:

Age 68 is expected between 2044 and 2046

Future reviews may bring this forward depending on life expectancy and economic conditions

This means younger caregivers may need to work even longer before they retire at age.

2. Ongoing Reviews and DWP Updates

The Department for Work and Pensions (DWP) regularly reviews pension policy. Recent pension news highlights:

Potential adjustments based on life expectancy trends

Discussions around affordability and sustainability

Occasional DWP state pension warnings about planning ahead

Care providers should monitor these updates to avoid being caught off guard.

3. Other Pension Changes to Watch

Several related updates may also impact your staff:

UK pensioner cash withdrawal changes 2025 – potential changes in how pension funds are accessed

UK state pension reduction 2025 – concerns around reduced real value due to inflation or policy shifts

September 2025 state pension updates – periodic policy announcements affecting benefits

These changes may influence how employees view retirement and financial security.

Understanding future pension trends helps you:

Prepare for long-term workforce changes

Support staff with realistic retirement expectations

Stay aligned with UK pension age reform impact

The UK state pension age increase will continue evolving. Care providers who stay informed and adapt early will remain stable, competitive, and better prepared for future workforce challenges.

Common Questions About the UK State Pension Age Increase 2026

uk state pension age increase 2026

When will the State Pension age reach 67?

The state pension age increase 2026 will raise the retirement age from 66 to 67 between April 2026 and April 2028. The change happens gradually, so not everyone reaches 67 at the same time.

Can I still retire at 66?

Yes, you can still retire at 66, but you may not receive your State Pension yet. If you fall under the UK state pension age increase, you will need to wait until your official pension age before receiving payments.

How do I check when I can retire?

You should use the official UK State Pension age calculator.

Your exact retirement age depends on your date of birth, and the calculator provides the most accurate answer.

You can also check your state pension forecast to understand how much you’ll receive.

Will the State Pension age increase again?

Yes. The government has already planned another state pension age increase to 68 between 2044 and 2046, although future reviews may change this timeline.

What happens if I don’t have enough National Insurance contributions?

You may receive less than the full New State Pension 2026 amount. To qualify for the full payment, you typically need 35 years of contributions. If you have gaps, you may still qualify for a partial pension.

Does the State Pension amount differ for men and women?

No. The amount is the same for both. The key factor is your National Insurance record, not gender.

If you’re wondering how much is the state pension for a woman, the answer is the same as for men under the current system.

These questions reflect the most common concerns around the UK state pension age increase 2026. Clear answers help both individuals and care providers plan more effectively.

Conclusion

The UK state pension age increase 2026 is more than a policy update—it’s a workforce shift that care providers must manage proactively.

What you should do now:

Expect staff to retire at age 67, not 66

Encourage employees to check when can I retire using the UK State Pension age calculator

Support staff in reviewing their state pension forecast

Adjust workforce planning to reflect delayed retirement

Introduce flexible roles to reduce burnout among older caregivers

Stay updated with pension news and DWP state pension age change 2026 developments

Care providers who understand the state pension age increase early will manage staffing better, retain experienced workers, and avoid sudden workforce gaps.

The state pension age increase 2026 is already shaping the future of the care sector. By acting now, you can protect your workforce, support your staff, and keep your operations stable in a changing environment.

Need Support Managing Workforce Changes from the State Pension Age Increase?

The UK state pension age increase 2026 can disrupt staffing plans, delay retirements, and increase pressure on your existing team if not managed early.

Care Sync Experts helps you:

Plan for delayed retirement and workforce shifts

Retain experienced caregivers without increasing burnout

Build flexible staffing models that support older employees

Improve workforce stability and reduce sudden staff shortages

Stay aligned with regulatory expectations and long-term care demands

Get practical, expert guidance to adapt your care service, support your staff, and stay ahead of pension-related workforce changes.

FAQ

Do I get my husband’s State Pension if he dies?

You may be able to receive part of your husband’s State Pension, depending on your circumstances. This is usually called inheriting State Pension or qualifying for bereavement benefits. – If you reached State Pension age before April 2016, you may inherit some of your partner’s pension based on their National Insurance record. – If you’re under the new State Pension system (after April 2016), inheritance is more limited, but you may still qualify for Bereavement Support Payment (BSP).

The exact amount depends on contributions, age, and marital status.

How long is pension paid after death in the UK?

State Pension payments stop shortly after death. However: – Payments may continue briefly if they were already issued before the death was reported – Any overpayments must usually be returned – A surviving spouse or partner may qualify for bereavement benefits instead

You should report a death to the DWP immediately to avoid complications.

