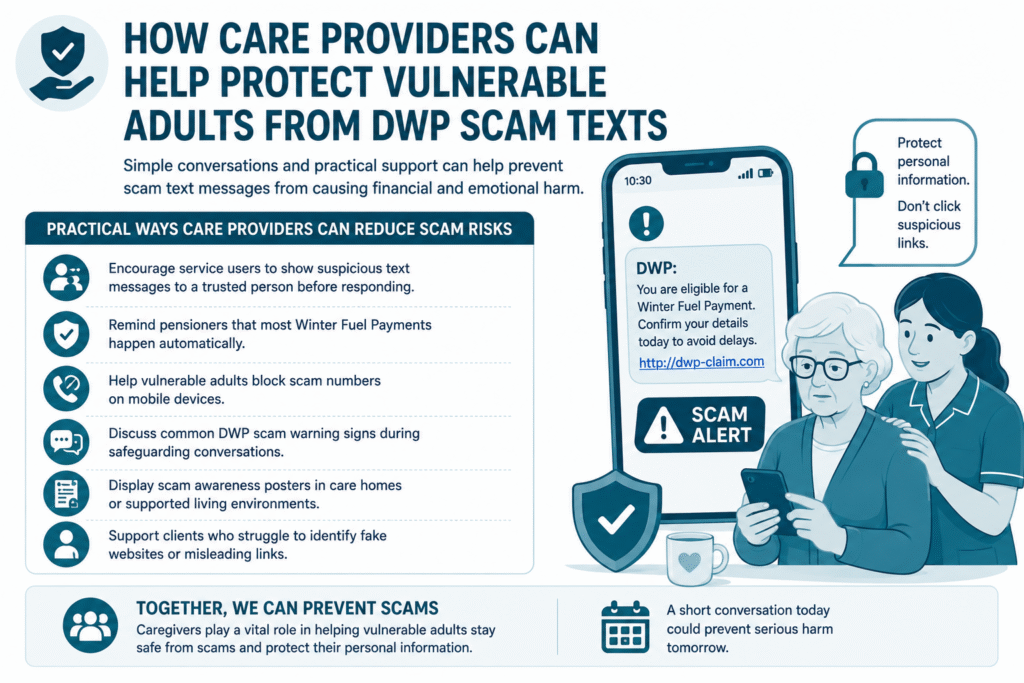

The Department for Work and Pensions (DWP) has issued a major dwp text message warning after a rise in winter fuel payment scams targeting older adults across the UK.

Fraudsters are sending fake text messages claiming pensioners must apply for a Winter Fuel Payment, Energy Allowance, or cost-of-living support payment by clicking a link and entering personal or bank details. These messages are scams designed to steal sensitive information.

Caregivers, family members, and care providers should remind vulnerable adults that most Winter Fuel Payments are automatic and the DWP will never ask for bank details through a text message.

Anyone who receives a suspicious DWP winter fuel payment text or winter fuel payment scam text should avoid clicking links, delete the message, and forward it to 7726 immediately.

Key Takeaways

- The recent dwp scam text surge mainly targets pensioners and vulnerable adults expecting Winter Fuel Payments or cost-of-living support.

- Most Winter Fuel Payment payments happen automatically, so recipients usually do not need to apply.

- The DWP does not ask for bank details, passwords, or card information through text messages.

- Many winter fuel payment scams create urgency by using fake deadlines or “claim now” messages.

- Caregivers and families should help older adults recognise suspicious messages and avoid clicking unknown links.

- Forward suspicious texts to 7726 for free to help mobile providers block scam numbers.

- If someone clicks a fraudulent link or shares personal details, they should contact their bank and report the incident to Action Fraud immediately.

Why Caregivers Need to Take This DWP Text Message Warning Seriously

Caregivers now play a critical role in protecting older adults from rising dwp scam activity linked to Winter Fuel Payments and other government support schemes. Criminals often target pensioners because many already expect messages about winter support, Attendance Allowance, PIP, or state pension changes during colder months.

Scammers also take advantage of confusion surrounding benefit updates, dwp benefit warning letters, and changing winter fuel payment eligibility rules. Many older adults react quickly when a message mentions heating costs, missed payments, or urgent deadlines. Fraudsters know this and use fear to pressure vulnerable people into clicking malicious links.

