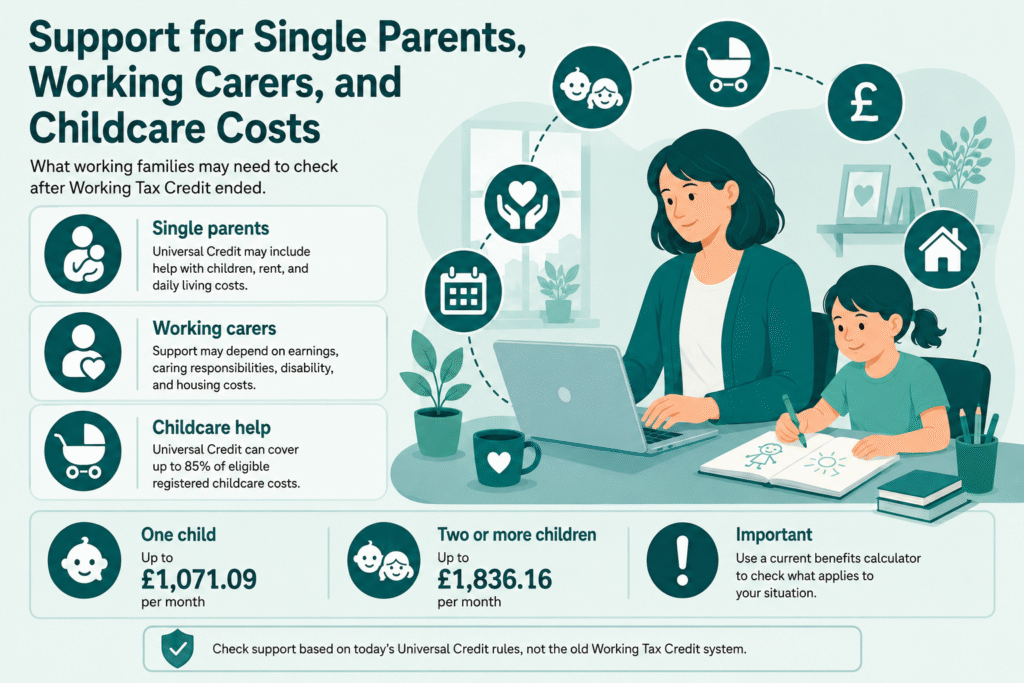

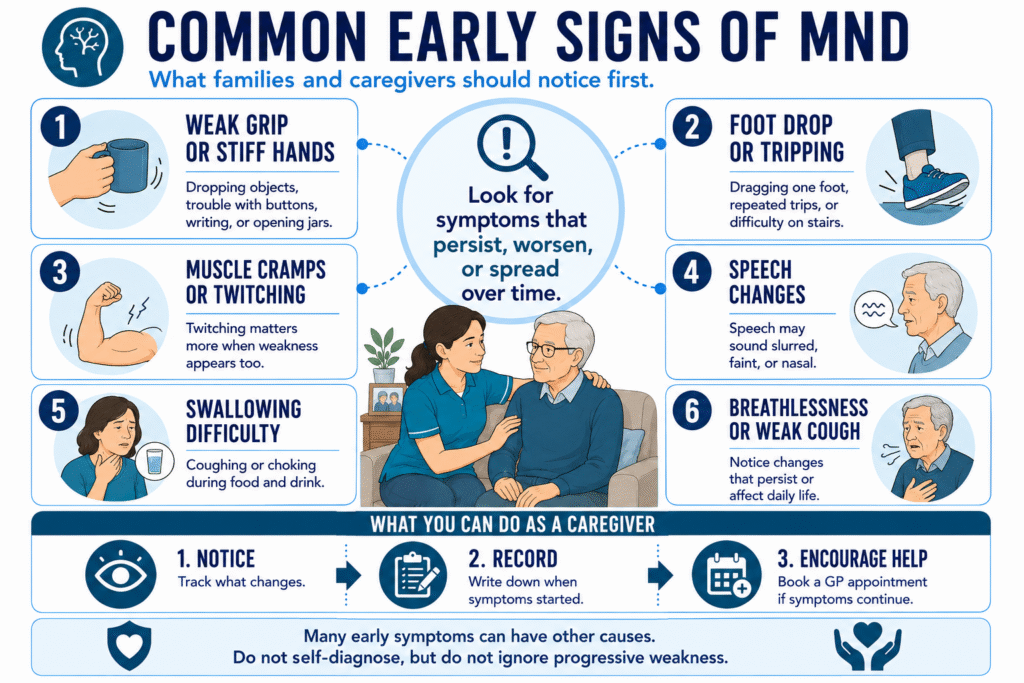

An early sign of MND often starts with muscle weakness that slowly gets worse. A person may develop a weak grip, drop objects more often, drag one foot, trip repeatedly, struggle with stairs, speak less clearly, or cough when eating and drinking.

Some people also notice muscle cramps or twitching, but twitching alone does not always point to MND. Stress, tiredness, trapped nerves, injuries, vitamin deficiencies, and other health problems can cause similar symptoms.

Families and caregivers should look for a pattern: symptoms that persist, worsen, spread, or begin to affect daily life. MND is uncommon, but early medical advice helps doctors check the cause and offer the right support sooner.

Why Caregivers Often Notice MND Symptoms First

Caregivers often notice changes before anyone else because they see the person in ordinary moments. They may watch them button a shirt, hold a cup, climb the stairs, walk across the room, or eat a meal.

Small changes can stand out. A person may drop cutlery more often, struggle to turn a key, drag one foot, avoid stairs, speak more softly, or cough during meals. These signs may seem minor at first, but a caregiver can spot when they become repeated patterns.

A caregiver does not diagnose MND. That role belongs to a GP, neurologist, and medical tests. But a caregiver can do something very important: notice what has changed, write it down, and encourage the person to seek medical advice when symptoms persist or get worse.

Many MND stories first symptoms mention everyday changes like weak hands, tripping, or speech changes. However, personal stories and an MND first symptoms forum should never replace professional assessment. They can offer reassurance, but only a healthcare professional can investigate the real cause.