Can I pass my pension to my children?

You cannot pass your State Pension directly to your children. The State Pension is not treated as a transferable asset. However: – Private or workplace pensions can often be passed on, depending on the scheme – Beneficiaries may receive lump sums or ongoing payments

Always check the specific rules of your pension provider.

What is the minimum salary to qualify for State Pension in the UK?

There is no fixed minimum salary to qualify for the State Pension. Instead, eligibility depends on National Insurance (NI) contributions. – You typically need at least 10 qualifying years to receive any pension – You need 35 years to receive the full New State Pension 2026

You earn qualifying years by: – Working and paying NI contributions – Receiving NI credits (e.g., for caregiving, unemployment, or illness)

Even low earners can qualify, as long as they meet the contribution requirements.

TL;DR: What the Employment Rights Bill Means for Workers

The Employment Rights Bill (often searched as the employee rights bill or Employment Rights Bill 2024) introduces phased employment law changes 2025–2027 that directly affect care providers across England, Wales, Scotland, and Northern Ireland. If you employ a care assistant, support worker, or healthcare assistant, you must prepare now.

Here is what you should know:

From 2026–2027: Workers gain stronger rights around predictable hours, sick pay, family leave, and protection from unfair dismissal.

From October 2026: Employers must take “all reasonable steps” to prevent harassment, including harassment by service users and family members.

Tribunal risk increases: Employees will have longer to bring claims, and tribunals can uplift compensation if you fail to meet prevention duties.

Costs will rise: Scheduling reforms, sick pay changes, and sector-wide pay negotiations will affect margins, especially in domiciliary care and 24 hour home care models.

Action required now: Audit contracts, update policies, model staffing costs, strengthen record-keeping, and train managers before deadlines hit.

This guide breaks down what the Employment Rights Bill changes, how it affects care assistant duties, rota management, and dismissal risk, and what care providers must implement before 2026–2027.

Key Dates:

The Employment Rights Bill moves in phases. Care providers must track each stage carefully and avoid assuming everything changes at once.

Here are the dates that matter:

26 October 2024 – Employers must take reasonable steps to prevent sexual harassment. This duty already applies.

18 December 2025 – The Employment Rights Act 2025 received Royal Assent, formally introducing wide-ranging employment law changes 2025.

April 2026 (expected implementation phase) – Whistleblowing protections expand, and early elements of reform begin to take effect.

October 2026 – Employers must take “all reasonable steps” to prevent harassment, including third-party harassment. Tribunal time limits extend from three to six months.

2026–2027 (phased roll-out) – Predictable-hours rights, zero-hours reform, and strengthened unfair dismissal protections come into force.

2027 – Workers on low-hours or variable contracts gain rights to guaranteed hours reflecting actual work patterns, along with compensation for cancelled shifts.

These new rules in UK employment law do not arrive overnight, but they build quickly. If you operate domiciliary care, supported living, or 24 hour live in care services, you should treat 2026 as your practical compliance deadline.

The Employment Rights Bill affects every employer, but care providers will feel the pressure faster and harder than most sectors.

You operate on narrow margins. You manage complex rotas. You employ large numbers of care assistants, support workers, healthcare assistants, and mental health support workers across multiple settings. When employment law changes 2025 tighten worker protections, your operational model absorbs the shock immediately.

Unlike office-based industries, care services rely on:

Variable-hours contracts for domiciliary care

Night shifts and lone working

24 hour home care and 24 hour live in care packages

Agency and bank staff

High turnover in assistant caregiver roles

If predictable-hours rights expand in 2027, rota flexibility reduces. If sick pay becomes payable from day one, absence costs increase. If unfair dismissal protection shortens qualifying periods, probation management becomes riskier. If tribunal time limits double, your exposure window expands.

Care settings also face higher third-party interaction risk. A care assistant delivering personal care in someone’s home cannot control every environment. A support worker in supported living interacts with visitors, family members, and external professionals daily. These realities make harassment prevention and dismissal decisions more complex under the employee rights bill reforms.

In short, employment law rarely hits care providers in theory. It hits you in scheduling, payroll, recruitment, safeguarding, and contracts, all at once.

What the Employment Rights Bill Actually Changes

Many providers hear “Employment Rights Bill” and assume it is just another update to employment law. It is not. This legislation restructures core employer obligations across pay, scheduling, dismissal, and harassment.