For care providers, domiciliary carers, and family members, this threat goes beyond financial loss. A successful scam can leave older adults distressed, embarrassed, and anxious about future support payments. Some victims may even hesitate to trust genuine government communications afterward.

Caregivers should regularly discuss common scam tactics with service users, especially anyone receiving a winter fuel payment, Attendance Allowance, PIP, or State Pension support. A simple conversation could prevent serious financial harm.

RELATED: DWP Benefit Scrapping 2026: Latest Update

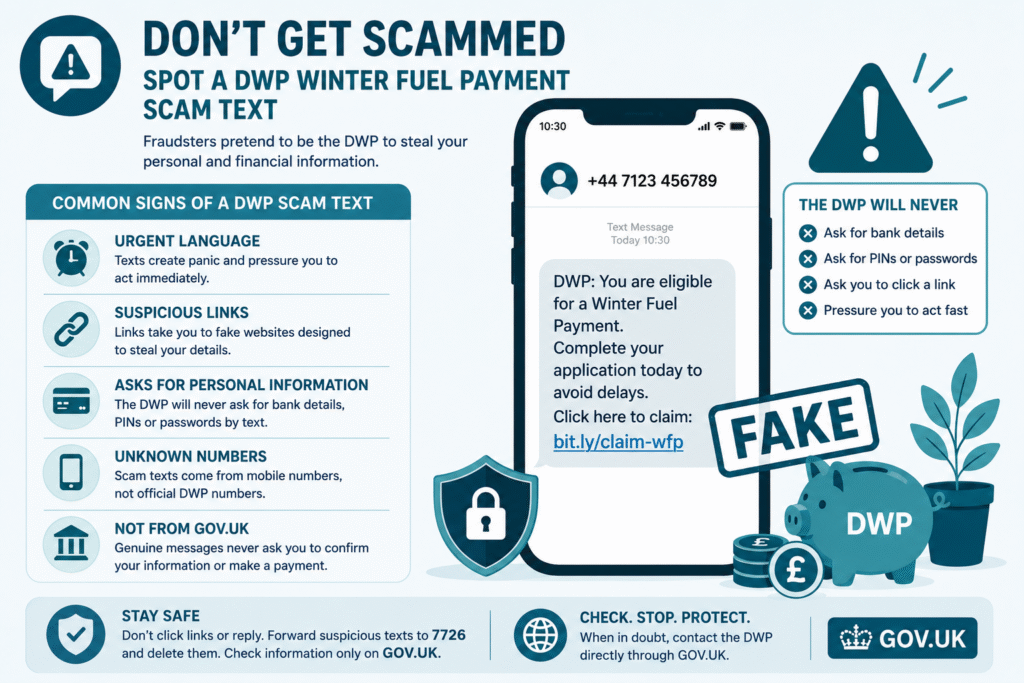

What Does a DWP Winter Fuel Payment Scam Text Look Like?

Most DWP winter allowance text scams follow a similar pattern. Fraudsters send messages claiming the recipient qualifies for a Winter Fuel Payment, Energy Allowance, or emergency winter heating support payment. The text usually creates urgency and asks the person to click a link before a fake deadline expires.

Some scam messages may mention:

- “Winter Fuel Payment application”

- “Energy Support Scheme”

- “Winter Heating Allowance”

- “Cost of Living Payment 2025”

- “National Insurance verification”

- “Claim your payment now”

A typical DWP text message example iPhone users report seeing might read: “DWP: You are eligible for a Winter Fuel Payment. Complete your application today to avoid delays. Click here to claim.”

These links often lead to fake government websites designed to steal bank details, passwords, or National Insurance information.

Common Signs of a DWP Scam Text

- The message asks for bank or card details

- It includes urgent language like “act now” or “final warning”

- The sender uses suspicious mobile numbers

- The link does not lead to an official GOV.UK website

- The text mentions fake schemes like a “dwp energy allowance text” or “winter heating allowance text”

- The message pressures the recipient to verify personal information immediately

Many older adults receive these scams on both Android devices and iPhones, which explains why searches for “do dwp send text messages on iPhone” and “dwp text message number” continue to rise across the UK.

