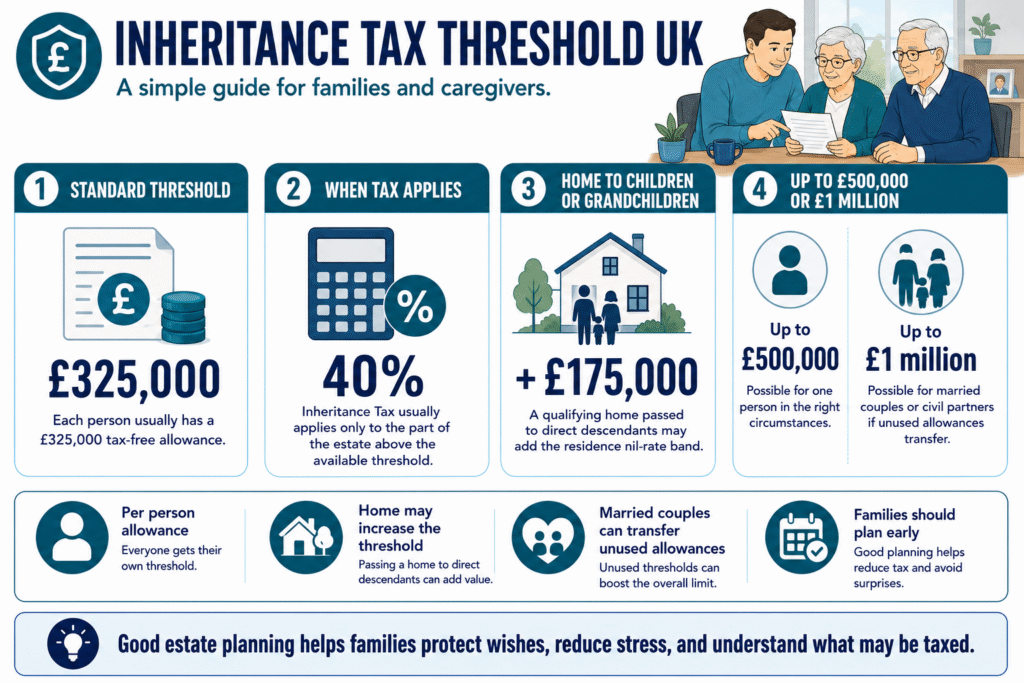

The inheritance tax threshold UK families usually start with is £325,000 per person. If an estate is worth more than the available threshold, HMRC usually charges Inheritance Tax at 40% on the amount above the threshold, not on the whole estate.

Some families can increase the tax-free amount. If someone leaves a qualifying home to their children or grandchildren, the estate may also use the residence nil-rate band, which can add up to £175,000. This can raise one person’s tax-free allowance to as much as £500,000.

Married couples and civil partners may also transfer unused allowances when the first partner dies. This means some couples can pass on up to £1 million tax-free, depending on their estate, property, and who inherits.

So, is inheritance tax per person? Yes, the basic threshold applies per person, but the final allowance depends on family circumstances. Families usually need to think about Inheritance Tax when the estate includes property, savings, investments, pensions, or valuable possessions above the available threshold.

Why Caregivers Should Understand Inheritance Tax Early

Caregivers often deal with more than care visits, medication, meals, and appointments. Many also help an elderly parent or vulnerable relative organise paperwork, understand bills, speak with professionals, and plan what happens next.

That is why inheritance tax planning matters. It can affect the family home, savings, pensions, gifts, and the money left to loved ones. When families delay the conversation, they often leave the hardest decisions until illness, care costs, or bereavement creates pressure.

An inheritance tax calculator or inheritance tax UK calculator can help families get a rough idea of possible exposure. However, calculators only work with the information you enter. They do not replace proper legal, financial, or tax advice.

Early planning gives families time to check the will, understand the estate, record wishes clearly, and avoid confusion later. Good planning does not only protect money. It protects peace of mind.