RELATED: What Is Safeguarding in Care? 2026 Update

Common Early Signs of MND

The common early signs of MND usually involve muscles becoming weaker over time. The first change may appear in the hands, feet, legs, speech, or swallowing, depending on which muscles MND affects first.

Families and caregivers may notice:

- Weak or stiff hands

- A weaker grip

- Dropping cups, keys, cutlery, or pens

- Difficulty with buttons, zips, writing, or opening jars

- Foot drop or dragging one foot

- Repeated tripping or falls

- Trouble climbing stairs

- Muscle cramps or spasms

- Muscle twitching, especially when it appears with weakness

- Slurred, faint, or nasal-sounding speech

- Coughing, choking, or struggling when swallowing

- A weaker cough or breathlessness

MND symptoms hands often worry families because hand weakness can affect everyday tasks quickly. Someone may stop writing clearly, struggle to hold a toothbrush, or avoid tasks they once managed easily.

Twitching alone does not usually mean MND. Many people experience twitching from stress, tiredness, exercise, caffeine, or minor nerve irritation. The bigger concern comes when twitching appears with weakness, wasting, speech changes, swallowing problems, or symptoms that keep getting worse.

What Can Be Mistaken for Motor Neurone Disease?

Several conditions can look like MND at first, which is why families should avoid self-diagnosing from one symptom. A trapped nerve, muscle injury, vitamin B12 deficiency, thyroid problems, medication side effects, stress, anxiety, or another neurological condition can cause weakness, twitching, tiredness, or changes in movement.

Many people search “convinced I have motor neurone disease” after noticing twitching, fatigue, or weakness. That fear feels real, but MND usually causes weakness that gradually worsens rather than symptoms that come and go quickly.

