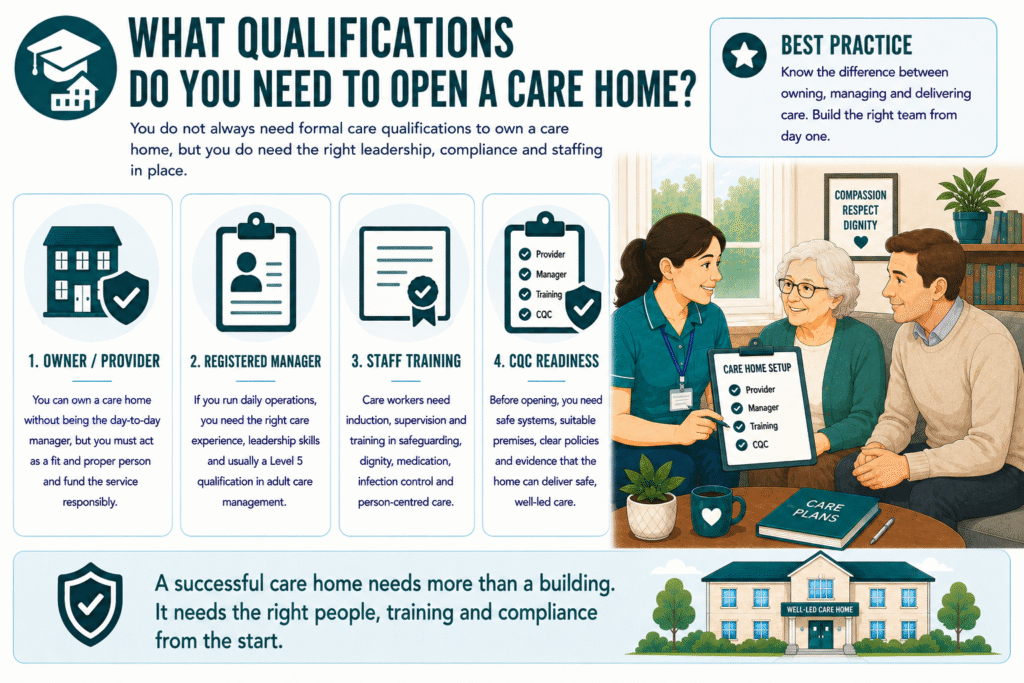

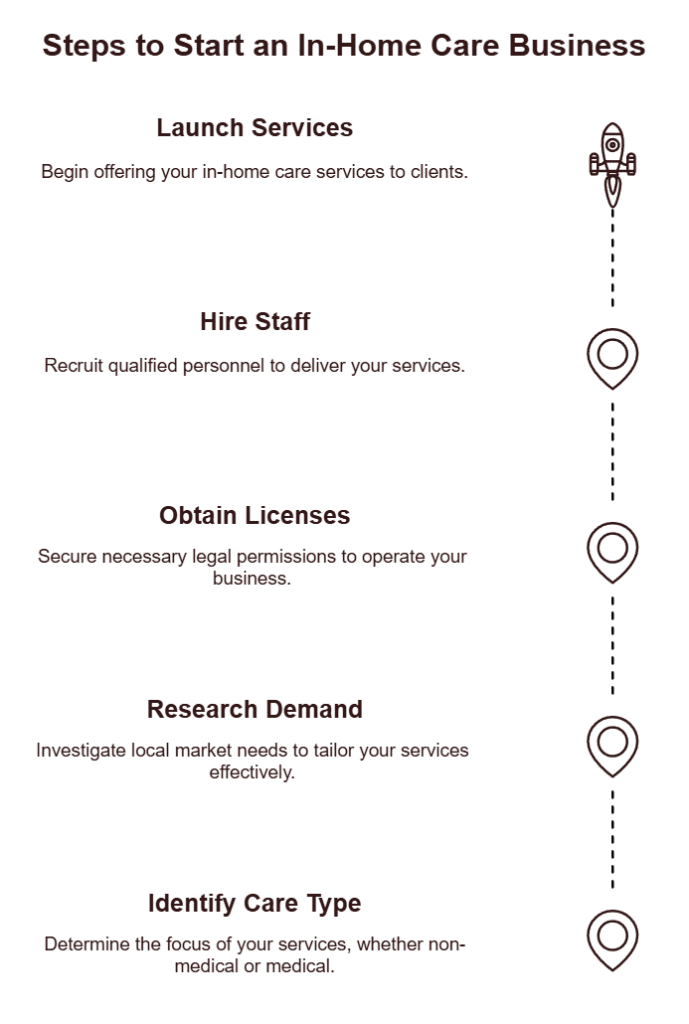

If you are asking, “what qualifications do you need to open a care home?”, the honest answer is this: you do not always need formal care qualifications to own one.

You can own a care home as an investor, director or provider, but you must prove that you understand the responsibility that comes with running a regulated care business.

The Care Quality Commission will expect you to act as a fit and proper person, show financial stability, meet legal requirements and put safe systems in place before you provide care.

If you plan to manage the home yourself, you will need the right care experience, leadership skills and usually a recognised management qualification. If you will not manage daily operations, you must appoint a competent Registered Manager.

Opening a care home is not just a property project. You are building a service where people live, receive support and trust your team with their safety, dignity and wellbeing.

A nursing home carries greater responsibility than a residential care home because residents may need regular clinical support. If you want to run a nursing home, you must understand personal care, nursing oversight, medication risks, clinical governance, staffing levels and safe escalation when a resident’s health changes.

You do not have to be a nurse to own a nursing home, but the service must have the right nursing leadership in place. Registered nurses must support residents who need nursing care, and the Registered Manager must show the experience, competence and judgement needed to manage a higher-risk service.

This is where many new owners make a costly mistake. They focus on the building, beds and occupancy plan, but underestimate the clinical responsibility. The Care Quality Commission looks closely at whether nursing homes can keep people safe, meet complex needs and prove that staff have the right skills for the residents they support.

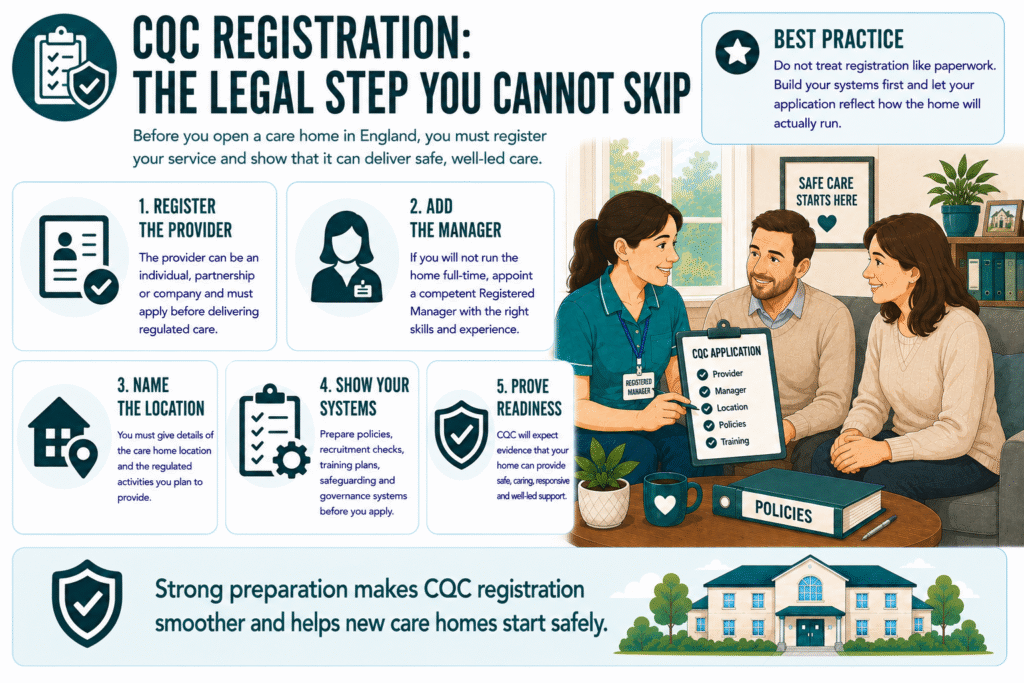

Before you open a care home in England, you must register with the Care Quality Commission. You cannot start providing regulated care first and sort out registration later. The provider, whether an individual, partnership or company, must apply and show that the service can meet the required standards.

Your application must explain the type of care you plan to provide, the location you will operate from, the regulated activities you want to deliver and the people who will manage the service. You also need strong policies, safe recruitment processes, suitable premises, financial planning and clear evidence that you can protect residents from avoidable harm.

CQC registration is not just paperwork. It tests whether your care home has the leadership, systems and culture needed to provide safe, caring and well-led support from the first day residents move in.

Care Certificate, Staff Training and Care Standards

Your care home will only run safely if your staff know what good care looks like in practice. The Care Certificate UK gives new care workers a clear foundation in the behaviours, knowledge and skills expected in adult social care. It covers key care certificate standards such as safeguarding, dignity, privacy, communication, infection prevention, duty of care and person-centred support.

However, the Care Certificate is only the starting point. Your team also needs role-specific training based on the residents you support. This may include dementia care, medication, moving and handling, nutrition, falls prevention, fire safety, mental capacity, end-of-life care and accurate record keeping.

Strong owners build a learning culture early. They do not wait for problems before training staff. They use supervision, spot checks, team meetings and care plan reviews to keep health and social care standards visible every day.

