Income taxation UK rules affect more than monthly wages. They can affect care workers, family carers, pensioners, people receiving benefits, and families who need to plan the cost of care at home.

For the 2026/27 tax year, most people can earn up to £12,570 before they pay Income Tax. This is the standard personal tax allowance 2026.

In England, Wales, and Northern Ireland, income above that allowance falls into the 20%, 40%, or 45% tax bands, depending on how much taxable income someone has. Scotland uses different bands for employment and pension income.

For caregivers and families, tax matters because income can come from different places. A paid carer may receive wages through PAYE. A family carer may claim Carer’s Allowance.

An older person may receive State Pension, private pension income, savings interest, or benefits. Some of these count as taxable income, while others do not. GOV.UK lists Carer’s Allowance and State Pension as taxable benefits.

Understanding Income Tax helps families ask better questions: how much can you earn before tax, how much do you take home, which benefits count as taxable income, and whether pension or savings income may affect the amount owed.

For anyone arranging care, those answers can make budgeting clearer and reduce stressful surprises later.

When Does the New Tax Year Start?

The UK tax year starts on 6 April and ends on 5 April the following year. So, the 2026/27 tax year runs from 6 April 2026 to 5 April 2027.

This date matters because tax allowances, benefit rates, pension rules, and tax bands usually follow the tax year, not the calendar year. If you work in care, claim Carer’s Allowance, receive pension income, or support an older person with their finances, the new tax year can affect how much tax someone pays.

Families often ask, when does the new tax year start because they want to plan wages, pension income, savings interest, or care costs properly. A simple yearly check can help you spot changes early and avoid confusion later.

RELATED: Earned Income Disallowance: Benefits & Allowances (2026 Guide)

How Much Can You Earn Before Tax?

Most people can earn up to £12,570 in the 2026/27 tax year before paying Income Tax. This is the personal tax allowance 2026, and it means the first £12,570 of taxable income usually falls into the 0% tax band.

For caregivers and families, this matters because taxable income can come from wages, pension income, Carer’s Allowance, rental income, self-employment, or savings interest above certain allowances. So when someone asks, how much can you earn before tax, the simple answer is £12,570 for most people, but the full answer depends on the type and total amount of income they receive.

Pensioners usually use the same Personal Allowance. That means the answer to how much can a pensioner earn before paying tax UK is also generally £12,570 in taxable income for 2026/27. However, State Pension, private pensions, work income, and some benefits can all count towards that total.

If someone’s adjusted net income goes above £100,000, HMRC reduces their Personal Allowance by £1 for every £2 above that limit. Once income reaches £125,140, the Personal Allowance becomes zero.

UK Income Tax Rates 2026/27 and Tax Brackets

The main UK income tax rates 2026/27 for England, Wales, and Northern Ireland are simple once you separate your tax-free income from your taxable income.

| Band | Taxable income | Tax rate |

| Personal Allowance | Up to £12,570 | 0% |

| Basic rate | £12,571 to £50,270 | 20% |

| Higher rate | £50,271 to £125,140 | 40% |

| Additional rate | Over £125,140 | 45% |

These are the main UK tax brackets 2026 for most taxpayers outside Scotland. Scotland uses different Income Tax bands for employment income, pension income, and some other taxable income, so Scottish taxpayers should check the Scottish rates separately.

It helps to remember that Income Tax works in layers. You do not pay one tax rate on everything you earn. For example, if a care manager earns enough to enter the higher-rate band, only the part above the higher-rate threshold gets taxed at 40%.

This matters for caregivers, pensioners, and families because taxable income can come from more than one place. Wages, State Pension, private pensions, taxable benefits, rental income, and some savings interest can all affect which band someone falls into.