RELATED: What Disabilities Qualify for Council Tax Reduction? 2026

How the UK Inheritance Tax Threshold Works

The inheritance tax threshold UK families need to understand starts with the nil-rate band. This is the amount someone can usually leave before Inheritance Tax applies. For one person, the standard nil-rate band is £325,000.

If the estate goes above the available threshold, HMRC usually charges 40% only on the excess amount. For example, if someone has a £425,000 estate and only the £325,000 threshold applies, the taxable amount is £100,000.

The family home can change the calculation. If someone leaves a qualifying home to direct descendants, such as children or grandchildren, the estate may claim the residence nil-rate band. This can add up to £175,000, bringing one person’s possible tax-free threshold to £500,000.

Married couples and civil partners may transfer unused allowances. This can allow some families to pass on up to £1 million tax-free after the second death.

So, when do you have to pay inheritance tax? Usually, when the estate is worth more than the available allowances and the excess does not pass to an exempt beneficiary, such as a spouse, civil partner, charity, or community amateur sports club.

Inheritance Tax When the Second Parent Dies

Inheritance tax when second parent dies often worries families because the estate may now include the family home, savings, investments, personal possessions, and anything the first parent left behind.

When the first parent dies, they often leave everything to their spouse or civil partner. In that case, Inheritance Tax usually does not apply because transfers between spouses and civil partners are normally exempt. Their unused allowance can also pass to the surviving partner.

The issue usually comes later. Inheritance tax when second parent dies UK families should check depends on the total value of the second parent’s estate and how much unused allowance transferred from the first parent.

For example, if both parents were married or in a civil partnership and left the family home to their children, the estate may be able to use two nil-rate bands and two residence nil-rate bands. This can give a possible tax-free allowance of up to £1 million.

Unmarried partners do not get the same automatic spouse or civil partner exemption, even if they lived together for many years. That is why families should review wills, property ownership, and estate plans before a crisis.

READ MORE: Is Carers Allowance Taxable in 2026?

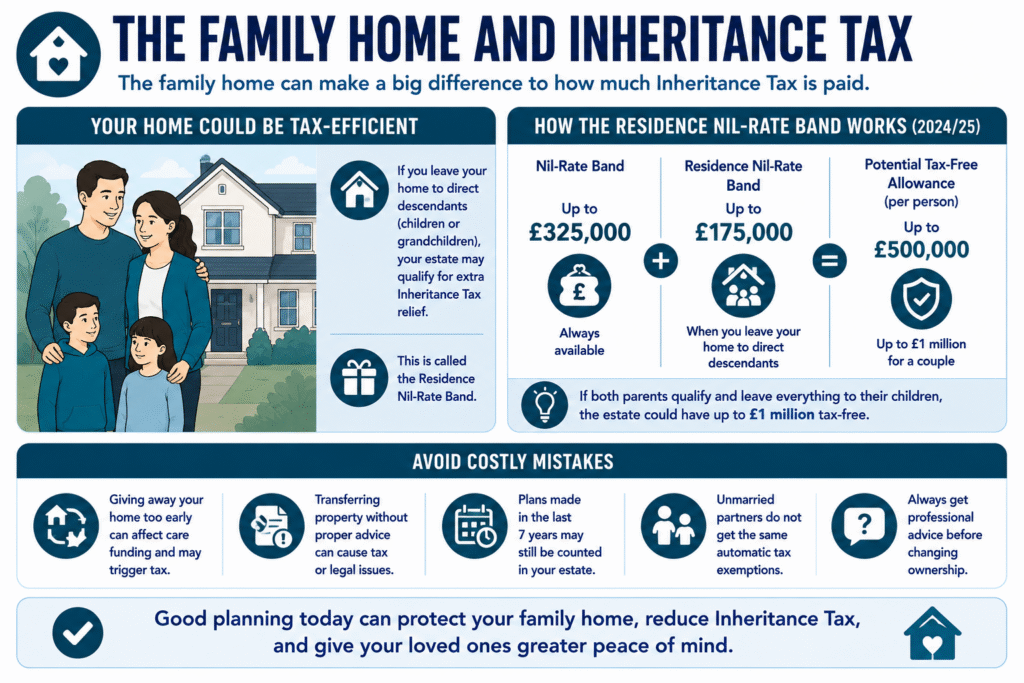

What Happens to the Family Home?