Fatigue also needs context. If you keep asking, “why do I feel tired and fatigued all the time?”, the cause may involve sleep, stress, anaemia, infection, low mood, thyroid issues, vitamin deficiency, or another health problem. Tiredness alone does not usually point to MND.

Vertigo can also confuse families because it affects balance. But vertigo often feels like spinning, dizziness, or unsteadiness, not progressive muscle weakness. If you wonder how long can a bout of vertigo last, the answer depends on the cause, but it can last seconds, hours, days, or longer.

The safest approach is simple: track the symptoms, look for patterns, and speak to a GP if weakness persists, spreads, or affects walking, grip, speech, swallowing, or breathing.

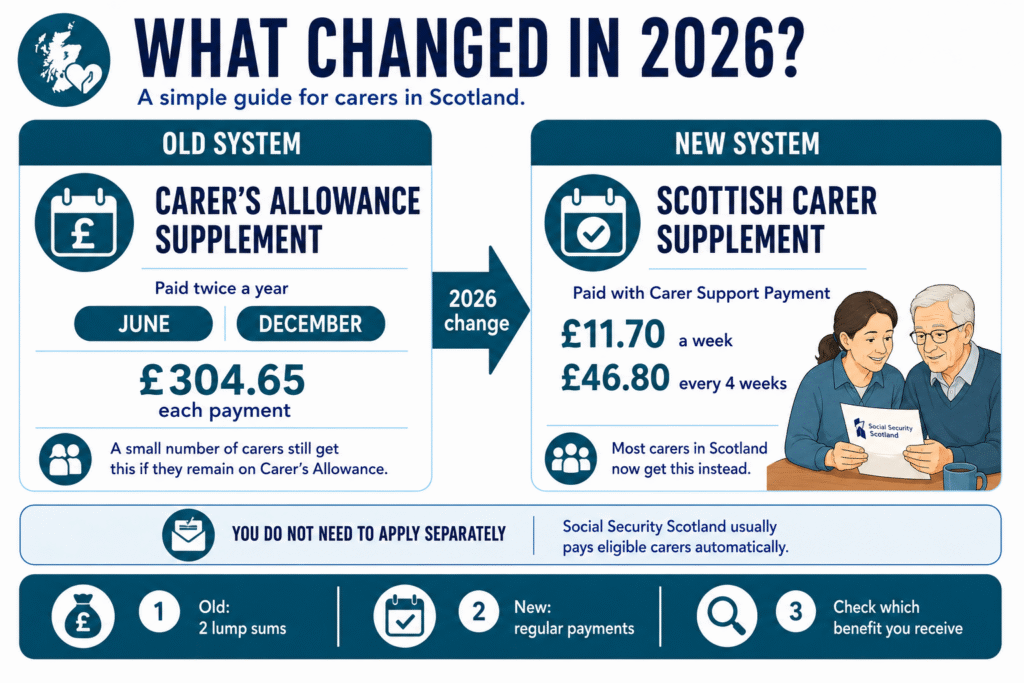

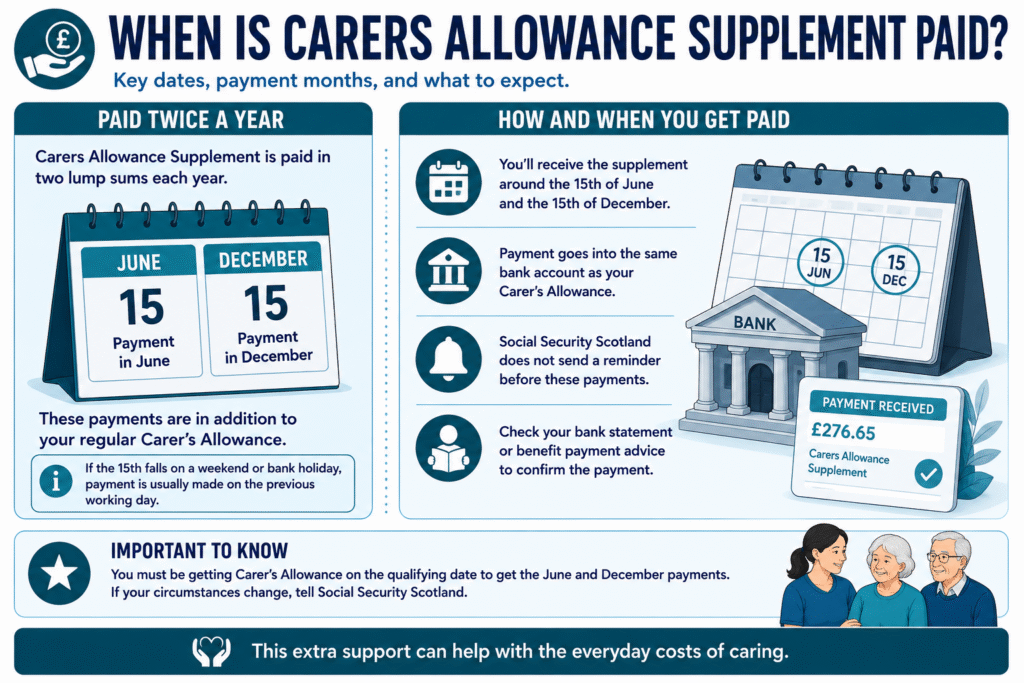

READ MORE: Carers Allowance Supplement: What Scotland’s Carers Need to Know in 2026

Is ALS the Same as MND?

Yes, ALS is a type of MND. In the UK, people usually use the term motor neurone disease, or MND, to describe a group of conditions that affect the nerves controlling movement. In the United States, people often use ALS more commonly.

ALS stands for amyotrophic lateral sclerosis. It is the most common type of MND and can affect muscles in the arms, legs, speech, swallowing, and breathing over time.

So, if someone asks “is ALS the same as MND?” or “is MND and ALS the same?”, the simple answer is: ALS falls under the wider MND family. The terms may differ by country, but both refer to serious conditions that affect motor neurones and gradually weaken muscles.

Is MND Hereditary or Genetic?

Most cases of MND do not run in families. In many people, doctors cannot point to one clear cause, and the condition appears without a known family history.

Still, some families worry and ask, “is MND hereditary?”, “is MND inherited?”, or “is MND genetic?” These questions matter, especially when more than one person in the family has had MND or a related neurological condition.

A small number of MND cases involve inherited genetic changes. If MND runs in the family, the person should speak to a GP or neurologist about the next step. The doctor may suggest genetic counselling before any genetic testing, so the family can understand what the results may mean.

From a caregiver’s perspective, the most helpful step is not to assume. Record symptoms, ask about family history, and encourage medical advice if weakness, speech changes, swallowing problems, or mobility issues continue to worsen.