READ MORE: NHS Pension Calculator: How to Estimate Retirement Income in 2026

Do DWP Send Text Messages on iPhone or Android?

The DWP may occasionally send legitimate text messages to remind people about appointments, claim updates, or application progress. However, genuine DWP messages do not ask people to click suspicious links, transfer money, or provide bank details through text messages.

This distinction matters because many pensioners now search questions like “do DWP send text messages on iPhone” or “how do I know if a text message from DWP is genuine” after receiving unexpected messages about Winter Fuel Payments or Attendance Allowance support.

How to Identify a Genuine DWP Message

A genuine DWP text message usually:

- relates to an existing claim or appointment

- avoids asking for sensitive financial information

- does not pressure the recipient with urgent deadlines

- directs users toward official GOV.UK services

- comes after previous contact or expected communication

By contrast, a DWP text message pension scam or DWP text message national insurance scam often pushes recipients to “confirm eligibility” or “unlock” payments immediately.

Caregivers should encourage older adults to pause before responding to any unexpected message. If a text feels suspicious, the safest option is to ignore the message and contact the DWP directly through official GOV.UK channels instead of using the number or link provided in the text.

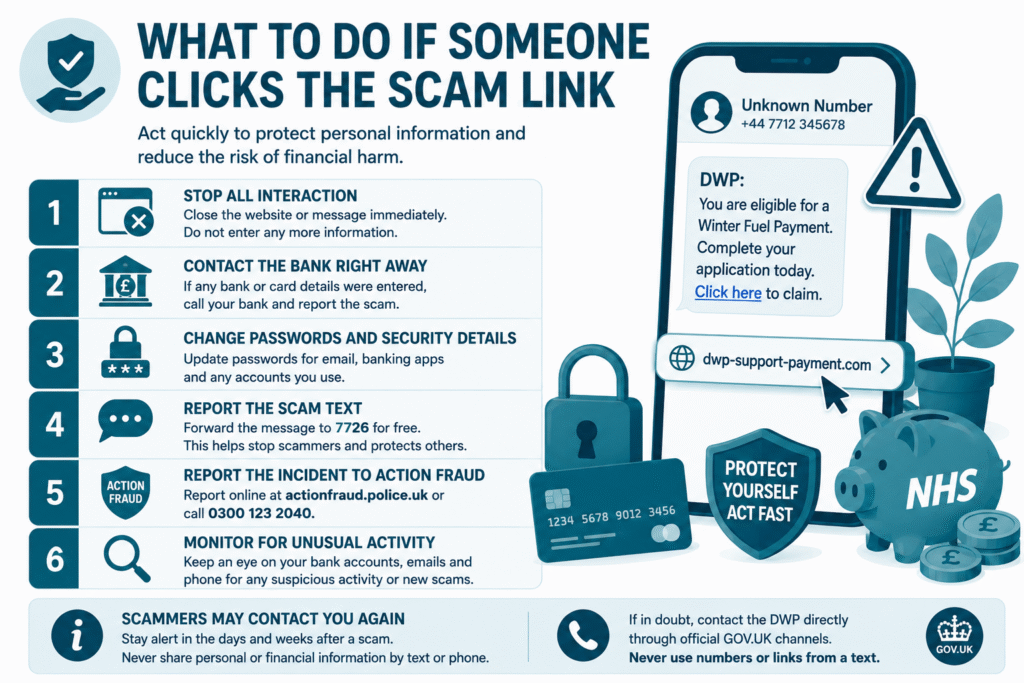

What Should Caregivers Do if Someone Clicks the Scam Link?

A quick response can reduce the damage caused by a DWP scam text or winter fuel payment scam text. Caregivers, relatives, and support workers should act immediately if an older adult clicks a suspicious link or shares personal information.

Steps to Take Immediately

- Stop all interaction with the website or sender

Close the webpage immediately and avoid entering any additional information.

- Contact the bank right away

If the person entered bank or card details, call the bank immediately and explain that fraudsters may have accessed the account.

- Change passwords and security details

Update passwords linked to email accounts, banking apps, or government services if login details were shared.

- Report the scam text

Forward the message to 7726 for free. Mobile providers use these reports to investigate and block scam numbers.

- Report the incident to Action Fraud

Action Fraud collects reports about scams and cybercrime across the UK. Reporting the incident may help prevent further fraud against vulnerable adults.