The Employment Rights Bill 2024, now enacted as the Employment Rights Act 2025, introduces phased reforms between 2026 and 2027. These reforms aim to strengthen worker protections, increase job security, and shift more responsibility onto employers.

Here is what that means in practical terms:

Workers on irregular or low-hours contracts gain stronger rights to predictable income.

Employers must tighten dismissal processes as qualifying periods shorten.

Sick pay and family leave protections expand.

Harassment prevention duties move from “reasonable steps” to “all reasonable steps.”

Tribunal time limits extend, increasing litigation exposure.

These are not cosmetic updates. They reshape how you structure contracts, manage rotas, document decisions, and train managers.

If you run a service employing care assistants, support workers, or healthcare assistants, you must now treat workforce compliance as a strategic function, not just an HR task.

The remainder of this guide breaks down each reform in detail and shows how it affects domiciliary care, care homes, supported living services, and assistant caregiver job structures.

Staffing & Scheduling: Zero-Hours Reform and Predictable Hours

The Employment Rights Bill targets variable and zero-hours working patterns, a model many care providers rely on to deliver flexible support.

From 2026–2027 (phased implementation), workers on low or unpredictable hours will gain stronger rights to:

Guaranteed hours that reflect their actual working pattern

Advance notice of shifts

Compensation for cancelled or curtailed shifts

If you run domiciliary care or 24 hour home care services, this affects how you build rotas for every care assistant, support worker, and mental health support worker on your books.

Care providers often:

Increase hours during winter pressures

Cancel visits when packages change

Use bank staff to fill last-minute gap

Adjust shifts when service users enter hospital

Under the employment law changes 2025, these routine adjustments may trigger financial consequences.

If a care assistant regularly works 35 hours despite holding a 10-hour contract, you may need to offer a contract that reflects reality. If you cancel shifts at short notice due to package withdrawal, you may need to compensate the worker.

This reform directly impacts:

Domiciliary care agencies

Supported living providers

24 hour live in care models

Services relying heavily on assistant caregiver job flexibility

What You Should Do Now

Do not wait for 2027 implementation. Start building evidence and systems now:

Audit actual hours worked versus contracted hours

Track cancelled or shortened shifts

Review probationary contract templates

Model cost exposure under guaranteed-hours scenarios

Speak to commissioners about pricing assumptions

If you fail to align contracts with real working patterns, you increase exposure to tribunal claims and compliance challenges under the employee rights bill reforms.

The providers who adapt early will protect margins. The providers who ignore rota data will struggle to defend their decisions later.

Pay, Terms and the Adult Social Care Negotiating Body

Fair Pay Negotiating Body for adult social care

The Employment Rights Bill does not only change contracts and scheduling. It also reshapes how pay develops across the care sector.

The government plans to introduce an Adult Social Care Negotiating Body to agree sector-wide pay rates and employment standards. This move aims to improve retention, reduce turnover, and stabilise the workforce. In theory, it strengthens career pathways for every care assistant, support worker, and healthcare assistant.

In practice, it increases cost pressure on providers.

What This Means for Care Providers

If national minimum pay bands rise through negotiated agreements, you will need to:

Review your care assistant job specification and pay structure

Recalculate margins on council contracts

Adjust recruitment budgets for support worker jobs

Update assistant caregiver job descriptions to reflect new standards

Higher baseline pay may improve recruitment in care assistant jobs and mental health support worker roles. However, unless commissioners increase contract rates, your wage bill rises without matching income.

This creates a direct tension between:

Workforce stability

Contract viability

Service sustainability

What You Should Do Now

Do not wait for formal pay bands to appear before preparing.

Start by:

Modelling wage increases of 5–15% across frontline role

Reviewing contracts with local authorities for uplift clauses

Identifying services operating on the tightest margins

Building a clear evidence pack showing cost increases

Commissioners increasingly expect providers to justify pricing with workforce data. If you prepare now, you position yourself as credible and proactive when negotiating rates.

The Employment Rights Bill strengthens worker protections. Care providers must strengthen financial planning at the same time.

Sick Pay, Leave, and Day-One Rights: What Changes for Care Employers

The Employment Rights Bill strengthens statutory protections around sick pay and family leave. For care providers, these reforms affect daily operations more than policy wording.

From 2026 onwards (phased implementation), reforms are expected to:

Remove waiting periods for Statutory Sick Pay (SSP), making sick pay payable from the first eligible day

Expand eligibility for lower-income workers

Strengthen “day-one” rights for certain family-related leave

Shorten qualifying periods for protection against unfair dismissal

For employers of care assistants, support workers, and healthcare assistants, this means absence management must tighten.