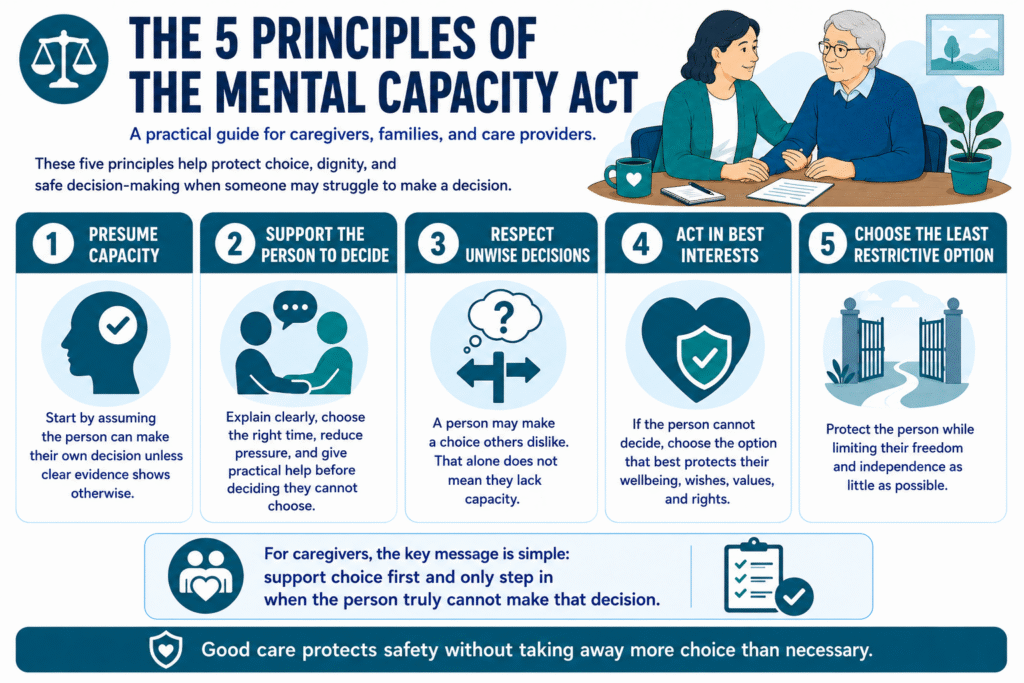

SEE MORE: The 5 Principles of Mental Capacity Act: A Practical Guide for 2026

Can You Prevent Motor Neurone Disease?

There is no proven way to prevent motor neurone disease. Researchers still do not know exactly why most cases happen, and MND causes can involve a mix of genetic, environmental, and biological factors.

That can feel frustrating for families, especially when they want a clear action plan. But prevention is not the same as early action. Caregivers can still help by encouraging regular health checks, balanced nutrition, safe movement, and prompt medical advice when new weakness or speech changes appear.

If someone asks how to prevent motor neuron disease, the honest answer is that no lifestyle change can guarantee prevention. However, noticing symptoms early, recording changes, and speaking to a GP can help rule out other treatable causes and get the right support in place sooner.

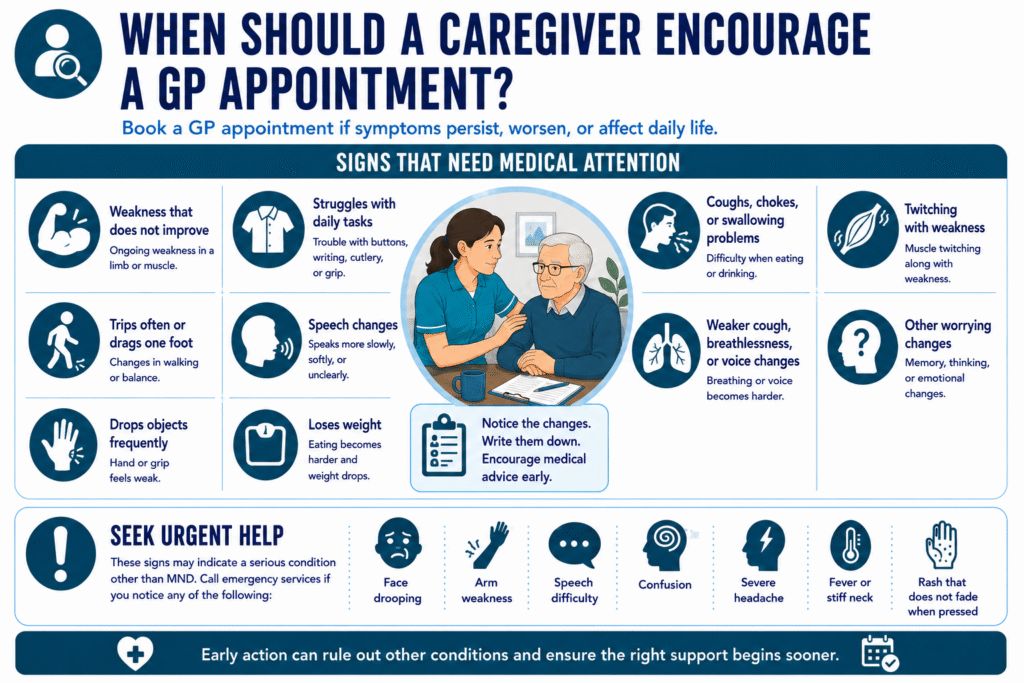

When Should a Caregiver Encourage a GP Appointment?