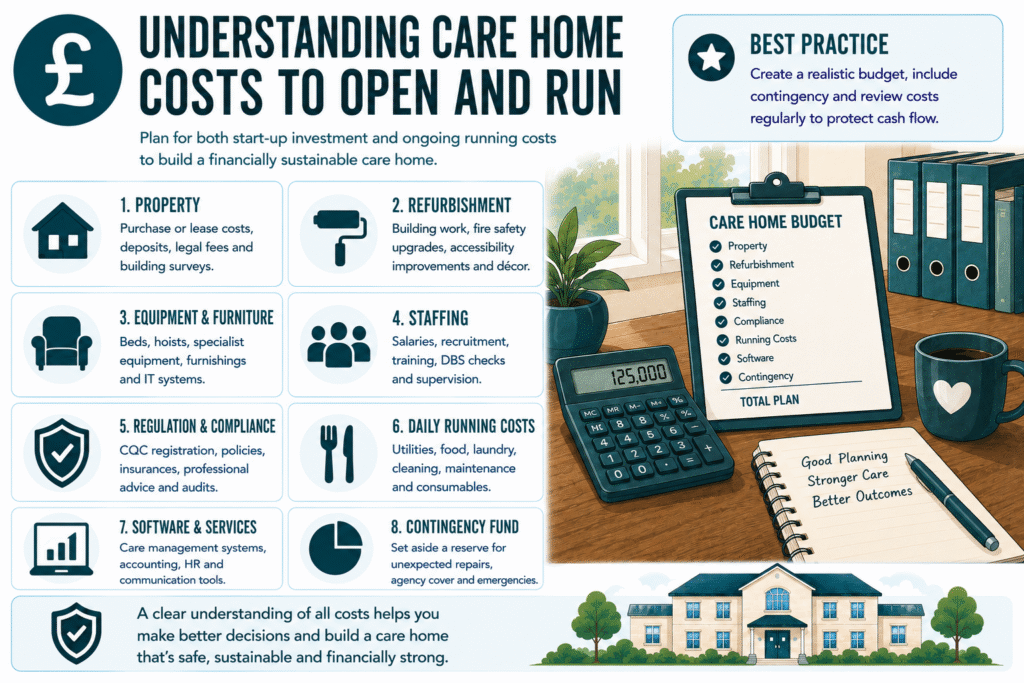

The cost of care homes varies widely because every project starts from a different point. Buying an existing care home, converting a suitable building and building from scratch all carry different costs, risks and timelines. Before you commit, you need to understand both the start-up cost and the monthly running cost.

Your main costs may include property purchase or lease, refurbishment, fire safety work, equipment, furniture, insurance, staff wages, recruitment, training, professional advice, CQC preparation, software, utilities, food, laundry, maintenance and contingency funds.

When people ask, “how much does a care home cost?”, they often focus only on the building. A stronger business owner looks at occupancy, local authority fee rates, private-pay demand, staffing ratios and cash flow. A care home can look profitable on paper and still struggle if wages, agency cover, repairs or low occupancy drain the budget.

Care Home Activities, Resident Experience and Family Trust

Understanding care home costs

Families do not choose a care home because it has beds available. They choose the home that makes them feel their loved one will live safely, comfortably and with dignity. That means your care model must go beyond compliance.

Care home activities play a major role in resident wellbeing. Good activities help people stay socially connected, maintain routines, enjoy hobbies, celebrate identity and reduce loneliness. They also show families that your home sees residents as people, not just care tasks.

If a family asks how to get an elderly person into a care home, they often want more than a placement process. They want reassurance. They want to know the home will communicate clearly, involve them properly and support the person through a difficult transition. A successful care home earns trust before admission and keeps earning it after move-in day.

Care Home vs Care Agency: Do You Need the Same Qualifications?

A care home and a care agency both support people with daily care, but they operate in different ways. A care home provides accommodation and care in one residential setting. A care agency usually sends care workers into people’s own homes to provide visiting care, live-in care or assisted living at home.

The qualification rules also differ by business model. If you ask, “what qualifications do you need to open a care agency?”, the answer is similar in principle: you do not always need formal qualifications to own the company, but you must register with CQC if you provide regulated personal care in England. You also need a competent manager, safe recruitment, staff training, policies, insurance and strong oversight.

So, if you are asking, “what qualifications do I need to open a care company?”, start with the type of service you want to provide. The rules, risks, premises, staffing model and costs will change depending on whether you open a residential care home, nursing home or home care agency.

Final Checklist Before You Open a Care Home

What Qualifications Do You Need to Open a Care Home UK

Before you open a care home, check that your business is ready for both care delivery and regulation.

Choose your care model: residential care, nursing care, dementia care or another specialist service.

Research local demand, competitors, fees and staffing availability.

Prepare a realistic business plan and cash-flow forecast.

Secure funding for start-up costs and early running costs.

Choose premises that can meet safety, accessibility and care requirements.

Understand CQC registration before you spend heavily.

Appoint a competent Registered Manager if you will not manage the home yourself.

Prepare policies, procedures, audits and governance systems.

Recruit staff safely and complete DBS checks.

Build training around the Care Certificate, supervision and residents’ needs.

Plan care home activities, family communication and resident experience from day one.

Get expert support before submitting your CQC application.

A care home succeeds when the owner treats compliance, compassion and commercial planning as one system. Get that right, and you build more than a business, you build a home people can trust.

Opening a care home takes more than funding and a suitable building. You need the right CQC registration, policies, staffing structure, training plan, governance systems and business preparation from the start.

Care Sync Experts can support you with CQC registration preparation, care home compliance, policies and procedures, Registered Manager readiness, mock inspections and wider quality assurance. Whether you plan to open a residential care home, nursing home or care agency, we can help you build a safe, compliant and well-led service.

FAQ

How much does homecare cost per hour in the UK?

Homecare in the UK often costs around £25 per hour, but the final price depends on where the person lives, the type of support they need, the visit length and whether they need specialist care.

Short visits, complex care, overnight support and weekend care may cost more. Families should compare local providers and check whether the person qualifies for local authority funding, NHS support or attendance-related benefits.

Is a care home a good business in the UK?

A care home can be a good business in the UK, but only when the owner understands both care quality and financial discipline. Demand remains strong because many older people need residential, dementia or nursing support.

However, staffing costs, regulation, insurance, utilities, maintenance and occupancy levels can quickly affect profit. The best care home owners do not rely on demand alone. They build a safe service, recruit well, manage cash flow and create a home families trust.

How much does a care home worker earn in the UK?

A care home worker in the UK commonly earns around £20,000 to £25,000 a year, depending on experience, location, employer, shift pattern and responsibility level. Senior care workers, team leaders and staff with specialist skills may earn more.

Pay can also change when employers adjust wages in line with the National Living Wage, local recruitment pressure or additional responsibilities such as medication support, night shifts or dementia care.

Who owns the majority of care homes in the UK?

The majority of care homes in the UK sit within the independent sector, which includes private companies, charities and not-for-profit providers. Private operators play a major role, but no single company owns most care homes.

The market remains mixed, with large groups, smaller independent owners, investors, charities and local authority provision all operating in different parts of the sector.

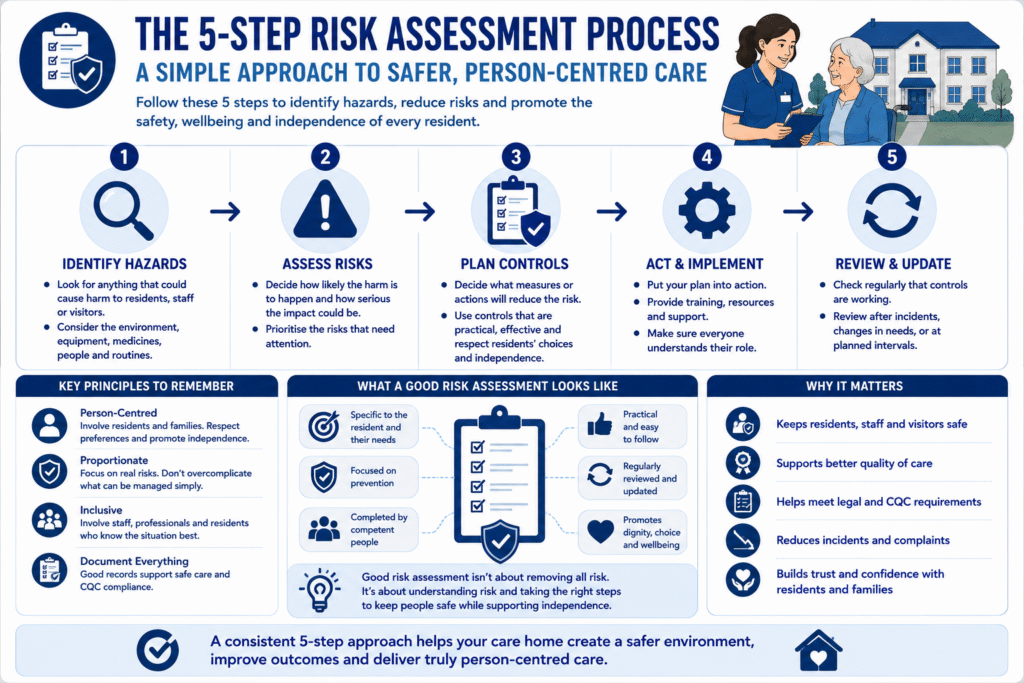

A care home risk assessment identifies anything that could cause harm to residents, staff, or visitors and sets out practical steps to reduce that risk.

It should cover the whole care environment as well as each resident’s individual needs, including falls, moving and handling, medication, nutrition, dementia-related risks, infection control, fire safety, and safeguarding.

Risk assessments matter because they help care teams prevent avoidable harm before an incident happens. They also give staff clear guidance on what to do, what equipment to use, when to ask for support, and when to review someone’s care.

However, the purpose of a risk assessment is not to remove every risk from a resident’s life. Good care homes use risk assessments to protect people while still supporting dignity, independence, routines, and personal choice.

For example, a resident may want to walk to the garden, make a cup of tea, or take part in an activity that carries some risk. Instead of stopping them automatically, the care team should assess the situation, put sensible controls in place, and help the person enjoy everyday life as safely as possible.

A hazard is anything that could cause harm. A risk is the chance that harm could happen and how serious the outcome could be.

For example, a wet bathroom floor is a hazard. The risk is that a resident could slip, fall, and suffer an injury. A hoist used without the right sling is a hazard. The risk is that the resident or carer could fall or get hurt during a transfer.