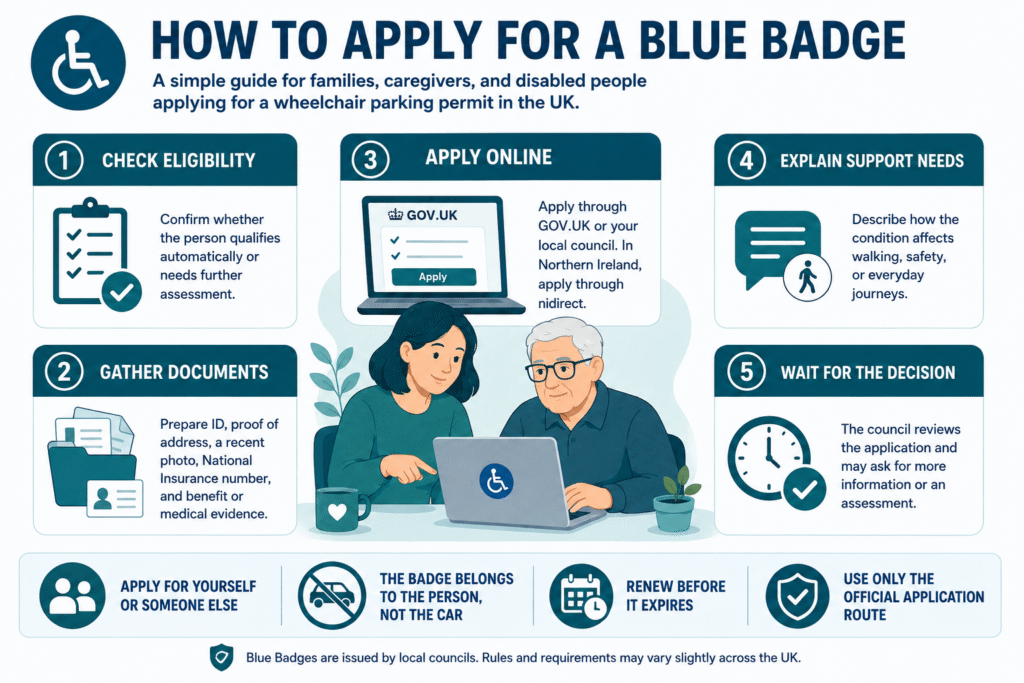

READ MORE: Wheelchair Parking Permit UK: Who Qualifies for a Blue Badge in 2026?

What Is the 40% Tax Bracket?

The 40% tax bracket is the higher-rate Income Tax band. In England, Wales, and Northern Ireland, you usually enter this band when your taxable income goes above £50,270 in the 2026/27 tax year.

People often ask, what is the 40 tax bracket or when do you pay 40 tax because they worry that all their income will suddenly get taxed at 40%. That is not how it works.

You only pay 40% on the part of your income that falls inside the higher-rate band. For example, if a senior care worker, care manager, or self-employed care consultant earns above the higher-rate threshold, the income below the threshold still uses the lower bands. Only the income above the threshold faces the 40% rate.

This makes a big difference when planning care wages, extra shifts, pension income, or private work. A pay rise can still leave you better off, but it may also change your tax band, savings allowance, or take-home pay.

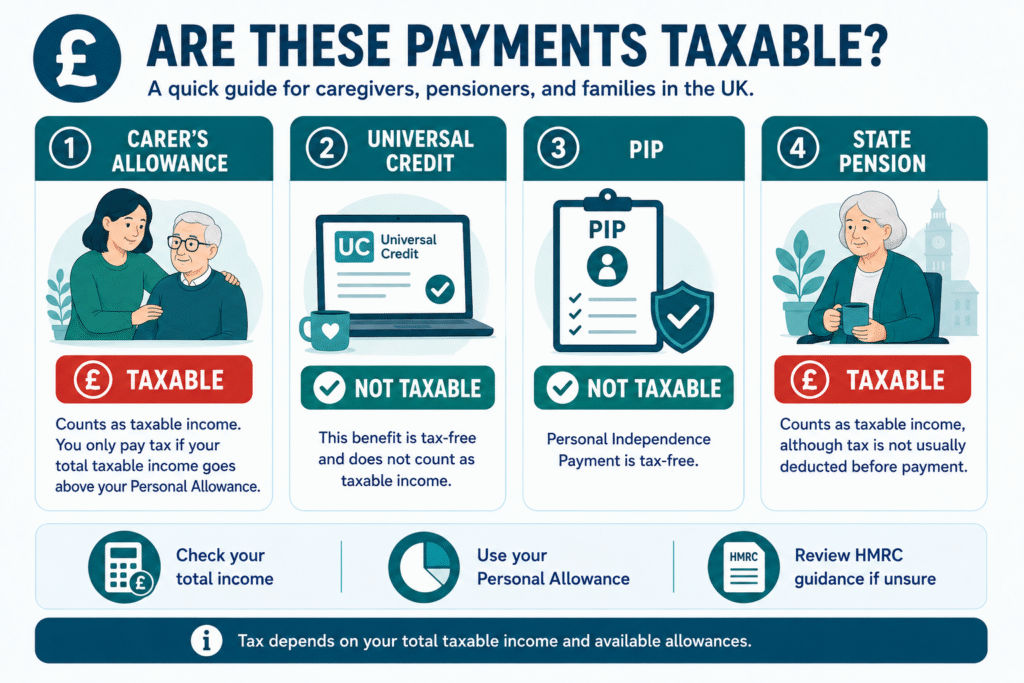

Is Carer’s Allowance, Universal Credit or PIP Taxable?