- Monitor for unusual activity

Caregivers should watch for unexpected bank transactions, suspicious calls, or additional scam attempts in the following days.

Many fraudsters continue targeting victims after an initial response, especially older adults receiving a winter fuel payment, Attendance Allowance, or State Pension support. Early action gives families and care providers the best chance of limiting financial harm.

SEE ALSO: End of Life Care at Home: What to Expect in 2026, Costs, and Family Support

How Care Providers Can Help Protect Vulnerable Adults From DWP Scam Texts

Care providers, domiciliary carers, and support workers often spot scam risks before family members do. Many vulnerable adults trust messages that appear to come from the government, especially when they mention a Winter Fuel Payment, Attendance Allowance, PIP, or State Pension support.

Care organisations should actively discuss common scam tactics during care visits, welfare checks, and support planning conversations. A short reminder about current winter fuel payment scams could stop someone from sharing sensitive information with fraudsters.

Practical Ways Care Providers Can Reduce Scam Risks

- Encourage service users to show suspicious text messages to a trusted person before responding

- Remind pensioners that most Winter Fuel Payments happen automatically

- Help vulnerable adults block scam numbers on mobile devices

- Discuss common DWP scam warning signs during safeguarding conversations

- Display scam awareness posters in care homes or supported living environments

- Support clients who struggle to identify fake websites or misleading links

Care teams should pay particular attention to adults who live alone, feel anxious about heating costs, or recently received state pensioners dwp warning letters or other benefit-related communications. Fraudsters often target people already worried about rising living expenses.

For many older adults, caregivers now serve as an important safety net against increasingly convincing DWP winter heating allowance text scams and fake cost-of-living payment messages.

Final Thoughts…

The recent DWP text message warning highlights how aggressively fraudsters now target older adults during winter support payment periods. Scammers continue using fake Winter Fuel Payment, Energy Allowance, and cost-of-living payment messages to create panic and steal personal information.

Families and caregivers should remember one key fact: most Winter Fuel Payments happen automatically, and the DWP will never ask for bank details or payment verification through a text message. Any unexpected message requesting urgent action, financial information, or account confirmation deserves immediate suspicion.

If you receive a suspicious DWP winter fuel payment text, do not click the link. Forward the message to 7726, delete it, and verify any concerns directly through official GOV.UK channels.

A simple warning conversation today could protect a vulnerable older adult from serious financial and emotional harm this winter.

Need Support Navigating Care, Compliance, or Safeguarding Challenges?

At Care Sync Experts, we help UK care providers stay informed, compliant, and prepared for emerging risks affecting vulnerable adults. From safeguarding guidance and compliance support to practical care industry insights, our team supports organisations that want to deliver safer, higher-quality care.

Explore more expert resources and caregiver support updates at Care Sync Experts.

FAQ

What are some signs that a phone call is actually a scammer?

Scam callers often create urgency and pressure people to act immediately. They may claim your Winter Fuel Payment, Attendance Allowance, or other DWP support will stop unless you confirm personal details straight away.

Fraudsters also frequently ask for bank information, passwords, PINs, or payment transfers. Genuine government representatives will not pressure you into making immediate financial decisions over the phone.

How do I know if a scammer is messaging me?

A scam message usually contains urgent wording, suspicious links, spelling mistakes, or requests for sensitive information. Many DWP scam text messages also promise unexpected payments or ask recipients to “verify” bank details to receive support. If a message pressures you to act quickly or directs you to a non-GOV.UK website, treat it as suspicious.

Does the DWP use WhatsApp?

The DWP does not normally use WhatsApp to request bank details, payment confirmations, or sensitive personal information. Fraudsters sometimes impersonate government departments through WhatsApp messages because many people trust the platform.

If someone claiming to represent the DWP contacts you through WhatsApp asking for financial information, you should treat the message as a potential scam.

How does a scammer know my name and phone number?

Scammers often collect personal information through data breaches, leaked contact lists, fake online forms, social media profiles, or previous phishing scams.

Some fraudsters also buy personal data from illegal sources online. Once they have basic details like your name, phone number, or age group, they can create convincing scam messages that appear more trustworthy to vulnerable adults and pensioners.