In care homes, staff should look beyond obvious hazards such as wet floors, loose carpets, poor lighting, or trailing cables. They also need to consider less visible risks, including medication errors, dehydration, pressure damage, infection, choking, confusion, wandering, or unsafe moving and handling.

Good risk assessment in healthcare examples always link the hazard to the person most likely to be affected. A resident with poor balance may face a higher falls risk than another resident. Someone with dementia may need extra support around exits, routines, or unfamiliar environments.

Once staff understand the hazard and the risk, they can put the right controls in place. That may include clearer routines, equipment checks, extra supervision, staff training, or changes to the environment.

Care homes use different types of risk assessment because residents, staff, visitors, and the building itself can face different risks. A strong care home risk assessment brings these areas together so staff can deliver safe care without losing sight of the person’s choices and routine.

The main types of risk assessment in care include:

Individual resident risk assessments for falls, mobility, moving and handling, nutrition, hydration, skin integrity, medication, personal care, dementia, and behaviour that may place someone at risk.

Environmental risk assessments for slips, trips, poor lighting, unsafe equipment, hot water, infection risks, fire safety, and maintenance issues.

Staff and operational risk assessments for staffing levels, lone working, manual handling, medication procedures, training needs, and emergency response.

Safeguarding and security assessments for abuse, neglect, unauthorised access, missing residents, financial risks, and protecting vulnerable adults.

COSHH assessments for cleaning chemicals, disinfectants, laundry products, and other hazardous substances.

Emergency risk assessments for fire, evacuation, power failure, severe weather, outbreaks, or other incidents that could disrupt care.

Personal care risk assessment examples may include checking whether a resident needs help with bathing, dressing, continence care, eating, or using the bathroom safely. In nursing care, staff may also assess pressure ulcer risk, swallowing difficulties, medication needs, and clinical equipment.

The best assessments do not sit in a folder and gather dust. Care teams should use them every day, share updates clearly, and review them whenever a resident’s needs change.

Risk Assessment in Care Homes Examples

The clearest way to understand risk assessment is to look at everyday care situations. Good assessments do not simply identify a problem; they help carers decide what safe, practical support looks like.

Falls risk: A resident becomes unsteady after a medication change. The team checks their footwear, mobility aid, lighting, hydration, medication timing, and level of supervision. They may add regular checks or encourage the resident to use a walking aid, while still supporting them to move around independently.

Moving and handling: A resident needs help transferring from bed to wheelchair. The assessment should record the correct equipment, sling type, number of carers needed, transfer method, and any pain or mobility issues staff need to consider. This protects both the resident and the carers.

Dementia-related risk: A resident enjoys walking outside but sometimes becomes confused about how to return. Rather than stopping them from going out completely, the care team can agree safer controls such as familiar routes, regular check-ins, a personal alarm, family involvement, or staff support at certain times.

Nutrition and hydration risk: A resident loses weight or struggles to swallow safely. Staff may record food textures, drink preferences, mealtime support, allergy information, weight-monitoring plans, and when to seek clinical advice.

These risk assessment in care homes examples show why care providers need more than generic forms. Each plan should reflect the person’s needs, choices, strengths, and daily routine.

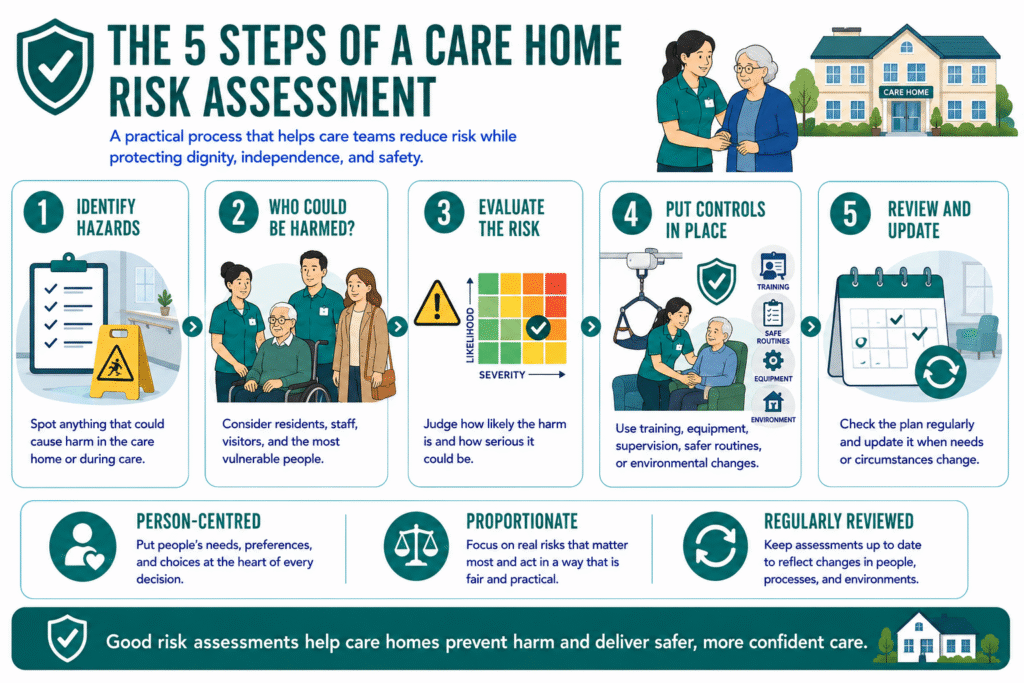

There are five main steps in a risk assessment. Care homes can use this process to spot hazards, protect people, and make sure staff know what action to take.

Identify the hazards Walk through the care home, observe daily routines, speak with staff and residents, and review incident records. Look for anything that could cause harm.

Decide who could be harmed and how Consider residents, staff, visitors, contractors, and the most vulnerable people in the home. A hazard may affect each person differently.

Evaluate the risk and choose controls Decide how likely harm is and how serious it could be. Then put sensible controls in place, such as equipment, training, supervision, safer routines, or environmental changes.

Record findings and put controls into practice Write the assessment clearly. Staff should know what the risk is, what action they need to take, and when they must report concerns.

Review and update the assessment Update the plan when circumstances change. A fall, hospital stay, medication change, infection outbreak, mobility decline, or new equipment may all trigger a review.

So, who should perform a risk assessment? A competent person with the right knowledge should lead it, but good care homes involve carers, managers, residents, families, and relevant health professionals. A risk assessment only works when the people delivering care understand it and follow it consistently.

What Is a Dynamic Risk Assessment?

A dynamic risk assessment happens in the moment when a situation changes and a carer must make a safe decision quickly. Unlike a planned risk assessment, staff do not complete it days or weeks in advance. They use their training, the resident’s care plan, and their professional judgement at the time.

For example, a resident may usually transfer safely from their chair to the bathroom with one carer. One morning, they appear dizzy, weak, or confused. The carer should stop, check what has changed, call for support if needed, and avoid continuing with the usual routine until it is safe.

Dynamic risk assessments also help staff respond to changing situations such as:

A spill on the floor during a busy mealtime

A resident showing signs of distress or agitation

A broken mobility aid or hoist

A sudden deterioration in mobility

A visitor raising a safeguarding concern

A resident refusing care they would normally accept

A good care team does not rush through these moments. Staff pause, assess what has changed, reduce immediate risks, and report the concern so the wider care plan can be reviewed if needed.

Safeguarding, COSHH, and Other Risks Care Homes Must Manage

Care homes need to manage more than falls and moving and handling. They must also protect residents from abuse, neglect, unsafe substances, medication mistakes, infection, and failures in day-to-day care.

Safeguarding in care means protecting people from abuse, neglect, discrimination, avoidable harm, or improper treatment. In practice, this includes listening to concerns, noticing changes in behaviour, recording incidents clearly, and reporting concerns quickly through the right channels.

So, what is safeguarding adults? It is the process of protecting adults who may have care and support needs from harm while respecting their rights, wishes, and involvement in decisions about their lives.

Care homes also need a clear COSHH assessment. COSHH means Control of Substances Hazardous to Health. A COSHH assessment looks at cleaning chemicals, disinfectants, laundry products, and other substances that could harm staff or residents if someone stores, uses, or disposes of them incorrectly.

Other key risks include medication management, infection prevention, fire safety, staffing levels, equipment maintenance, visitor access, and emergency planning. The Care Quality Commission, or CQC, regulates health and adult social care services in England and expects providers to manage these risks safely, consistently, and in a person-centred way.

Why Risk Assessments Matter in Good Care

Common care home risks

Risk assessments protect residents, staff, and visitors, but they should never turn care into a list of restrictions. Good care teams use them to prevent avoidable harm while helping people keep their routines, choices, and independence.

They improve care because they give staff clear guidance. Carers know what support a resident needs, what equipment to use, when to call for help, and what changes they must report. Families also gain confidence when they can see that the home understands the person’s risks and has a plan to manage them.

Risk assessments also support better communication between carers, nurses, managers, families, and health professionals. When everyone works from the same information, the care team can respond earlier to falls, weight loss, confusion, medication changes, pressure damage, or safeguarding concerns.

The Care Certificate also reinforces this approach by covering key areas such as safeguarding, duty of care, dignity, health and safety, fluids and nutrition, infection prevention, and dementia awareness.

The best care home risk assessment does not ask, “How do we remove every risk?” It asks, “How do we help this person live as safely, confidently, and independently as possible?”

Make Risk Management a Strength of Your Care Service

Strong risk assessments protect residents, support carers, and show regulators that your service takes safe, person-centred care seriously.

Care Sync Experts helps care providers build practical systems, strengthen compliance, and create safer services that families and staff can trust.

FAQ

What Are the 5 Risk Assessments?

