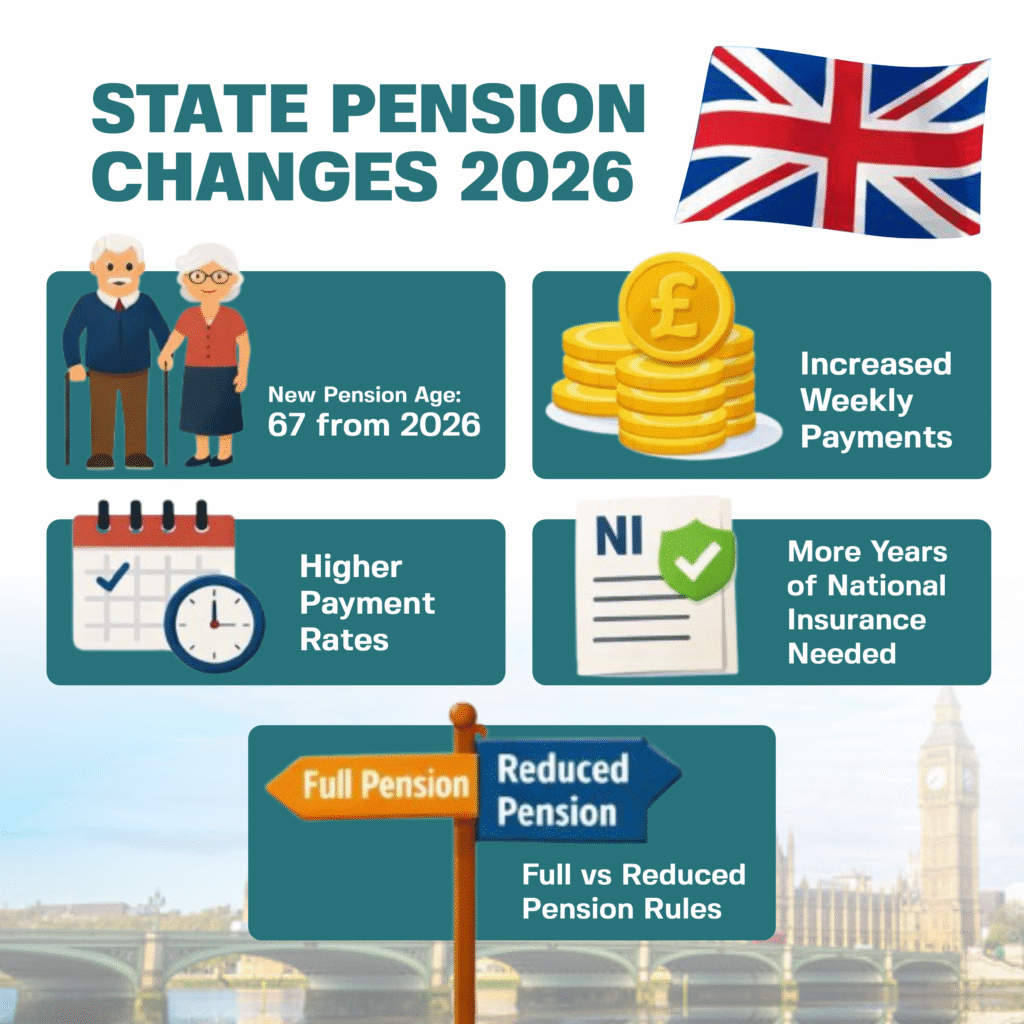

The UK State Pension age increase 2026 will raise the retirement age from 66 to 67 between April 2026 and April 2028. This change affects people born on or after 6 April 1960, meaning they will retire at age 67 instead of 66, depending on their exact birth date. The government introduced this state pension age increase to reflect longer life expectancy and reduce long-term pension costs.

If you’re asking “when can I retire?”, the answer now depends on your date of birth. The increase does not apply all at once, it rolls out gradually over two years, so some people will wait a few extra months, while others will wait the full year.

For care providers and their staff, this means many workers will remain in employment longer, making it essential to understand how the UK state pension age increase 2026 affects retirement planning and workforce decisions.