A caregiver should encourage a GP appointment when symptoms persist, worsen, or start to affect daily life. One weak day may not mean something serious, but repeated changes deserve attention.

Book a GP appointment if someone:

- Develops weakness that does not improve

- Trips often or starts dragging one foot

- Drops objects because their hand feels weak

- Struggles with buttons, writing, cutlery, or grip

- Speaks more slowly, softly, or unclearly

- Coughs, chokes, or struggles when swallowing

- Has twitching together with weakness

- Loses weight because eating becomes harder

- Shows a weaker cough, breathlessness, or voice changes

Some symptoms need urgent help because they may point to something other than MND. Call emergency services if someone suddenly develops face drooping, arm weakness, speech difficulty, confusion, severe headache, fever, stiff neck, or a rash that does not fade when pressed.

Families sometimes ask how does meningitis start, how can you catch meningitis, or how do you catch meningitis B because sudden illness can feel frightening. Meningitis is different from MND, but symptoms such as fever, severe headache, stiff neck, confusion, or a non-fading rash need urgent medical attention.

ALSO READ: Band C Council Tax Per Month: What You Should Know in 2026

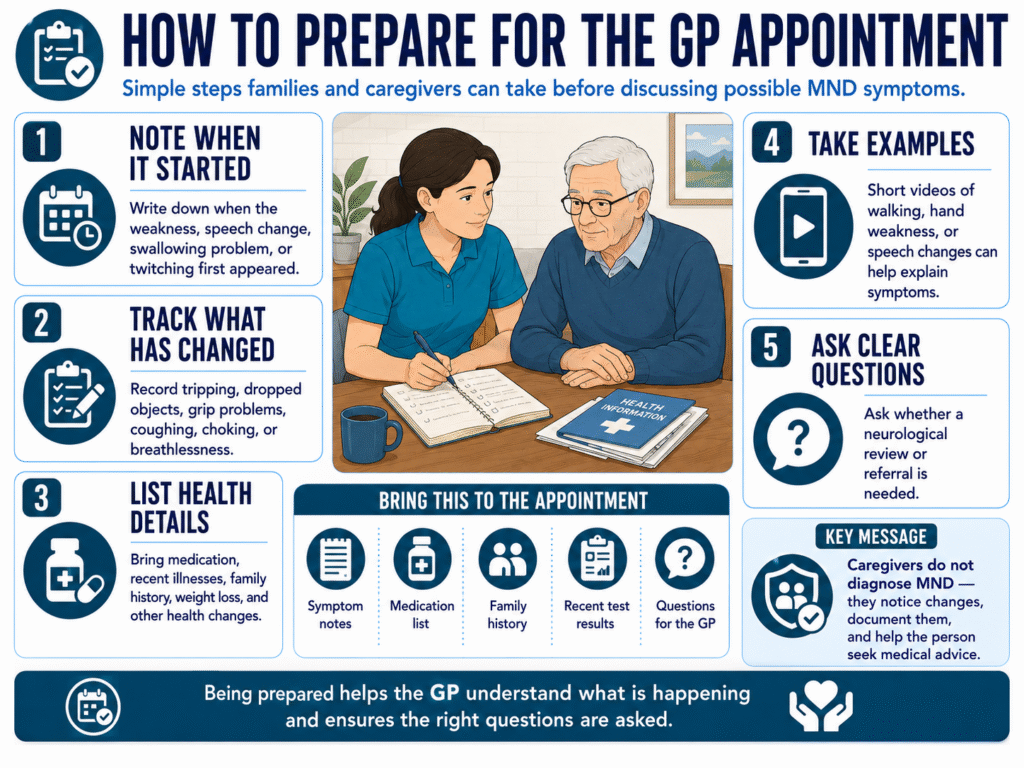

How to Prepare for the GP Appointment

Before the appointment, write down what has changed and when it started. Clear notes help the GP understand the pattern, especially when symptoms come and go or feel difficult to explain.