In a care home, the five most common risk assessment areas are usually: Individual resident risks — such as falls, moving and handling, nutrition, skin integrity, medication, and dementia-related risks. Environmental risks — such as slips, trips, lighting, hot water, fire safety, and unsafe equipment. Staff and operational risks — including staffing levels, lone working, training, and manual handling. Safeguarding and security risks — including abuse, neglect, missing residents, visitor access, and financial harm. Hazardous substance risks — often managed through COSHH assessments for cleaning chemicals, disinfectants, and other substances.

The exact list may vary between homes, but these five areas help providers manage both resident safety and day-to-day care delivery.

What Are 5 Examples of Risk?

Five common examples of risks in a care home include: – A resident falling while walking to the bathroom – A carer injuring their back during a transfer – A medication dose being missed or given incorrectly – A resident choking during a meal – A cleaning chemical being stored where a resident can access it – A risk assessment should identify what could cause the harm, who may be affected, and what controls can reduce the chance or severity of harm.

HSE describes risk assessment as identifying hazards, assessing the risks, controlling them, recording findings, and reviewing the controls.

What Are the 4 Components of Risk Assessment?

A simple risk assessment usually includes four core components: Hazard — what could cause harm Who may be harmed — residents, staff, visitors, or contractors Risk level — how likely the harm is and how serious it could be Control measures — what action will reduce the risk

Many care homes also record who is responsible for each action and when the action must be completed.

HSE templates commonly include existing controls, further actions needed, the responsible person, and deadlines.

What Is a Type 2 Risk Assessment?

“Type 2 risk assessment” is not a standard UK-wide HSE or CQC term. Different providers, local authorities, training companies, and clinical services may use it differently.

In some settings, it can mean a more detailed or specialist assessment completed when a basic assessment identifies a higher level of risk. For example, a resident may need a more detailed moving-and-handling, falls, pressure-care, behavioural, or clinical assessment after an initial concern.

Care homes should avoid relying on the label alone. The important question is whether the assessment clearly identifies the risk, records proportionate controls, names who will act, and sets review triggers.

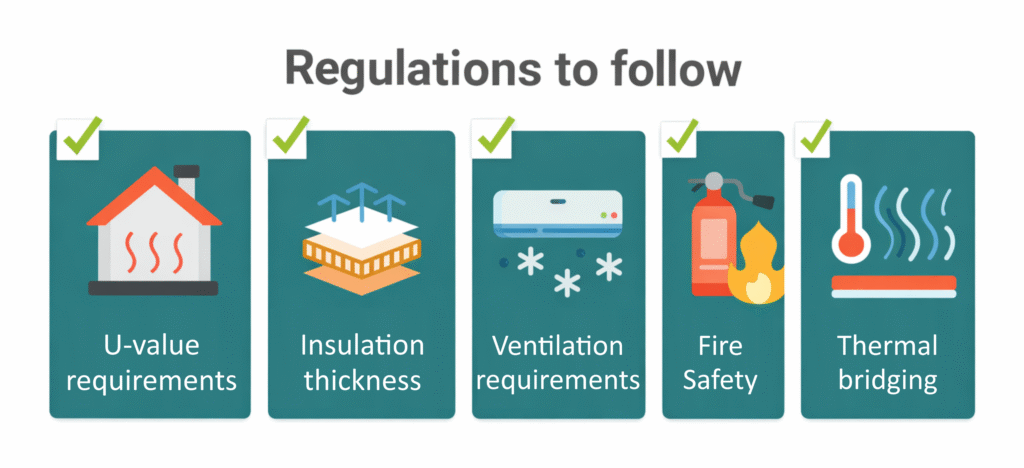

Part L building regulations are UK rules that set minimum energy efficiency standards for buildings, including how they are designed, heated, insulated, and ventilated. In England, these requirements are explained in Approved Document L, which applies to both new buildings and existing properties undergoing renovation or extension.

For care businesses, Part L UK matters whenever you build, convert, extend, or upgrade a property. Whether you are opening a new care home, converting a house into supported living, or improving an office space, you must meet Part L compliance standards before the building can be approved for use.

The latest updates, often referred to as Part L building regulations 2022, came into effect on 15 June 2022 under the Part L building regulations 2021 framework (with later amendments). These changes introduced stricter requirements to reduce energy use and carbon emissions, as part of the UK’s wider push toward net zero.

In simple terms, building regs Part L ensure that:

Buildings lose less heat through walls, roofs, and windows

Heating systems run efficiently and use less energy

Ventilation systems maintain air quality without wasting heat

Developers and contractors provide clear evidence that work meets required standards

For care providers, this is not just a technical requirement. It directly affects:

resident comfort and safety

energy costs and long-term operating expenses

whether a building can legally open or continue operating

Understanding Part L building regulations early helps care businesses avoid delays, reduce costs, and make smarter decisions when planning or upgrading their services.

Care businesses cannot treat Part L building regulations as a “builder’s problem.” These rules directly affect how you open, run, and scale your service.

Energy efficiency is not just about compliance; it shapes your daily operations.

1. It directly impacts your running costs

Care homes and supported living services operate 24/7. Heating, hot water, and ventilation run constantly.

Poor Part L compliance means:

higher energy bills

inefficient heating systems

long-term financial pressure

Meeting building regs Part L standards helps you reduce energy waste and protect your margins.

2. It affects resident comfort and care quality

Warm, well-ventilated environments are essential in care settings.

Strong insulation and proper Part L building Regulations ventilation improve:

indoor temperature stability

air quality for vulnerable residents

infection control and overall wellbeing

If you get this wrong, you don’t just fail compliance, you compromise care standards.

3. It determines whether your project can open on time

If your building fails Part L UK requirements, building control can delay or block approval.

This can lead to:

delayed service launch

lost revenue

costly redesigns or rework

Many care providers only discover issues late, when fixes become expensive and disruptive.

4. It influences funding, inspections, and reputation

Part L building regulations focus on how a building uses energy and how much heat it loses. In England, Approved Document L explains how to meet these requirements in practice.

For care businesses, this section answers a simple question: What exactly do we need to get right before a building is approved?

1. Two main categories: dwellings vs non-dwellings

Part L UK splits buildings into two groups:

Dwellings (Part L1A / L1B)

Homes where people live independently (e.g. some supported living setups)

Non-dwellings (Part L2A / L2B)

Commercial or institutional spaces (e.g. care homes, offices, clinics)

Most care homes fall under Part L building regulations non dwellings, while supported living can fall under either category depending on layout and level of independence.

Getting this classification wrong can lead to incorrect design, failed approval, and delays.

2. Fabric performance (how well the building retains heat)

Building regs Part L require strong insulation across:

walls

roofs

floors

windows and doors

This is measured using U-values (how much heat escapes).

For care providers, this means:

better temperature control for residents

reduced heating demand

lower long-term costs

3. Heating and hot water systems

Part L building regulations push for more efficient, low-carbon systems.

This includes:

modern boilers or heat pumps

lower flow temperatures

smarter controls

For care environments, heating must balance:

energy efficiency

consistent warmth for vulnerable residents

4. Ventilation and air quality

Part L building Regulations ventilation works alongside other rules to ensure buildings stay healthy as they become more airtight.

This includes:

mechanical or natural ventilation systems

controlled airflow

reduced heat loss while maintaining fresh air

This is critical in care settings, where air quality directly affects health outcomes.

5. Energy modelling and calculations

To prove compliance, developers must use:

SAP (for dwellings)

SBEM (for non-dwellings)

These models calculate:

energy use

carbon emissions

overall efficiency

Care businesses don’t need to run these models, but you must ensure your project team does.

6. Evidence and documentation

One of the biggest changes under Part L building regulations 2022 is stricter proof requirements.

You must provide:

design-stage calculations

as-built performance reports

photographic evidence of construction details

Without this, you cannot demonstrate Part L compliance, even if the building is physically correct.

Approved Document L is not just guidance, it defines what your building must achieve to pass.

For care providers, it covers:

how your building is built

how it performs

how you prove it meets the rules

Understanding this early helps you avoid costly mistakes and ensures your project meets Part L building regulations from day one.

Many care providers assume Part L building regulations only apply to large construction projects. In reality, they affect almost every type of property change in the care sector.

If you run or plan to expand a care business, you will likely trigger Part L compliance at some point.

1. Opening a new care home

New-build care homes fall fully under building regs Part L, usually within the Part L building regulations non dwellings category.

You must meet strict requirements for:

insulation and airtightness

heating system efficiency

ventilation design

full energy modelling and evidence

These projects must align with Part L building regulations 2022, which introduced tighter carbon reduction targets.

2. Converting buildings into supported living

Conversions are common in the care sector, but they come with risk.

If you convert:

a house into supported living

a commercial building into a care facility

You must meet Part L building regulations 2021 standards for existing buildings.

This often means:

upgrading insulation

improving heating systems

meeting minimum energy performance levels

Many providers underestimate how much upgrade work is required.

3. Extending an existing care home

Adding new rooms, wings, or facilities triggers Part L UK requirements.

You must ensure:

the new extension meets current energy standards

the connection between old and new parts does not create heat loss issues

Even small extensions can require significant upgrades to meet compliance.

4. Refurbishing or upgrading existing buildings

Even if you are not building new, Part L building regulations still apply when you:

replace windows or doors

upgrade insulation

install a new heating system

carry out major renovation work

These fall under Part L1B or L2B, depending on the building type.

Many care providers trigger compliance without realising it.

5. Setting up or upgrading a domiciliary care office

Office spaces may seem simple, but they still fall under building regs Part L.

If you:

move into a new office

refit an existing one

upgrade heating or ventilation

You may need to meet energy efficiency standards and provide compliance evidence.

6. Special cases and older buildings

Some care providers operate in older or unique properties, such as a grade 2 listed building.

In these cases:

full compliance may not always be possible

adjustments or alternative approaches may apply

However, you should never assume exemption without expert advice under Part L building Regulations exemptions.

Part L Requirements Care Providers Should Understand Before Starting Work

Before you start any project, you need a clear understanding of what Part L building regulations actually require in practice. This is where many care businesses make costly mistakes, by relying entirely on contractors without understanding the basics.