Caregivers and families often deal with more than wages. They may also manage benefits, pensions, savings, and care-related payments. Some of these count as taxable income, and some do not.

| Payment | Taxable? | What this means |

| Carer’s Allowance | Yes | It counts as taxable income, but you only pay tax if your total taxable income goes above your allowance. |

| Universal Credit | No | It does not count as taxable income. |

| PIP | No | Personal Independence Payment is tax-free. |

| State Pension | Yes | It counts as taxable income, although tax is not usually deducted before payment. |

GOV.UK lists Carer’s Allowance and the State Pension as taxable state benefits. It also lists Universal Credit and Personal Independence Payment, PIP, as tax-free benefits.

So, if you ask is Carer’s Allowance taxable, the answer is yes. If you ask is Universal Credit taxable or is PIP taxable, the answer is no. For pensioners, the key point is simple: the State Pension is taxable, but tax only becomes due if total taxable income rises above the Personal Allowance.

SEE ALSO: Working Tax Credit: What Replaced It and What You Can Claim in 2026

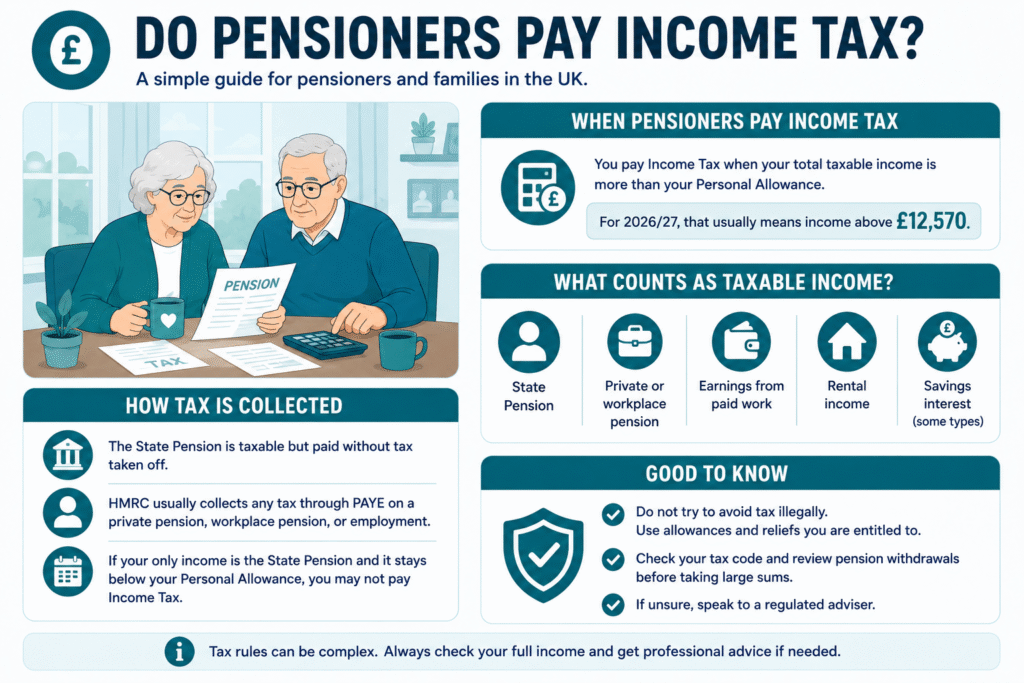

Do Pensioners Pay Income Tax?

Pensioners pay Income Tax when their total taxable income goes above their Personal Allowance. For 2026/27, that usually means income above £12,570. This can include State Pension, private pensions, workplace pensions, earnings, rental income, and some savings interest.

Many families ask, do you pay tax on State Pension or is the State Pension taxable. The answer is yes: State Pension counts as taxable income. However, the Department for Work and Pensions pays it without deducting tax first. HMRC usually collects any tax due through PAYE on a private pension, workplace pension, or employment income.

A pensioner whose only income is the State Pension may not pay Income Tax in practice if their yearly income stays below the Personal Allowance. But if they also receive a private pension, paid work income, rental income, or taxable savings interest, their total income may cross the tax-free limit.

People also ask how to avoid paying tax on your pension. The safest answer is: do not avoid tax illegally. Instead, use legitimate allowances, understand your tax code, check pension withdrawals before taking large sums, and ask a regulated adviser before making major pension decisions.