The family home often makes the biggest difference to Inheritance Tax. If someone leaves their home to children or grandchildren, the estate may qualify for the residence nil-rate band. This can add up to £175,000 on top of the standard £325,000 threshold.

This is why families often ask how to avoid inheritance tax on a property. The safer way to ask is: how can we use the legal allowances properly? The answer depends on who inherits the home, the total value of the estate, whether the person had a valid will, and whether the estate falls within the residence nil-rate band rules.

Caregivers should start this conversation early, especially when an elderly parent may need home care, live-in care, or a care home later. Property decisions can affect care planning, estate planning, and family expectations.

Trying to give away a home at the wrong time can create tax, legal, or care funding problems. Families should get proper advice before transferring property, changing ownership, or making major gifts. Legal planning can reduce Inheritance Tax, but rushed decisions can create bigger problems later.

Gifts, Savings, and Pensions: What Families Often Miss

Gifts, savings, and pensions can change the Inheritance Tax picture, so families should not only focus on the house.

Savings usually form part of the estate. So, if someone asks, do I have to pay tax on my savings UK, the answer depends on the type of tax. Savings interest may create Income Tax during life, while the savings balance may count towards Inheritance Tax after death.

Gifts also need careful planning. Families often ask how much money can you gift tax free because they want to reduce the estate legally. Some gifts fall within annual exemptions, while larger gifts may only fall outside the estate if the person lives for seven years after giving them.

Pensions need extra attention too. People often ask, do you pay tax on pension or how much tax will I pay on my pension. Pension income can count as taxable income during life, but pension pots also have separate death benefit rules. From April 2027, most unused pension funds and death benefits are expected to come within Inheritance Tax rules, so families should review pension planning early.

Pension contributions may also reduce taxable income in some situations. That is why people ask, do pension contributions reduce your taxable income UK. The answer can depend on the pension type, income level, and tax position, so proper advice matters.