1. Insulation and building fabric

Building regs Part L place strong emphasis on how well your building retains heat.

You must ensure:

walls, roofs, and floors meet minimum insulation standards

windows and doors limit heat loss

gaps and air leakage are controlled

Better insulation means:

more stable indoor temperatures

improved comfort for residents

lower energy bills over time

2. Heating and hot water systems

Part L building regulations 2022 push for more efficient and lower-carbon systems.

Your project must include:

energy-efficient boilers or heat pumps

properly sized systems for the building

modern controls to manage temperature effectively

In care settings, you must balance efficiency with reliability, residents cannot tolerate inconsistent heating.

3. Ventilation and air quality

As buildings become more airtight, ventilation becomes critical.

Part L building Regulations ventilation ensures:

fresh air circulation

removal of moisture and pollutants

reduced risk of overheating

This often includes:

mechanical ventilation systems

heat recovery systems in some cases

Poor ventilation can lead to:

damp and mould

poor air quality

increased health risks for residents

4. Energy modelling and performance targets

To prove Part L compliance, your project team must complete energy calculations.

These include:

SAP for dwellings

SBEM for non-dwellings

These models assess:

carbon emissions

energy consumption

overall building performance

You don’t need to run these models yourself, but you must ensure they are completed correctly.

5. Evidence and documentation (often overlooked)

One of the biggest shifts in Part L UK is the requirement to prove compliance, not just claim it.

You must provide:

design-stage energy reports

as-built performance reports

photographic evidence of key construction stages

Photos must clearly show:

insulation installation

junction details where heat loss can occur

key building elements before they are covered

Without proper evidence, your building may fail approval, even if the work is correct.

6. Responsibility and coordination

Many care providers assume the builder handles everything.

How Part L Links with Other Rules Care Businesses May Hear About

Part L Building Regulations Compliance

When you plan a care project, you will hear multiple regulations, not just Part L building regulations. This can feel overwhelming, especially if you are not from a construction background.

The key is to understand what each rule covers and how they connect.

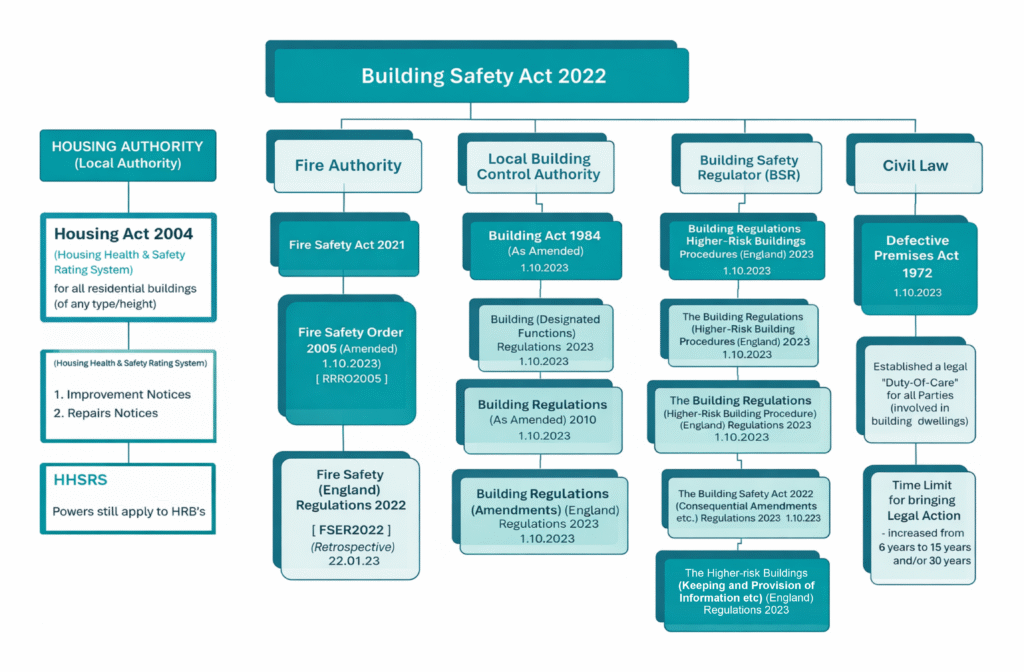

1. Part L vs the Building Safety Act

Part L focuses on energy efficiency. The Building Safety Act and building safety act 2022 focus on safety, accountability, and documentation.

For care providers, this means:

Part L ensures your building performs efficiently

The Building Safety Act ensures your building is safe and properly documented

Both require strong record-keeping and evidence, especially for larger or higher-risk buildings.

2. Part L vs Part M (accessibility)

You will often hear about part m building regulations or approved document m during care projects.

Part L = energy efficiency

Part M = accessibility and usability

In care settings, building regs part m is critical because it covers:

wheelchair access

bathroom layouts

safe movement within the building

You must meet both standards at the same time; one does not replace the other.

3. Part L vs fire safety rules (Part B)

Fire safety falls under:

approved doc b

building regs part b

These rules focus on:

fire detection systems

escape routes

compartmentation

While Part L UK focuses on insulation and airtightness, you must ensure these do not conflict with fire safety design.

4. Other related regulations you may encounter

Depending on your project, you may also hear about:

approved document k (safety around stairs, ramps, and movement)

general building regulations covering structure and ventilation

These do not replace Part L building regulations, but they run alongside them.

5. Why this matters for care providers

Care projects rarely deal with one regulation in isolation.

If you:

build a new care home

convert a property

extend an existing facility

You will need to meet multiple standards at once.

The biggest risk is:

focusing on energy efficiency

while overlooking access, safety, or usability

Part L building regulations form just one part of a wider compliance framework.

For care providers:

Part L = energy performance

Part M = accessibility

Part B = fire safety

Building Safety Act = accountability and safety systems

Understanding how they work together helps you:

avoid design conflicts

prevent costly redesigns

ensure your building meets all approval requirements the first time

Are there any exemptions or special cases under Part L?

Changing Part L Thermal Standards

Many care providers ask whether Part L building regulations always apply in full. The answer is: not always, but exemptions are limited and highly controlled.

You should never assume you qualify for Part L building Regulations exemptions without proper advice.

1. Existing and older buildings

When you upgrade an existing property, Part L allows some flexibility.

For example:

you may not need to upgrade every element to new-build standards

improvements must be “reasonable and practical”

However, you still need to:

improve energy performance where possible

avoid making the building worse

Even partial refurbishment can still trigger Part L compliance requirements.

2. Listed and heritage buildings

Care providers sometimes operate in older or historic properties, such as a grade 2 listed building.

In these cases:

strict upgrades (like replacing windows or external insulation) may not be allowed

heritage protection can limit what changes you can make

However:

you must still improve energy efficiency where it does not damage the building’s character

This often requires:

specialist advice

tailored solutions

3. Technical and practical limitations

Some buildings cannot meet full modern standards due to:

structural limitations

space constraints

compatibility with existing systems

In these situations:

alternative measures may be accepted

compliance focuses on “reasonable improvement” rather than perfection

4. What does NOT count as an exemption

Care providers often misunderstand this.

You are not exempt just because:

the building is old

the project is small

you are only making minor changes

you are leasing the property

If your work affects energy performance, building regs Part L will likely apply.

5. Why exemptions still require documentation

Even when flexibility applies, you must:

justify your approach

document decisions

show why full compliance was not possible

Building control will still expect:

clear reasoning

supporting evidence

Part L building regulations rarely offer full exemptions.

In most cases:

you must comply fully

or improve performance as far as reasonably possible

Care providers who assume they are exempt often face:

delays

redesign costs

compliance issues during approval

The safest approach is simple:

Always check early, plan properly, and treat Part L compliance as part of your core project strategy.

Many care providers run into problems with Part L building regulations, not because the rules are unclear, but because they get involved too late or rely on the wrong assumptions.

Avoiding these mistakes can save you time, money, and project delays.

1. Treating Part L as the builder’s responsibility

Many providers assume the contractor will “handle compliance.”

In reality:

you own the project

you remain responsible for Part L compliance

poor coordination can still lead to failure

You need visibility from design to completion.

2. Signing a lease or buying a property without checking requirements

This is one of the most expensive mistakes.

Care providers often:

secure a building first

check building regs Part L later

This can lead to:

unexpected upgrade costs

delays in opening

redesign of heating, insulation, or ventilation systems

Always assess Part L building regulations before committing to a property.

3. Assuming only new builds are affected

Many providers think Part L UK only applies to new construction.

In reality, it also applies when you:

refurbish

extend

replace key building elements

Even simple upgrades can trigger compliance requirements.

4. Ignoring ventilation when improving insulation

Improving insulation without considering Part L building Regulations ventilation creates serious problems.

This can lead to:

poor air quality

damp and mould

overheating

Energy efficiency must always balance with ventilation.

5. Underestimating documentation and evidence

Some providers focus on the physical build but forget about proof.

Under Part L building regulations 2022, you must provide:

energy calculations

as-built reports

photographic evidence

Without this, your project may fail, even if everything is installed correctly.

6. Leaving compliance too late in the project

If you only think about Part L during construction, you are already at risk.

Late changes can mean:

redesigning systems

replacing materials

increased costs

The best projects consider compliance at the design stage.

7. Not involving the right professionals early

Successful projects require:

energy assessors

consultants

experienced contractors

If you delay bringing them in:

mistakes go unnoticed

compliance gaps increase

Bottom line

Most Part L building regulations issues come down to timing and awareness.

Care providers who:

plan early

ask the right questions

stay involved

Avoid delays, reduce costs, and achieve smooth approvals.

Those who don’t often face:

rework

compliance failures

delayed service launches

Final takeaway for care providers

Part L building regulations are not just a technical requirement, they directly shape how your care business operates, grows, and delivers safe environments.

If you plan to:

open a new service

convert a property

extend or refurbish a building

You must consider Part L compliance from the very beginning.