Care services face:

High exposure to illness (especially in 24 hour home care and residential care)

Frequent short-term absence

Infection control obligations

Reliance on bank or agency cover

If sick pay becomes payable earlier and unfair dismissal protections attach sooner, you cannot treat early absence during probation as a low-risk decision.

Managers must understand the difference between:

Unfair dismissal (statutory rights and fairness test)

Wrongful dismissal (breach of contract, such as failing to give notice)

Under strengthened employment law protections, probation management errors may lead to claims faster than before.

What You Should Do Now

Prepare your service before changes take full effect:

Update absence and sick pay policies

Train managers on lawful probation reviews

Document performance concerns clearly and early

Review your assistant caregiver job description and expectations for attendance

Ensure payroll systems can adapt quickly

If you employ frontline roles such as care assistant or mental health support worker, you must assume that dismissal decisions made within the first year of employment will face closer scrutiny under the employment law changes 2025.

Strong documentation protects you. Informal conversations do not.

The Employment Rights Bill strengthens worker security. Your processes must match that strength.

Dismissals, Tribunal Risk and Wrongful Dismissal Exposure

The Employment Rights Bill increases legal risk when you dismiss staff. Care providers must now treat every dismissal as potentially reviewable by a tribunal within a longer window.

From October 2026, the time limit for most employment tribunal claims increases from three months to six months. This change alone doubles your exposure period.

At the same time, qualifying periods for certain protections shorten, meaning employees may access unfair dismissal rights earlier in their employment.

Unfair vs Wrongful Dismissal: Know the Difference

Care managers often confuse two separate legal concepts:

Unfair dismissal: You failed to follow a fair process or lacked a fair reason under employment law.

Wrongful dismissal: You breached the employee’s contract, often by failing to give proper notice or pay.

Both risks increase under the employment law changes 2025.

If you dismiss a care assistant during probation without evidence of performance concerns, you risk an unfair dismissal claim sooner than before.

If you dismiss a support worker immediately without contractual notice, you risk wrongful dismissal even if your reason was valid.

Why Care Providers Face Higher Risk

Care environments create complex dismissal situations:

Performance concerns linked to care assistant duties

Conduct issues involving service users

Lone-working safety breaches

Under the employee rights bill reforms, you must show:

A clear reason for dismissal

A documented investigation

Evidence you considered alternatives

A fair hearing process

If you cannot produce records six months later, your defence weakens significantly.

What You Should Do Now

Before terminating any employee, ensure you:

Confirm the contractual notice requirement

Follow a documented disciplinary or capability process

Keep detailed investigation notes

Separate safeguarding action from employment decision-making

Provide written outcome letters

Train managers to avoid informal dismissals. Phrases like “it’s just not working out” no longer provide safe ground.

The Employment Rights Bill does not remove your ability to dismiss staff. It removes your ability to do it casually.

Care providers who strengthen process now will avoid costly tribunal claims later.

Harassment, Third-Party Risk and the “All Reasonable Steps” Duty

How to Prevent Workplace Harassment

The Employment Rights Bill significantly strengthens employer responsibility for preventing workplace harassment. Care providers face particular exposure because your staff work in environments you do not fully control.

From October 2026, employers must take “all reasonable steps” to prevent harassment. This replaces the current “reasonable steps” standard and raises the bar.

At the same time, employers will become directly liable for harassment of staff by third parties, including:

Service user

Family members

Visitors

Contractors

External professionals

For care providers, this risk is real and immediate.

Why This Reform Hits Care Harder

A care assistant delivering 24 hour live in care works alone in a private home.

A support worker in supported living interacts daily with residents’ visitors.

A mental health support worker may manage behaviours linked to trauma or cognitive conditions.

These environments increase the likelihood of inappropriate conduct. Under the strengthened duty, you must prove you did everything reasonably possible to prevent it.

Tribunals will examine:

Your policy

Your training

Your reporting routes

Your risk assessments

Your actions after incidents

If any of these elements are missing, you weaken your defence.