SEE ALSO: Universal Credit Permanent Boost 2026

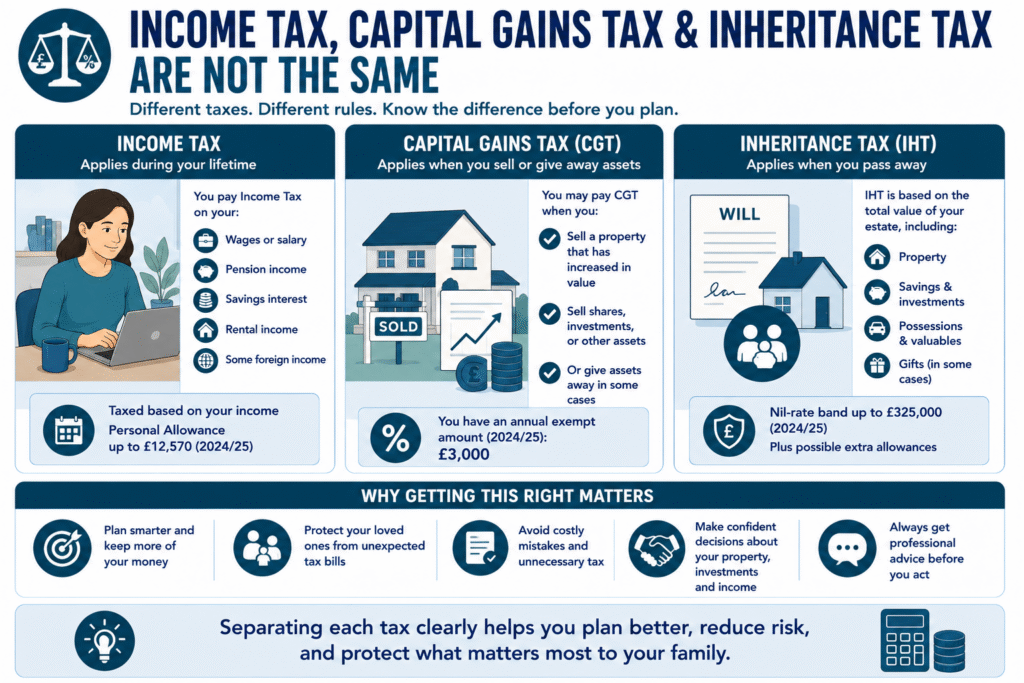

Income Tax, Capital Gains Tax, and Inheritance Tax Are Not the Same

Families often mix up different UK taxes when they start planning later life finances. Inheritance Tax applies to an estate after someone dies. Income Tax applies to money someone receives during life, such as wages, pension income, savings interest, rental income, or some foreign income. Capital Gains Tax may apply when someone sells or gives away an asset that has increased in value.

So, questions like how much do you need to earn to pay tax, what is the higher tax bracket, and how much can a pensioner earn before paying tax UK relate to Income Tax, not Inheritance Tax.

Questions like how much foreign income is tax-free in UK or how to avoid capital gains tax UK also sit outside the main Inheritance Tax rules. They may still matter when families plan property sales, overseas income, investments, or retirement income.

The safest approach is to separate each issue clearly. Work out the estate value for Inheritance Tax, income sources for Income Tax, and asset sales for Capital Gains Tax. Then get proper advice before making major financial decisions.

How Families Can Reduce Inheritance Tax Legally

Families often search how to avoid inheritance tax UK, but the better goal is to reduce the bill legally and plan early. Inheritance Tax planning works best when families make clear decisions before illness, care pressure, or bereavement forces action.

Start with a valid will. A will helps the family understand who should inherit, who should manage the estate, and how the person wants their money, property, and possessions handled. If you wonder how much does a will cost UK, the price can vary depending on whether the will is simple, complex, or written with tax and trust planning advice.

Families can also use spouse or civil partner exemptions, review property ownership, understand gifting rules, keep records of gifts, and consider charitable giving. Some estates may qualify for a reduced Inheritance Tax rate if enough of the estate goes to charity.

Many people search Martin Lewis inheritance tax because they want plain-English guidance. The key lesson is simple: understand your allowances early, check whether the family home qualifies for extra relief, and do not leave planning until the second parent dies.

Legal planning can help reduce Inheritance Tax. Rushed decisions, hidden transfers, or poor records can create stress, disputes, and unexpected tax problems.