Care providers who approach Part L UK correctly:

control energy costs

create comfortable, healthy environments for residents

avoid delays during approval

protect their investment

Those who ignore it often face:

unexpected upgrade costs

failed inspections

delayed openings

The simple rule to follow

Treat building regs Part L as a business priority, not just a construction detail.

If you:

check requirements early

work with the right professionals

plan for both performance and evidence

You will meet compliance smoothly and avoid costly mistakes.

One final perspective

Energy efficiency is no longer optional. It sits at the centre of modern care delivery.

Understanding Part L building regulations helps you:

build smarter

operate more efficiently

deliver better care environments

And in a sector where comfort, safety, and sustainability matter every day…

That is a competitive advantage.

Need Expert Support Navigating Building Compliance and Care Facility Requirements?

Care Sync Experts supports care providers, care home operators, and healthcare organisations across the UK with clear, practical guidance on regulatory compliance, property requirements, and operational readiness.

From helping you understand Part L building regulations, energy efficiency standards, and building compliance requirements, to guiding you through property conversions, refurbishments, and service setup, our specialists turn complex regulations into simple, actionable steps.

Whether you are opening a new care home, converting a property into supported living, upgrading your facilities, or ensuring full Part L compliance alongside CQC expectations, our team delivers tailored support designed for real-world care environments.

Plan smarter, avoid costly mistakes, and ensure your care premises meet all regulatory standards from day one.

Contact Care Sync Experts today to get expert support on building compliance, care facility setup, and navigating UK care regulations with confidence.

FAQ

Is Part L law in the UK?

Yes. Part L building regulations form part of the Building Regulations in England and are legally enforceable. While Approved Document L provides guidance on how to meet the requirements, the underlying regulation itself is law.

If a care provider or developer fails to meet Part L compliance, building control can: – refuse approval – require corrective work – issue fines or enforcement action In simple terms: you must comply with Part L to legally complete and use a building.

What are carbon emission targets in Part L?

Part L building regulations 2022 introduced stricter carbon reduction targets as part of the UK’s journey toward net zero.

For new buildings: – new homes must reduce carbon emissions by around 30% compared to previous standards – future standards aim for 75–80% reductions by 2025

For care providers, this means: – more efficient heating systems – better insulation – lower overall energy use

These targets directly influence design, costs, and long-term energy performance.

What is the 10 year rule for listed buildings?

The “10-year rule” is often misunderstood. It does not automatically exempt buildings from regulation, including Part L building regulations.

In planning terms, it generally refers to situations where: – unauthorised work may become lawful after 10 years if no enforcement action is taken

However, for buildings such as a grade 2 listed building: – separate listed building consent rules still apply – energy upgrades must balance compliance with heritage protection

Care providers should always seek professional advice; never assume older or listed buildings are exempt from compliance requirements.

What are the 7 stages of construction?

Understanding the construction process helps care providers manage Part L compliance effectively. The typical stages are: – Planning and feasibility – Design and approvals – Procurement and contractor selection – Site preparation – Construction – Inspection and compliance checks – Completion and handover

Part L building regulations apply across multiple stages, especially: – design (energy modelling and specifications) – construction (installation quality) – completion (evidence and certification)

Getting involved early in these stages helps care businesses avoid delays and ensure smooth approval.

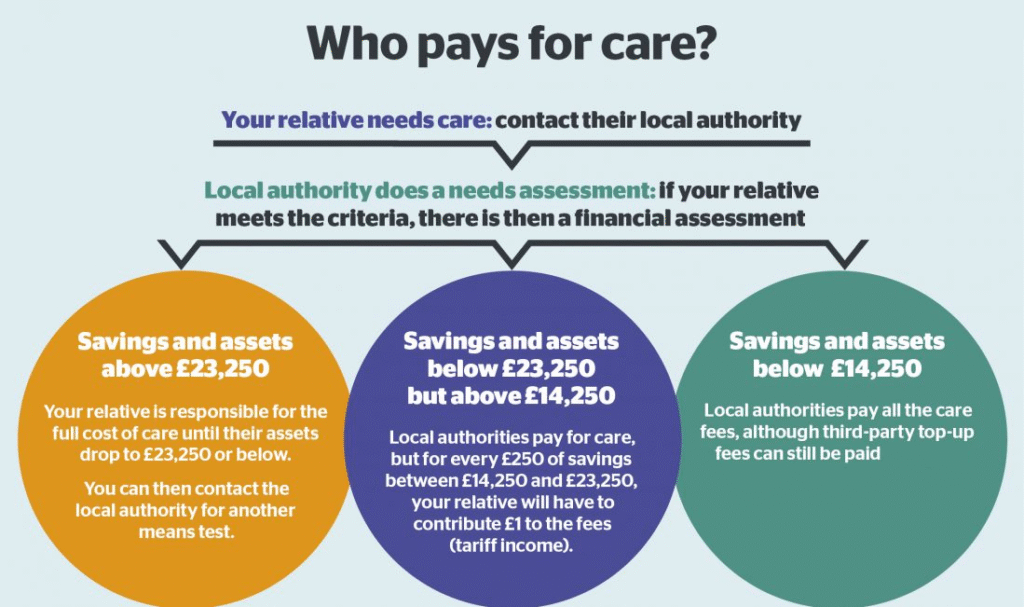

If you’re do dementia sufferers have to pay care home fees, the answer is yes. Many dementia sufferers do have to pay care home fees in the UK, because dementia care is usually classified as social care rather than medical care. This means the cost of a dementia care home is typically assessed through a financial (means) test carried out by the local authority.

If a person’s savings, income, or assets exceed certain thresholds, they usually have to pay for their own care home fees, either fully or partly. In England, for example, people with more than £23,250 in assets are generally expected to fund their own care.

However, some people with dementia may receive financial support or fully funded care, depending on their circumstances.

Self-funding is common. Many families pay privately for dementia care homes when savings or property exceed the means-test threshold.

Local authorities may contribute. If assets fall below the upper threshold, the council may help with care home fees.

NHS Continuing Healthcare (CHC) may cover the full cost of care if the person’s needs are primarily medical rather than social.

NHS-Funded Nursing Care (FNC) may pay a weekly contribution if the person lives in a nursing home and needs care from registered nurses.

Because of these rules, dementia care home costs in the UK vary widely. Some families pay the full price of long-term care, while others receive partial or full funding depending on their financial situation and health needs.

Understanding how the system works is the first step toward finding help with care home fees for dementia patients and planning the right level of support.

Why dementia care home costs in the UK are often high

Many families feel shocked when they first see dementia care home costs in the UK. Unlike standard residential care, dementia care requires specialist support, higher staffing levels, and a secure environment, all of which increase the overall cost of care homes.

People living with dementia often need help throughout the day and night. Care teams support residents with memory loss, confusion, mobility problems, and changes in behaviour. As the condition progresses, care homes may provide enhanced dementia care, which includes:

24-hour supervision and support

Staff trained specifically in dementia care

Secure layouts to prevent wandering

Structured routines and therapeutic activities

Specialist nursing care for complex health needs

These additional services make dementia care homes more resource-intensive than many other forms of residential care.

Location also plays a major role in the cost of an old people’s home. Care homes in cities or areas with higher staffing costs often charge significantly more than homes in rural regions. Facilities that provide specialist dementia units, private rooms, or advanced medical care may also charge higher fees.

For caregivers searching online for dementia care homes near me or a care home for dementia near me, the price can vary dramatically depending on the level of support required. Families often discover that dementia care involves not just accommodation but round-the-clock professional care, which is why the price of long-term care can feel overwhelming at first.

Understanding these factors helps families prepare for the financial side of dementia care and explore available funding options before making long-term decisions.

The cost of care homes for dementia in the UK varies widely depending on the type of care, the location, and the level of support required. However, most families can expect dementia care to cost more than standard residential care, because specialist support and supervision are often needed.

On average, weekly dementia care home costs in the UK are approximately:

Residential dementia care: around £1,200 – £1,500 per week

Nursing dementia care: around £1,400 – £1,700 per week

These figures represent the typical price of long-term care, but the final cost depends on several factors.

What affects the cost of care homes?

Several factors influence how much families pay for care home fees, including:

Location: Care homes in London and major cities often charge more than those in smaller towns.

Level of care required: Residents who need specialist nursing or behavioural support may face higher costs.

Facilities and services: Private rooms, specialist dementia units, and enhanced dementia care programs can increase fees.

Availability of care homes: In some areas, limited supply means higher prices.

For families searching online for “dementia care homes near me”, prices can vary significantly even within the same region. Some homes focus on standard residential support, while others offer specialist dementia care homes with trained staff and secure environments designed specifically for memory conditions.

Because of these variations, the cost of an old people’s home or dementia care home can differ greatly from one provider to another. This is why many families first research local options before deciding whether to fund care privately or apply for financial support.

Who pays dementia care home fees in the UK?

do dementia sufferers have to pay care home fees 2026

In most cases, who pays care home fees depends on a financial (means) assessment carried out by the local authority. This assessment looks at the person’s income, savings, and assets to determine whether they must pay for their care themselves or qualify for financial support.

Many people with dementia end up paying some or all of their care home fees, particularly if they have savings or property above the government thresholds.

The financial assessment explained

Before funding any care placement, the local council will usually complete two assessments:

Needs assessment – Determines what type of care the person requires (home care, residential care, or nursing care).

Financial assessment – Calculates how much the person should contribute toward the cost of care homes.