What “All Reasonable Steps” Looks Like in Care

In practical terms, you should already be able to demonstrate:

A clear anti-harassment policy that includes third-party behaviour

Care-plan risk flags where previous incidents occurred

Two-carer arrangements for high-risk visits

A safe withdrawal protocol for staff

Multiple reporting routes that do not rely solely on line managers

Manager training on trauma-informed responses

If a service user behaves inappropriately toward a healthcare assistant, your records must show:

The incident was documented

The care plan was reviewed

Risk controls were updated

You communicated boundaries where appropriate

You protected the employee from further exposure

With tribunal time limits extending to six months, you must preserve:

Training attendance logs

Risk assessment updates

Incident reports

Investigation outcomes

Manager decisions and rationale

If you cannot evidence these steps, you may struggle to rely on the “all reasonable steps” defence.

The Employment Rights Bill does not expect perfection. It expects preparation.

Care providers who treat harassment prevention as a live operational risk, not just a policy requirement, will position themselves far more safely under the employment law changes 2025.

Payroll & Compliance Watch: HMRC Rule Changes (22 October 2025)

While the Employment Rights Bill focuses on worker protections, care providers must also monitor parallel compliance deadlines that affect payroll and reporting.

One important date to note is 22 October 2025. If your organisation operates a PAYE Settlement Agreement (PSA), HMRC requires electronic payment clearance by this date to avoid interest or penalties.

This is not a reform introduced by the employee rights bill itself. However, it sits within the same broader landscape of tightening compliance expectations for employers.

Care organisations often manage:

Large frontline workforces

Overtime and variable-hour payments

Mileage reimbursements for domiciliary care

Uniform allowances

Staff benefit schemes

If payroll processes slip, especially during periods of legislative change, HMRC penalties can add financial strain to an already pressured operating model.

What You Should Do Now

Confirm whether your organisation operates a PSA

Review payroll reporting processes

Ensure finance and HR teams align on compliance deadlines

Document internal responsibility for statutory submission

Employment law changes 2025 will already require policy updates and training investment. Avoid compounding risk with preventable payroll non-compliance.

Care providers must treat workforce reform and financial compliance as part of the same governance framework.

What Care Providers Should Do Next: A Practical Implementation Plan

Employment Rights Bill- Key Components of an Implementation Plan

The Employment Rights Bill introduces phased reforms, but preparation must begin now. Waiting until 2026 or 2027 will leave you reacting under pressure instead of leading with control.

Here is a structured plan to protect your organisation.

Phase 1: Immediate Review (Next 30 Days)

Focus on visibility and risk mapping.

Audit all employment contracts for care assistants, support workers, and frontline staff

Compare contracted hours against actual worked hours

Review dismissal procedures and probation policies

Update harassment policies to reference third-party situations

Identify your highest-risk services (e.g., 24 hour home care, lone working)

This phase creates clarity. You cannot fix what you have not measured.

Phase 2: Systems and Training (Next 90 Days)

Strengthen operational foundations.

Train managers on unfair vs wrongful dismissal

Introduce structured investigation templates

Update absence and sick pay policies

Build rota tracking systems to monitor cancellations and pattern hours

Create a harassment reporting flowchart for all staff

If you employ staff in assistant caregiver jobs, ensure managers understand how changes affect scheduling, probation handling, and disciplinary action.

Phase 3: Financial and Strategic Planning (Next 6–12 Months)

Prepare for cost and tribunal exposure.

Model wage uplift scenarios under sector-wide pay negotiations

Review council contracts for uplift mechanisms

Create a compliance evidence folder (training logs, policies, risk assessments)

Assign a named lead responsible for Employment Rights Act readiness

Care providers that treat these reforms as strategic governance will protect both margins and reputation.

The employment law changes 2025 will not reverse. Regulators, commissioners, and tribunals will expect preparation not surprise.

Conclusion

The Employment Rights Bill reshapes how care providers manage people, risk, and compliance. It strengthens worker protections, expands tribunal exposure, and raises the standard for prevention in areas such as harassment and dismissal.

For providers employing care assistants, support workers, and healthcare assistants, these employment law changes 2025 do not sit in isolation. They affect:

Rota flexibility

Contract structure

Absence management

Dismissal procedures

Payroll controls

Harassment prevention

Financial planning

The organisations that treat this as an HR update will struggle.

The organisations that treat it as a board-level governance issue will adapt.

You must:

Align contracts with real working patterns

Strengthen documentation around performance and dismissal

Build robust third-party harassment controls

Model workforce cost exposure

Preserve training and risk assessment evidence

The employee rights bill does not remove your ability to run a care business. It removes tolerance for weak systems.

Care providers who act early will protect margins, maintain commissioner confidence, and reduce tribunal risk. Those who delay will face pressure from every direction: financial, legal, and reputational.