A caregiver can help by recording:

- Which body part showed symptoms first

- Whether weakness affects the hand, foot, leg, speech, or swallowing

- How often the person trips, drops objects, coughs, or chokes

- Whether symptoms have worsened or spread

- Any muscle cramps, twitching, stiffness, or visible muscle loss

- Recent injuries, infections, stress, medication changes, or weight loss

- Family history of MND or other neurological conditions

Short videos can also help if the symptom does not always appear during the appointment. For example, a video of foot dragging, hand weakness, speech changes, or repeated difficulty with a daily task may give the GP useful context.

Forums and personal stories can make people feel less alone, but they cannot confirm a diagnosis. If someone feels worried after reading MND stories online, encourage them to take the next practical step: collect the facts, book the appointment, and let a healthcare professional investigate properly.

Final Caregiver Advice

An early sign of MND can feel frightening, especially when weakness, speech changes, or swallowing problems begin to affect daily life. But fear should not become self-diagnosis. Many symptoms that worry families can come from other causes, and some of those causes can be treated.

A caregiver’s role is not to diagnose MND. It is to notice, document, support, and act early.

If someone you care for develops weakness that keeps getting worse, starts tripping, drops objects often, speaks differently, or struggles with swallowing, encourage them to see a GP. Clear notes, calm support, and early medical advice can help doctors investigate the cause and guide the next step.

The most helpful thing a caregiver can do is stay observant without creating panic. Notice the changes, protect the person’s dignity, and help them get the right medical support at the right time.

Need Clearer Care Guidance for Your Team?

Early symptoms can be easy to miss, especially when changes happen slowly. Caregivers who know what to notice can support families sooner and encourage the right medical help at the right time.

At Care Sync Experts, we provide practical, caregiver-focused guidance that helps care teams recognise concerns, respond with confidence, and support safer care decisions.

Help your carers notice changes early and act with confidence.

FAQ

At what age does MND start?

MND can affect adults at different ages, but it usually starts in people over 50. Younger adults can develop it too, but this is less common. If someone develops ongoing weakness, foot drop, speech changes, or swallowing problems at any age, they should speak to a GP rather than waiting to see if it disappears. The NHS says MND can affect adults of any age but usually affects people over 50.

Is MND painful at first?

MND does not usually start with pain as the main symptom. Early symptoms more often involve weakness, stiffness, cramps, twitching, tripping, weak grip, speech changes, or swallowing difficulties. Pain can still happen because of muscle cramps, stiffness, poor posture, reduced movement, or falls, but pain alone usually points doctors to check for other causes too.

Would MND show up in a blood test?

A standard blood test does not confirm MND on its own. Doctors may use blood tests to rule out other causes of symptoms, such as vitamin deficiencies, thyroid problems, inflammation, or other illnesses.

Diagnosis usually depends on a neurological examination and tests such as nerve tests, EMG, MRI scans, and other investigations. The NHS says there is no single test for MND.

What is Stage 1 motor neurone disease?

“Stage 1” usually refers to the early stage of MND, when symptoms may affect one area first, such as the hand, foot, leg, speech, or swallowing muscles.

At this point, a person may still manage many daily activities but notice weakness, stiffness, cramps, twitching, tripping, or grip problems.

MND progression varies from person to person, so doctors focus more on the person’s symptoms, function, and support needs than a simple numbered stage.