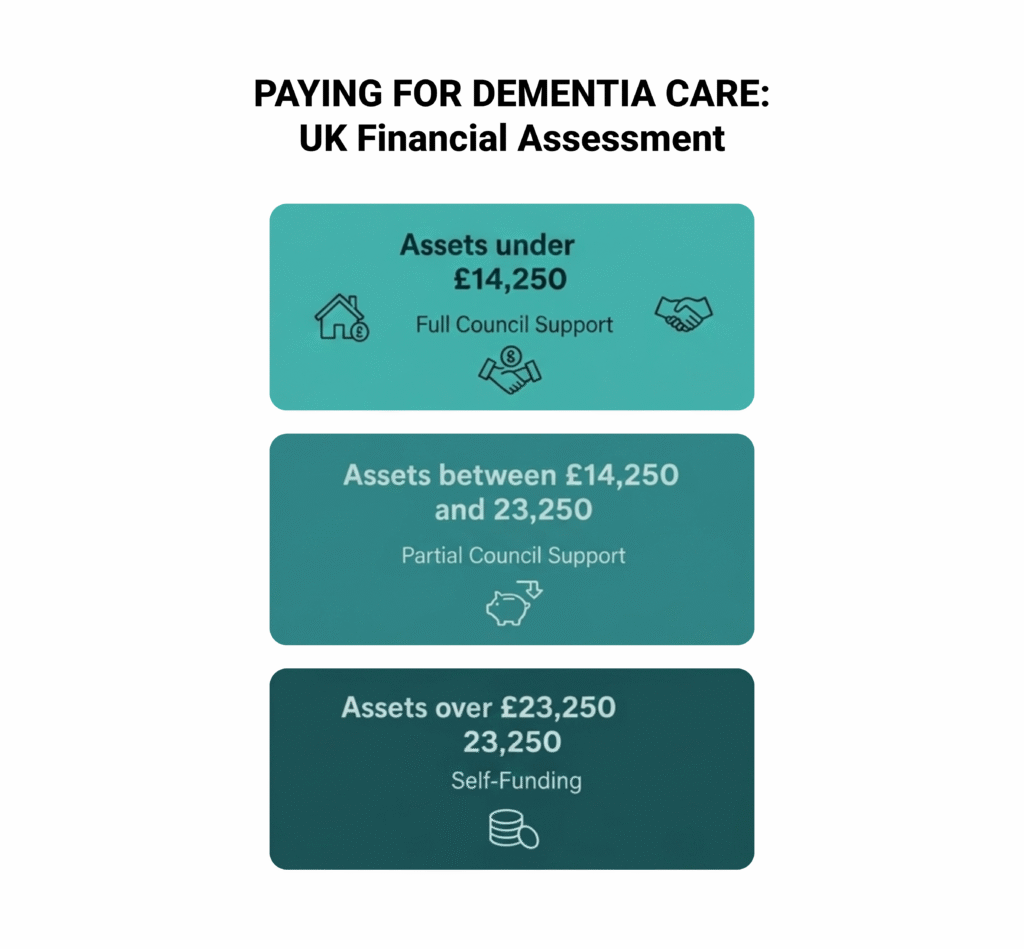

In England, the main capital limits currently work as follows:

Over £23,250 in assets: The person normally pays the full dementia care home costs UK privately (self-funding).

Between £14,250 and £23,250: The person contributes toward care costs, and the local authority may help pay the rest.

Below £14,250: The local authority usually covers most care costs, although income such as pensions may still contribute.

Assets considered in the financial assessment can include:

Savings and investments

Property (in some cases)

Pensions or regular income

However, the value of a home may not always be included in the assessment. For example, if a spouse or dependent relative still lives in the property, the council may disregard its value.

Local authority funding for care

If someone qualifies financially and meets eligibility criteria, the council may provide local authority funding for care in your own home or help cover the cost of a residential placement.

Families often start researching how to get help with care home fees once they understand the outcome of the financial assessment. The council may either arrange the placement directly or provide a personal budget to support the person’s care needs.

Understanding how the financial assessment works can help families plan ahead and explore the options available for help with care home fees for dementia patients.

Is there free care home funding for dementia patients?

Many families ask whether there is free care home funding for dementia patients in the UK. In most situations, dementia care is not automatically free, because the system treats it primarily as social care rather than healthcare. However, some people with dementia may qualify for funding that covers part or all of their care home fees.

Two NHS funding routes can help reduce dementia care home costs in the UK.

NHS Continuing Healthcare (CHC)

NHS Continuing Healthcare is a package of care fully funded by the NHS. If someone qualifies, the NHS pays the full cost of care, including accommodation and nursing support in a care home.

Eligibility does not depend on savings or assets. Instead, assessors decide whether the person has a “primary health need.” This means their care needs mainly involve medical supervision rather than personal support.

Some people with advanced dementia qualify for CHC when they experience complex needs such as:

Severe cognitive impairment

High levels of behavioural distress

Complex mobility problems

Significant medical supervision needs

Although families sometimes assume dementia automatically qualifies for CHC, this is not always the case. Each person must go through a detailed assessment conducted by healthcare professionals.

For those who meet the criteria, CHC effectively provides free care for dementia patients in the UK, because the NHS covers the full cost of care.

NHS-Funded Nursing Care (FNC)

If someone lives in a nursing home but does not qualify for CHC, they may still receive NHS-Funded Nursing Care.

Under this scheme, the NHS pays a weekly contribution toward the nursing element of care. The payment goes directly to the care home and helps reduce the overall care home fees families must pay.

FNC does not cover accommodation or personal care costs, but it can still provide meaningful financial support for people living in specialist dementia care homes that require registered nursing staff.

Understanding these funding options helps families determine whether they can access help with care home fees for dementia patients, particularly when dementia progresses, and care needs become more complex.

Are next of kin responsible for care home fees?

Pay for Dementia Care-Uk Financial Assessment

Many families worry that they might personally inherit the care home fees of a loved one with dementia. In most cases, next of kin are not legally responsible for paying care home fees.

The person receiving care usually remains responsible for their own dementia care home costs in the UK. Local authorities or the NHS may contribute depending on the outcome of the needs and financial assessments, but family members do not automatically become liable for the bill.

However, there are a few situations where a relative may agree to pay part of the cost.

When families may contribute to care home fees

A family member may become financially involved if they choose to:

Sign a contract with the care home agreeing to pay part of the fees

Provide a third-party top-up payment if they select a more expensive home than the local authority normally funds

Manage finances on behalf of the person through Lasting Power of Attorney

For example, if a council agrees to fund care up to a certain amount but the family prefers a more expensive care home for dementia near me, they may choose to pay the difference as a top-up.

What families should understand

In most cases:

Next of kin are not automatically responsible for care home fees.

The financial assessment focuses on the assets and income of the person receiving care.

Families should carefully review any agreements before signing documents with a care home.

Understanding this distinction can reduce anxiety for caregivers who already face emotional and practical challenges when supporting someone living with dementia.

Not every person with dementia needs to move into a care home immediately. Many families first explore care at home, especially in the early or moderate stages of dementia. Understanding home care services cost can help caregivers decide whether staying at home is a practical alternative.

How much does home care cost per hour in the UK?

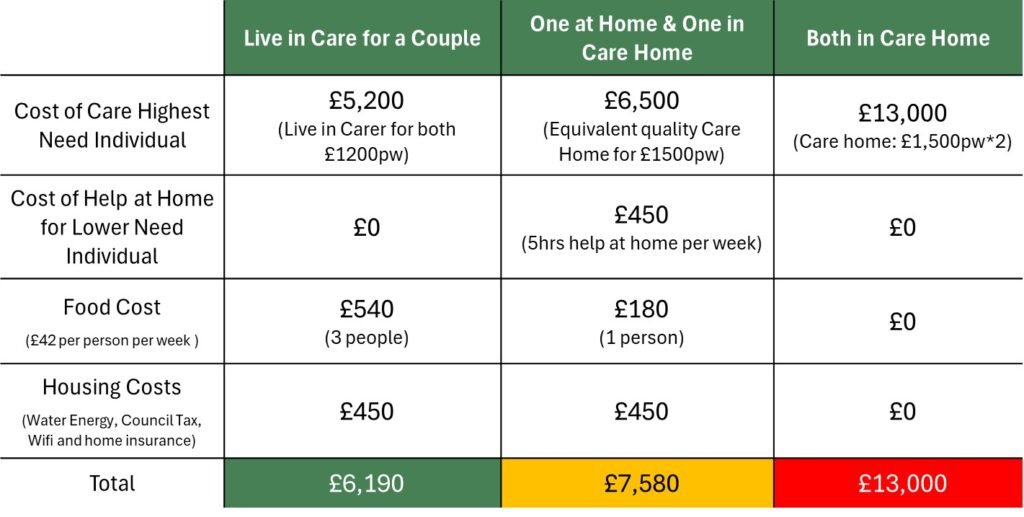

The cost of home care services depends on the level of support required and the region where you live. On average:

Home care services: around £20–£35 per hour

Live-in carer cost: roughly £900–£1,600 per week depending on care needs

Private nursing care: higher costs if medical support is required

Families often search questions such as “how much does home care cost per hour UK” or “how much does a home nurse cost” when deciding whether home care might be more affordable than residential care.

When home care may work better

Home care can be a suitable option when a person with dementia:

Can still live safely in familiar surroundings

Needs help with daily tasks such as washing, dressing, or medication

Benefits from routine and familiar environments

In some situations, the local authority may also provide local authority funding for care in your own home after completing a needs and financial assessment.

When residential care becomes necessary

As dementia progresses, some people eventually require 24-hour supervision or specialist dementia support. At that stage, families may start exploring dementia care homes near me or a care home for dementia near me that offers structured care and specialist staff.

Understanding the differences between home care and residential care helps families make informed decisions about the cost of care homes, the price of long-term care, and the level of support their loved one truly needs.

How to get help with care home fees for dementia patients

Many families feel overwhelmed when they first learn about dementia care home costs in the UK. The good news is that several funding routes may help reduce or cover care home fees, depending on the person’s financial situation and care needs.

If you are wondering how to get help with care home fees, the process usually begins with two important assessments arranged through your local authority.

1. Request a care needs assessment

Start by asking your local council for a care needs assessment. A trained professional will evaluate the person’s condition and decide what level of support they require. This assessment determines whether the person needs:

Home care support

Specialist dementia care

A residential or nursing care home

The results help the council decide what type of support they can provide.

2. Complete a financial assessment

If the person needs residential care, the council will then carry out a financial (means) assessment to determine who pays for the care.