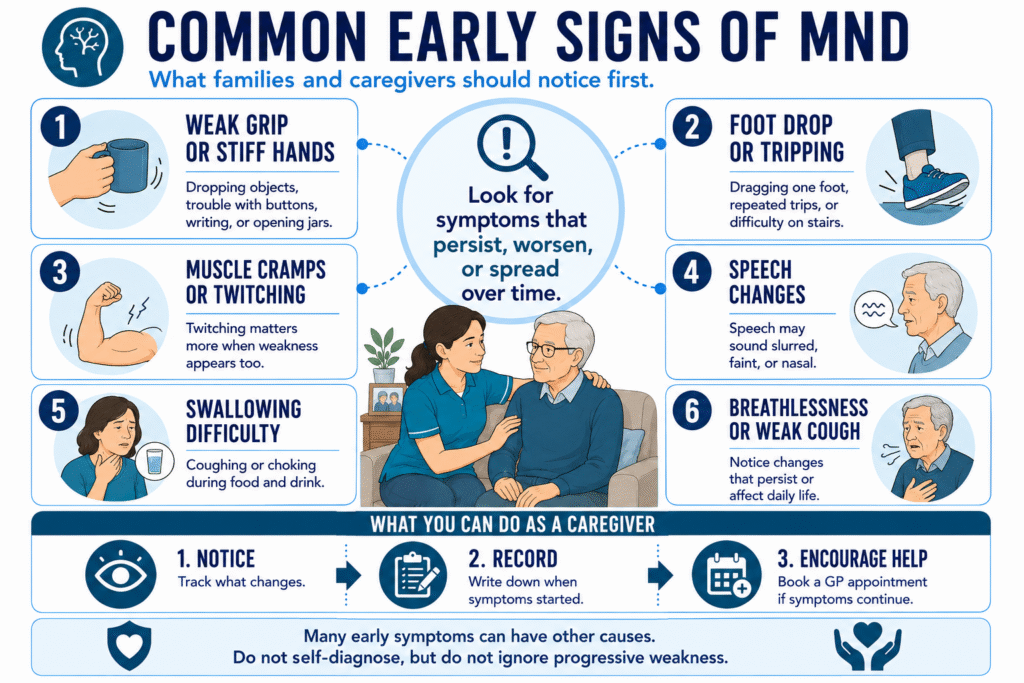

MORE: Early Sign of MND in 2026: What Care Businesses Should Notice First

Final Advice for Caregivers and Families

The best time to talk about Inheritance Tax is before a crisis. Caregivers often see the warning signs first: an elderly parent forgets paperwork, care needs increase, bills pile up, or the family starts asking what should happen to the house.

Do not wait until the second parent dies before checking the will, savings, property, pensions, and records of gifts. Start early, involve the right professionals, and keep clear notes so the family does not have to guess later.

Good planning does more than reduce tax. It protects the person’s wishes, helps families avoid conflict, and gives everyone more confidence when difficult decisions arise.

The inheritance tax threshold UK families can use depends on the estate, family structure, home ownership, and legal planning. When in doubt, get regulated financial or legal advice before making major decisions.

Need Help Making Sense of Inheritance Tax and Later-Life Planning?

Inheritance Tax, care costs, wills, pensions, and family property decisions can feel overwhelming when you are supporting an elderly parent or vulnerable loved one.

At Care Sync Experts, we explain care and family support topics in plain English, helping caregivers make clearer, calmer decisions before a crisis begins.

Plan early. Protect wishes. Reduce family confusion.

FAQ

What is a good monthly retirement income in the UK?

A good monthly retirement income depends on lifestyle, housing costs, health needs, and whether someone lives alone or as a couple.

As a guide, the Retirement Living Standards show that a comfortable retirement costs about £45,400 a year for one person and £62,700 for a couple, which works out at roughly £3,783 per month for one person or £5,225 per month for a couple before adjusting for personal circumstances.

How much does a will cost in the UK?

The cost of a will depends on how simple or complex the estate is. MoneyHelper says a straightforward solicitor-written will often costs around £180 to £420, while a more complex will may cost £420 to £900 at a high street firm, or more at larger firms.

Families dealing with property, inheritance tax, second marriages, care planning, or trusts should consider regulated legal advice rather than relying only on a cheap template.

What is the higher tax bracket in the UK?

For England, Wales, and Northern Ireland, the higher Income Tax rate starts when taxable income goes above £50,270. The higher rate is 40% on taxable income from £50,271 to £125,140. Scotland uses different Income Tax bands and rates for Scottish taxpayers.

How much foreign income is tax-free in the UK?

For UK residents, foreign income is generally taxable in the UK, but the rules changed from 6 April 2025. GOV.UK says the remittance basis was abolished and replaced with a residence-based Foreign Income and Gains regime.

Some qualifying new residents may claim relief and pay no UK tax on eligible foreign income and gains for up to four years, but this depends on strict conditions.