The question is not whether these new rules in UK employment law will affect your service.

The question is whether your governance framework is strong enough to absorb them.

Ready to Strengthen Your Employment Law Compliance Before 2026?

The Employment Rights Bill is not just another policy update. It changes how you manage rotas, dismiss staff, prevent harassment, document decisions, and defend tribunal claims.

For care providers, weak systems will not survive these reforms. Strong governance will.

Care Sync Experts supports domiciliary care agencies, supported living providers, and care homes across the UK with:

Full employment contract audits aligned with the Employment Rights Act 2025

Zero-hours and predictable-hours compliance modelling

Dismissal process reviews to reduce unfair and wrongful dismissal risk

Care-specific harassment prevention frameworks and third-party risk controls

Manager training on probation, absence management, and investigation standards

Workforce cost modelling ahead of sector-wide pay negotiations

Tribunal-readiness evidence pack design and documentation systems

Whether you operate 24 hour home care, supported living services, or large residential settings, we help you build employment systems that protect your margins, strengthen governance, and withstand legal scrutiny.

What are the 5 fair reasons for dismissal under the Employment Rights Act?

UK employment law recognises five potentially fair reasons for dismissal:

– Capability or qualifications (performance, skill, or health issues) – Conduct (misconduct or gross misconduct) Redundancy – Statutory restriction (e.g., loss of required licence or visa status) – Some other substantial reason (SOSR)

Even if you rely on one of these reasons, you must still follow a fair process. If you skip investigation, ignore evidence, or fail to hold a proper hearing, a tribunal may still find the dismissal unfair.

Do I need a new contract if my role changes?

It depends on the scale of the change. Minor adjustments to duties, for example, adjusting certain care assistant duties within the scope of an existing job, usually do not require a brand-new contract.

However, you should issue written confirmation if: – Hours change significantly – Pay changes – Reporting lines change – Core responsibilities expand beyond the original care assistant job specification – The role moves into a substantially different function

If you introduce predictable-hours adjustments or guaranteed-hour offers under the Employment Rights Bill reforms, you should document those changes formally. Always consult the variation clause in the original contract before making changes.

Can an employer make changes to your job duties?

An employer can make reasonable changes if:

– The contract allows flexibility – The changes remain within the scope of the role – The changes are not discriminatory – The employer consults properly where changes are substantial

For example, asking a support worker to assist with additional community activities may fall within scope. Asking them to perform a completely different professional function without agreement may not.

If changes significantly alter responsibilities, pay, or status, the employer should consult and agree the variation. Imposing major changes without agreement can lead to claims for constructive dismissal or breach of contract.

Can I be fired for refusing to do something not in my job description?

It depends on what you refused and how your contract is written.

If the instruction falls reasonably within your role, even if not explicitly listed in the assistant caregiver job description, refusal may amount to misconduct.

However, you may have legal protection if: – The instruction is unsafe – The instruction is unlawful – The instruction breaches regulatory standards – The instruction significantly exceeds your agreed role

For care providers, this often arises in safeguarding contexts. If a healthcare assistant refuses to perform a task because they believe it breaches care standards, you must investigate carefully before taking disciplinary action.

Always assess whether the instruction was reasonable and whether refusal connects to health, safety, or legal compliance.

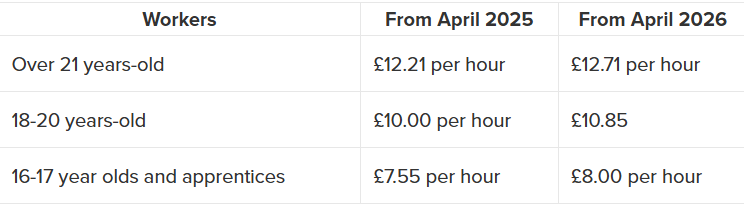

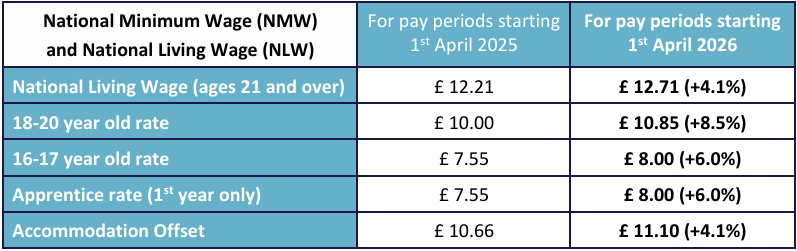

From 1 April 2026, the National Minimum Wage and National Living Wage 2026 rates increase across England, Scotland, Wales, and Northern Ireland. Workers aged 21 and over must receive £12.71 per hour. Younger age bands and apprentice rates also rise.