The assessment considers:

Savings and investments

Income, such as pensions

Property ownership

Other financial assets

Depending on the results, the local authority may contribute toward the cost of care homes, or the person may need to self-fund their care.

3. Ask about NHS funding options

Families should also ask for an assessment for NHS Continuing Healthcare (CHC) if the person has complex health needs. If approved, CHC can cover the full cost of care, including accommodation in a care home.

If CHC is not granted but the person lives in a nursing home, they may still qualify for NHS-Funded Nursing Care, which contributes toward the nursing portion of care home fees.

4. Check benefits and financial support

Some people with dementia may qualify for additional financial help, including:

Attendance Allowance

Personal Independence Payment (PIP) for people under pension age

Pension Credit

Council tax reductions for severe mental impairment

These benefits can help cover daily expenses and reduce the overall price of long-term care.

5. Explore deferred payment schemes

If the person owns a home but does not want to sell it immediately, the local authority may offer a deferred payment agreement. This allows care fees to be paid later, usually when the property is eventually sold.

Understanding these steps helps families access help with care home fees for dementia patients and navigate the financial side of care with more confidence.

Tips for caring parent or loved ones with dementia at home

When dementia progresses, and care needs increase, many families begin searching online for dementia care homes near me or a care home for dementia near me. Choosing the right home can feel overwhelming, but taking a structured approach can make the process easier.

Start with local authority directories

Your local council usually keeps a list of approved providers and can help you identify government funded care homes near me that meet required standards. If the local authority funds part of the placement, they may suggest care homes that work within their funding arrangements.

However, families can still explore other dementia care homes if they prefer a different location or service. In some cases, this may involve paying a top-up fee if the chosen home costs more than the council normally covers.

Check care quality ratings

Before choosing a care home, review the inspection ratings from the relevant regulator:

Inspection reports can reveal important details about safety, staffing levels, and the quality of dementia care provided.

Visit care homes in person

Whenever possible, visit several dementia care homes near you before making a decision. Pay attention to:

Staff interactions with residents

Safety and cleanliness

Activities designed for people with dementia

Secure layouts for residents who may wander

Many homes offer specialist enhanced dementia care, including memory-friendly environments, trained staff, and structured daily routines.

Consider care needs and future progression

Dementia is a progressive condition, so it is important to choose a home that can support increasing care needs over time. Some homes provide both residential and nursing care, which allows residents to remain in the same environment as their condition changes.

Taking time to research and visit care homes for dementia near you helps families make confident decisions and ensures their loved one receives the level of care and support they truly need.

Key facts about dementia care home fees

If you are supporting someone with dementia, understanding how care home fees work can make the financial side of care much less confusing. The most important points families should remember include the following:

Many people with dementia pay for their own care. Dementia care is usually treated as social care, which means funding depends on a financial assessment rather than being automatically covered by the NHS.

Local authorities may help with the cost of care homes. If a person’s savings and assets fall below the capital thresholds, the council may contribute toward their care.

NHS funding is sometimes available. People with complex medical needs may qualify for NHS Continuing Healthcare, which can cover the full cost of care.

NHS-Funded Nursing Care may reduce costs. If someone lives in a nursing home but does not qualify for full NHS funding, the NHS may contribute a weekly amount toward the nursing element of care.

Home care can be an alternative in earlier stages. Some families explore options such as live-in carers or hourly support before moving to residential care.

Understanding these key facts can help families plan ahead, explore help with care home fees for dementia patients, and make informed decisions about the best care options for their loved ones.

New rules for care home payments in the UK (2026 update)

Families often ask whether the government has introduced new rules for care home payments that could reduce the price of long-term care. The UK government has discussed several reforms to the social care system in recent years, but the way care home fees work largely remains the same for most families.

The proposed care cost cap

A major reform previously planned was a cap on lifetime care costs, which would have limited how much individuals pay for personal care over their lifetime. The proposed cap was set at £86,000.

However, the government later delayed these reforms, meaning the current funding system still relies mainly on the means-tested financial assessment used by local authorities.

What this means for families today

For now, most people entering a care home will still follow the existing system:

People with assets above the upper capital limit usually self-fund their care.

Those with fewer assets may receive local authority support.

NHS funding remains available through Continuing Healthcare or NHS-Funded Nursing Care for those who qualify.

Because policy changes can happen over time, families should always check the latest government guidance or speak with their local authority before making long-term financial decisions about care.

Understanding these rules can help caregivers plan ahead and better prepare for the cost of care homes or specialist dementia care homes in the future.

Conclusion

Understanding whether dementia sufferers have to pay care home fees can feel confusing at first, especially when families face emotional and financial pressure at the same time. In the UK, dementia care is usually treated as social care, which means many people pay for some or all of their care home fees depending on their financial situation.

The amount someone pays depends on several factors, including their savings, property, and the outcome of a local authority financial assessment. Some people qualify for support from the council, while others may receive NHS funding through Continuing Healthcare or NHS-Funded Nursing Care if their needs are primarily medical.

Because dementia care home costs in the UK can be significant, families benefit from understanding the funding process early. Requesting a care needs assessment, exploring financial support options, and reviewing care home choices carefully can make the transition into long-term care much easier to manage.

Planning ahead also helps caregivers make informed decisions about the cost of care homes, home care alternatives, and the best level of support for their loved one.

If you are supporting someone with dementia and need guidance navigating care home fees, funding assessments, or NHS Continuing Healthcare applications, Care Sync Experts can help.

We work with families and care professionals to review funding eligibility, explain the assessment process clearly, and help present care needs accurately so you can access the financial support available for dementia care and avoid the common mistakes that delay or reduce funding.

FAQ

Do dementia patients do better at home or in a nursing home?

It depends on the stage of dementia and the level of support the person needs. In the early stages, many people with dementia do well at home because familiar surroundings can reduce confusion and anxiety. Family support, home care services, and structured routines often help maintain independence for longer.

However, as dementia progresses, some individuals require 24-hour supervision, specialist dementia care, or nursing support. At this stage, a dementia care home or specialist nursing home may provide a safer environment with trained staff, structured activities, and secure facilities designed to support memory-related conditions. The best option depends on the person’s safety, medical needs, and the level of support available at home.

How fast can dementia progress?

Dementia progresses at different speeds depending on the type of dementia, the person’s age, and their overall health. Some people experience slow progression over many years, while others may decline more quickly.

On average, many people live between 4 and 10 years after diagnosis, although some individuals live much longer. Certain forms of dementia, such as vascular dementia, may progress in noticeable steps, while Alzheimer’s disease typically causes a gradual decline. Regular medical reviews, supportive care, and early intervention can sometimes help slow the impact of symptoms.

What are the signs dementia is getting worse?

As dementia progresses, symptoms usually become more noticeable and begin to affect daily life more significantly. Families often notice changes in memory, behaviour, and independence.

Common signs that dementia may be worsening include: – Increasing memory loss and confusion – Difficulty recognising familiar people or places – Problems with communication or finding words – Changes in behaviour or mood, such as agitation or anxiety – Difficulty managing everyday tasks like dressing, cooking, or taking medication – Greater need for supervision and personal care

When these signs appear, families may start considering additional support such as home care services or specialist dementia care.

What are four common behaviours that people with dementia often exhibit?

People living with dementia often experience changes in behaviour because the condition affects memory, reasoning, and emotional regulation. While symptoms vary from person to person, several behaviours commonly occur.

Four common behaviours seen in people with dementia include: Memory loss – forgetting recent events, appointments, or conversations Confusion or disorientation – becoming lost in familiar places or forgetting the date or time Mood or personality changes – increased anxiety, irritability, or withdrawal Repetitive actions or questions – asking the same question repeatedly or repeating activities

These behaviours usually develop gradually as the condition progresses. Understanding them can help caregivers respond with patience and choose the right level of support for the person living with dementia.

Are there new rules for care home payments introduced in 2026?

Care home fees in the UK continue to follow the existing means-tested system, with no lifetime cap on care costs and no automatic reduction in care home costs. Families must still plan based on income, savings, and property, as local authorities assess care home payments using the same framework that applied in previous years.

This guide explains what actually applies in 2026, clears up common myths, and shows how care home fees work in practice so families can make informed decisions.

Why So Many Families Expect New Care Home Rules in 2026

How to Get Referrals for Supported Living Without a Property | 2025 Framework Guide

Confusion around care home payments in 2026 did not come from nowhere. For several years, the government discussed major reforms to how care is funded in England. These plans received widespread media coverage and created the expectation that care home costs would become more predictable or capped.

Earlier proposals promised changes such as a lifetime cap on care costs and higher thresholds before people would need to pay for their own care. Many families assumed these reforms would eventually take effect, especially after repeated delays.

However, those proposals never became law. By 2026, the government had abandoned them entirely. Despite that, outdated information continues to circulate online, leading many people to believe the care home fees UK system has changed when it has not.

This mismatch between expectation and reality causes real problems. Families delay planning, underestimate care home costs, or assume protections exist that simply do not apply. Understanding what didn’t change in 2026 matters just as much as what did.

Were New Care Home Payment Rules Introduced in 2026?

No. No new care home payment rules have been introduced in 2026 (As of the time of publishing this content). Despite years of public discussion about reform, the legal framework for paying care home fees in the UK, particularly in England, remains the same.

Local authorities still use a means-tested system to decide who pays for care and how much they contribute. There is no lifetime cap on care costs, and there are no new protections that automatically reduce care home fees in 2026. Families should not assume that care home costs are capped, frozen, or subsidised simply because reforms were previously announced.

This point matters because many people plan care based on headlines rather than law. In practice, councils continue to assess:

A person’s income, such as pensions and benefits

Their capital, including savings and, in some cases, property

Whether they qualify for full, partial, or no local authority support

The absence of new rules also means responsibility has not shifted. Individuals with assets above the upper threshold still self-fund their care, while those below may receive council support. Nothing in 2026 changes how that assessment works.