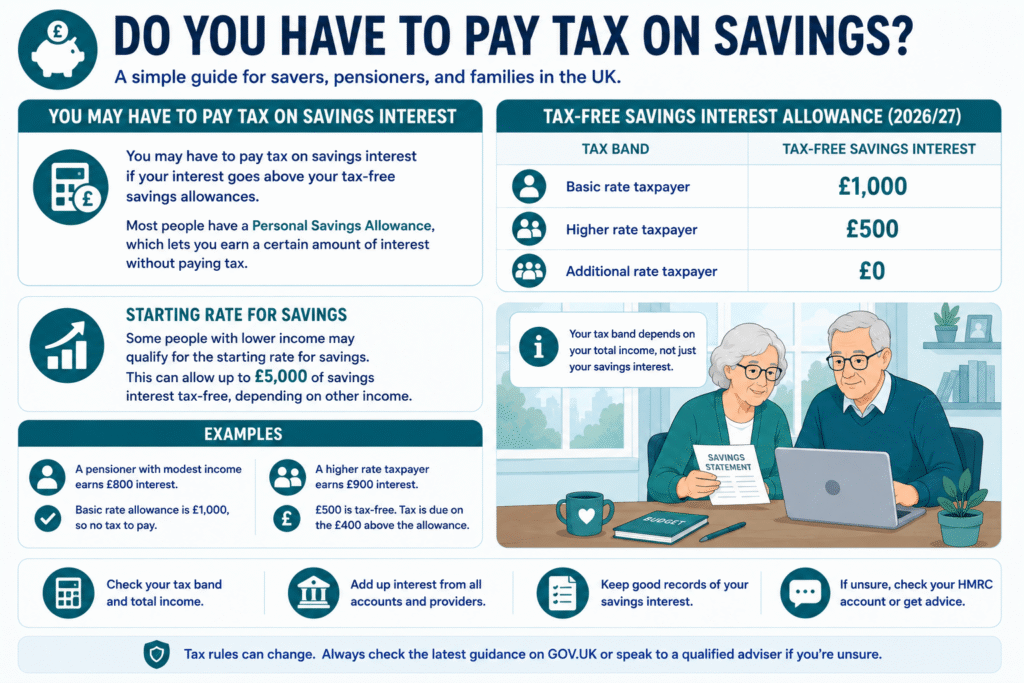

Do You Have to Pay Tax on Savings?

You may have to pay tax on savings interest if your interest goes above your tax-free savings allowances. This matters for pensioners, family carers, and people saving towards care costs because bank interest can still count as taxable income.

Most people have a Personal Savings Allowance. Basic-rate taxpayers can usually earn up to £1,000 in savings interest tax-free. Higher-rate taxpayers can usually earn up to £500 tax-free. Additional-rate taxpayers do not get a Personal Savings Allowance. GOV.UK also explains that some people with lower income may qualify for the starting rate for savings, which can allow up to £5,000 of savings interest tax-free, depending on other income.

| Tax band | Tax-free savings interest |

| Basic rate | £1,000 |

| Higher rate | £500 |

| Additional rate | £0 |

So, if you ask do you have to pay tax on savings or how much interest can I earn tax free, the answer depends on your total income and tax band. A pensioner with modest income may pay no tax on savings interest, while someone in the higher-rate band may pay tax once interest goes above £500.

MORE: What Is the Retirement Age UK for Female Workers in 2026?

Income Tax in UK for Foreigners Working in Care

Foreign care workers may pay UK Income Tax if they work in the UK or become UK tax resident. In most care jobs, employers deduct Income Tax through PAYE before paying wages, just as they do for UK workers.

The phrase income tax in UK for foreigners can cause confusion because tax does not depend only on nationality. HMRC looks at where someone lives, where they work, their residency status, and the source of their income. GOV.UK explains that non-residents usually pay UK tax only on UK income, while UK residents normally pay UK tax on income from the UK and abroad.

For overseas care workers, the simple rule is this: if you earn wages from a UK care employer, expect UK tax and National Insurance to apply. If you also receive income from another country, such as rent, pension income, investments, or business income, you may need extra advice.

Care providers should also help international staff understand payslips, tax codes, pension deductions, and HMRC letters. Clear guidance reduces stress and helps workers focus on delivering safe, reliable care.

How Much Would I Earn After Tax?

Your take-home pay depends on more than your gross salary. Income Tax, National Insurance, pension contributions, student loan repayments, tax code changes, and workplace deductions can all affect what lands in your bank account.

This is why many care workers and families ask, how much would I earn after tax or how much do I take home. The quickest way to estimate this is to use a reliable UK tax income calculator or check your HMRC personal tax account. GOV.UK also provides tools to help people check Income Tax, tax codes, and estimated pay.