At the same time, the new Fair Work Agency begins operations in April 2026, replacing HMRC’s standalone minimum wage enforcement with a single body that can investigate minimum wage, holiday pay, and statutory sick pay together.

For domiciliary care agencies, supported living providers, and care homes, the risk does not sit in the headline rate. It sits in travel time, deductions, sleep-ins, salaried hours, and record-keeping. If your effective hourly rate falls below the legal threshold in any pay reference period, you face arrears, penalties of up to 200%, and public naming.

Confirmed National Minimum Wage and National Living Wage rates from 1 April 2026

The Government accepted the Low Pay Commission’s recommendations in full. The new National Minimum Wage rates apply from 1 April 2026 across England, Scotland, Wales, and Northern Ireland.

Here are the confirmed rates:

Category

Rate from 1 April 2026

National Living Wage (aged 21 and over)

£12.71 per hour

18–20 year olds

£10.85 per hour

16–17 year olds

£8.00 per hour

Apprentice rate

£8.00 per hour

Accommodation offset

£11.10 per day

What this means in monthly terms

For employers calculating Minimum wage UK 2026 per month, use hours worked, not assumptions.

Example:

37.5 hours per week at £12.71

Weekly pay: £476.63

Monthly pay (average): approx. £2,065 before tax

Actual take home pay depends on tax code, pension deductions, and any salary sacrifice arrangements. Minimum wage compliance looks at gross pay before tax, not net pay received.

Scotland, London, and regional confusion

Some employers search for “minimum wage Scotland” or “minimum wage 2026 UK London.” The statutory National Minimum Wage is the same across the whole UK. Scotland and London do not set separate legal minimum wage rates.

However, the voluntary London Living Wage (set by the Living Wage Foundation) is higher than the statutory minimum. Paying it does not remove your obligation to comply with statutory minimum wage rules.

Now let’s look at what these increases actually cost care providers in real terms.

What the National Minimum Wage increase really costs a care business

The National Minimum Wage 2026 rise looks modest on paper. In practice, it reshapes your entire cost base.

Start with the headline figure:

£12.71 per hour for workers aged 21+

37.5 hours per week

Annual gross pay increases by roughly £975 per worker

That number alone does not break a business. The compounding effect might.

1. On-costs rise automatically

When base pay rises, everything calculated as a percentage rises with it:

Employer National Insurance

Workplace pension contributions

Holiday pay accrual

Statutory sick pay exposure

Overtime rates linked to basic pay

From April 2025, Employer NI increased to 15% with a reduced threshold. That change already tightened margins. April 2026 layers another wage uplift on top.

2. Travel time multiplies the impact (domiciliary care)

In homecare, you do not pay only for contact time. Travel time between visits counts as working time for National Minimum Wage purposes.

If travel time represents 15–25% of working hours, the wage increase applies to that portion too.

If you currently pay:

£12.71 for contact time

But fail to fully include travel time in payroll

Your effective hourly rate may already sit below minimum wage 2026 once you divide total pay by total working time.

3. Care sector margins remain thin

Independent care providers operate in a fee environment that rarely matches actual employment costs. Employment costs typically represent 70–80% of total provider expenditure.

When statutory rates rise, but commissioner fees stay static, providers absorb the difference.

That tension explains why compliance failures often arise from payroll structure errors, not deliberate underpayment. However, regulators do not treat financial pressure as a defence.

The math is simple:

Higher base rate

Higher on-cost percentage

Travel time inclusion

Variable hours = Narrower margin for error

Now add enforcement.

Let’s look at how the Fair Work Agency changes the compliance landscape from April 2026.

Fair Work Agency payroll checks: what changes from April 2026

From 7 April 2026, the Fair Work Agency (FWA) begins operations as the UK’s single labour market enforcement body. It replaces HMRC’s standalone National Minimum Wage enforcement function and brings several enforcement streams under one structure.

This is not a cosmetic change. It shifts how investigations start, how far they reach, and what they examine.

What the Fair Work Agency consolidates

The FWA combines:

HMRC’s National Minimum Wage enforcement

The Employment Agency Standards Inspectorate

The Gangmasters and Labour Abuse Authority

It also gains authority to enforce additional employment rights, including holiday pay and statutory sick pay, rather than waiting for workers to bring tribunal claims.