For care workers, this matters when comparing jobs, overtime, sleep-in shifts, weekend rates, or promotion into senior care roles. A higher wage can increase take-home pay, but it may also affect tax bands, National Insurance, pension deductions, or means-tested benefits.

Families arranging care should also think carefully about take-home income. If an older person receives pension income, savings interest, or taxable benefits, their actual disposable income may affect how they plan private care, home support, or contributions towards care costs.

ALSO: How to Report Benefit Fraud in the UK (2026)

What About UK Income Tax Rates from 1980 to Present?

UK Income Tax rates from 1980 to present have changed many times. Governments have adjusted allowances, basic-rate bands, higher-rate thresholds, dividend tax, savings rules, and pension-related tax treatment over the years.

For most caregivers, pensioners, and families, the current rules matter most. If you want to plan wages, care costs, Carer’s Allowance, pension income, or savings interest, focus on the tax year you are actually in. For this article, that means the UK income tax rates 2026/27 and the current Personal Allowance.

Historical tax rates can still help if you want to compare long-term policy changes, understand frozen thresholds, or review older pension and employment records. HMRC publishes current and previous Income Tax rates and allowances, which is the best place to check UK income tax rates 1980 to present instead of relying on outdated summaries.

Final Thoughts…

Tax may not feel like a care issue at first, but it often affects care decisions. It can shape how much a care worker takes home, how a family carer manages Carer’s Allowance, how a pensioner budgets for support, and how families plan long-term care costs.

The best approach is simple: check income, benefits, pensions, savings interest, and allowances before making major financial decisions. Do not guess based on one payment alone. Look at the full picture because several small income sources can push someone above their tax-free allowance.

For caregivers, this means checking payslips, tax codes, overtime, and pension deductions. For pensioners, it means understanding whether State Pension, private pension income, savings, or part-time work may create a tax bill. For families arranging care, it means planning with clear numbers rather than assumptions.

Income taxation UK rules can feel confusing, but they become easier when you break them down by income type. Use official calculators, keep records, read HMRC letters carefully, and get professional advice when income, pensions, overseas earnings, or care funding becomes complex. The more clearly you understand tax, the better you can plan safe, affordable, and sustainable care.

Need Clearer Guidance on Tax, Care, and Family Finances?

Income tax can affect care workers, family carers, pensioners, and families planning support at home.

At Care Sync Experts, we make complex care-related topics easier to understand, from taxable benefits and pensions to allowances, take-home pay, and everyday care planning.

If tax, benefits, or pension income could affect someone you support, do not rely on guesswork. Check the rules, use official tools, and make care decisions with clearer financial confidence.

Care Sync Experts helps caregivers and families plan safer, smarter, and more informed care across the UK.

FAQ

Can I gift money to my wife?

Yes. In the UK, you can usually gift money to your wife, husband, or civil partner without Inheritance Tax, as long as you both live permanently in the UK. GOV.UK says there is no Inheritance Tax to pay on gifts between spouses or civil partners.

This means questions like “how much money can I transfer to my spouse in the UK?” or “how much money can I give my wife without paying taxes?” usually have a simple answer: transfers between UK-domiciled spouses or civil partners are normally exempt. Complex cases, such as non-UK domicile, large assets, divorce, trusts, or care-fee planning, need professional advice.

What is the Marriage Allowance in the UK?

Marriage Allowance lets one spouse or civil partner transfer £1,260 of their Personal Allowance to the other person. It can reduce the recipient’s tax bill by up to £252 in the tax year.

It usually helps when one partner earns less than the Personal Allowance, and the other pays basic-rate tax. GOV.UK explains that the person transferring the allowance reduces their own Personal Allowance, while their partner gets the tax reduction.

Does anyone pay 60% tax in the UK?

There is no official 60% Income Tax band, but some people face an effective 60% marginal rate between £100,000 and £125,140. This happens because the Personal Allowance reduces by £1 for every £2 of adjusted net income above £100,000.

So the person pays 40% higher-rate tax and also loses part of their tax-free allowance at the same time. GOV.UK confirms the Personal Allowance taper above £100,000 and that it becomes zero at £125,140.

How much tax do I pay on a £57,000 salary?

For England, Wales, or Northern Ireland in 2026/27, a £57,000 salary with the standard Personal Allowance would create about £10,232 in Income Tax before considering pension contributions, student loans, benefits, or tax code changes.

Estimated employee National Insurance would be about £3,151, giving rough take-home pay of about £43,617 per year, before workplace pension or other deductions. This uses the 2026/27 Income Tax bands and employee NI rates published by GOV.UK.