For care providers, that means one investigation can now cover:

National Minimum Wage

Holiday pay calculations

Sick pay compliance

Record-keeping standards

Agency worker compliance (where relevant)

Expect more payroll checks, not fewer

Some providers search for phrases like “HMRC wage raid payroll checks.” The reality is less dramatic but more structured.

The FWA can:

Enter premises to inspect records

Require payroll, time sheets, and contracts

Issue Notices of Underpayment

Impose penalties of up to 200% of arrears (capped at £20,000 per worker)

Publicly name employers

If you pay arrears quickly, the penalty can reduce to 100%, but that still doubles the financial exposure.

Employers rely on zero-hours or flexible contracts

Domiciliary care, supported living, and care homes match that profile precisely.

Record-keeping now matters more than ever

The Employment Rights reforms introduce stronger record-keeping expectations, particularly around holiday entitlement and pay. Investigators will expect six years of accessible, accurate records.

If you cannot demonstrate compliance, you assume non-compliance.

In short, April 2026 brings higher pay rates and broader enforcement at the same time. Care providers must prepare for structured, evidence-based payroll scrutiny, not just headline wage checks.

Now, let’s look at the six compliance traps that most often trigger underpayment findings in care.

Why care providers underpay minimum wage without meaning to

National Minimum Wage 2026 for Care Providers

Most care providers do not deliberately breach the National Minimum Wage. They fall into calculation traps.

Investigators do not ask, “What hourly rate does the contract say?” They ask, “What was the worker’s effective hourly rate across the pay reference period?”

If total pay that counts ÷ total working time that counts falls below minimum wage 2026, you face arrears.

Here are the six traps that trigger enforcement in domiciliary care, supported living, and care homes.

1) Travel time between visits (domiciliary care risk)

In homecare, travel between appointments counts as working time for National Minimum Wage purposes.

If you:

Pay £12.71 for contact time

Fail to pay fully for travel time

Or underestimate travel time systematically

You reduce the worker’s effective hourly rate.

Example:

6 contact hours paid at £12.71

1.5 hours travel unpaid

Worker actually worked 7.5 hours

You divide total pay by 7.5 hours, not 6.

That difference alone can push pay below UK minimum wage increase 2026 thresholds.

If you use estimated travel time, document your method and test it against real routes regularly.

2) Deductions that reduce minimum wage pay

HMRC and the Fair Work Agency assess what the worker actually receives.

Certain deductions reduce minimum wage pay, including:

Required uniforms (even “black trousers and shoes”)

If post-deduction pay drops below the National Minimum Wage, you breach the law, even if the headline rate looks safe.

Many providers paying above minimum wage 2026 UK London levels still fail compliance because deductions erase the buffer.

3) Sleep-ins versus on-call (supported living risk)

The Supreme Court clarified that genuine sleep-in hours do not require minimum wage if the worker can sleep and only respond if needed.

However:

Time spent awake and working must be paid at minimum wage.

Records must show when the worker woke and worked.

If staff remain on-call and must stay awake or remain ready to work continuously, you must pay minimum wage for the full period.

Poor documentation, not intent, often creates arrears.

4) Unpaid training, induction, and meetings

Mandatory training counts as working time.

That includes:

Induction before first shift

E-learning modules

Safeguarding updates

Team meetings

If you require attendance, you must pay for it.

Providers frequently breach National Minimum Wage 2026 rules by assuming training outside rostered hours does not count. It does.

5) Salaried hours misclassification

A salary does not protect you from minimum wage checks.

For a worker to qualify as a salaried hours worker under minimum wage rules:

They must receive an annual salary

For a fixed number of basic hours

Paid in equal instalments

If those conditions fail, the worker becomes “unmeasured work” for minimum wage purposes.

If they regularly work beyond basic hours without paid overtime or timely time off in lieu, their effective hourly rate can fall below minimum wage UK 2026 per month equivalents once recalculated.

Investigators now review salaried care managers more closely than before.

6) Apprentice rate errors

The apprentice rate of £8.00 only applies to:

Apprentices under 19

Apprentices 19+ in their first year

Once an apprentice turns 19 and completes year one, they move to their age band rate.

Payroll systems often fail to update automatically.

That error creates technical underpayment under National Minimum Wage rules.

What changed in 2024 and 2025, and what next in 2026?

To understand National Minimum Wage 2026, you need to see the pattern.

Minimum wage 2024