The state pension age increase 2026 affects anyone born on or after 6 April 1960. If an employee falls into this group, they will not receive their State Pension at 66. Instead, they will need to wait until they reach age 67, depending on their exact birth date.

The increase does not apply equally to everyone. The government is rolling it out in phases between April 2026 and April 2028. For example, someone born in April 1960 may wait only a few extra months, while someone born later in the year could wait much longer.

From a caregiver business perspective, this change directly impacts your workforce:

Many experienced caregivers will stay in employment longer

Retirement timelines will become less predictable

Workforce planning will require closer tracking of staff age and retirement expectations

The DWP state pension age change 2026 also means employers can no longer assume that staff in their mid-60s will retire soon. Instead, care providers should expect a gradual shift, where older employees remain active in the workforce for an extended period.

Understanding who is affected by the UK state pension age increase allows care businesses to plan staffing levels, manage expectations, and avoid sudden workforce gaps.

When Can You Retire Now? (Use the Official Calculator)

State Pension Changes 2026- New Payment Rates and Age Rules

If you’re asking “when can I retire?”, the answer now depends entirely on your date of birth. The state pension age increase 2026 means there is no single retirement age anymore; each person has a specific date.

The easiest way to check is by using the official UK State Pension age calculator on GOV.UK. This tool gives you your exact retirement date based on current legislation.

Quick Answer:

Your State Pension age depends on your date of birth, and you should use the official UK State Pension age calculator to confirm when you can retire.

How to check your pension age:

Go to the GOV.UK pension calculator

Enter your date of birth

View your exact State Pension age and date

You can also check a state pension forecast to see how much you’re likely to receive under the New State Pension 2026 rules.

Caregiver businesses should encourage staff, especially those aged 55+, to use the UK State Pension calculator. This helps:

Set realistic retirement expectations

Prevent sudden staffing gaps

Support better workforce planning

Because of the UK state pension age increase 2026 calculator results, two employees of the same age may now retire at different times. Care providers must account for this variation when planning schedules, hiring, and succession.

How Much Is the State Pension in 2026/27?

The state pension increase 2026/27 raises payments by 4.8%, in line with average earnings under the triple lock policy. This means higher weekly income for pensioners starting from April 2026.

Current Rates:

New State Pension 2026:

£241.30 per week (£12,547.60 per year)

Basic State Pension (pre-2016 retirees):

£184.90 per week (£9,614.80 per year)

The New State Pension in 2026 will pay up to £241.30 per week, depending on your National Insurance record.

To receive the full amount, individuals typically need 35 years of qualifying National Insurance contributions. Those with fewer years will receive a reduced amount.

How much is the state pension for a woman?

The amount is the same for men and women under the current system. What matters is the individual’s National Insurance record, not gender.

Understanding the state pension increase 2026 helps care businesses:

Support staff with retirement planning

Explain income expectations to older employees

Reduce uncertainty around financial readiness

Many caregivers may rely heavily on the New State Pension 2026, especially if they do not have private pensions. Encouraging staff to check their state pension forecast ensures they understand what they will actually receive and whether they need to work longer.

The UK state pension age increase 2026 will directly affect how care providers manage their workforce. As employees delay retirement, your staffing model will shift, both positively and negatively.

Quick Insight:

The state pension age increase means more experienced caregivers will stay in the workforce longer, but it also increases the risk of burnout and workforce imbalance.

1. Longer Staff Retention

Many caregivers who planned to retire at 66 will now continue working until 67.

This can benefit your business:

You retain experienced staff longer

You reduce short-term recruitment pressure

You maintain continuity of care for clients

2. Increased Burnout Risk

Older caregivers may:

Struggle with physically demanding roles

Experience fatigue or reduced mobility

This creates a real operational risk if not managed properly.

3. Workforce Planning Becomes Critical

The UK pension age reform impact means you must actively plan for:

Gradual retirement timelines

Flexible working options

Succession planning

You can no longer assume when staff will leave. Instead, you must track and manage retirement expectations.

4. Recruitment Strategy Must Evolve

With delayed retirement:

Fewer roles may open up immediately

Younger workers may face slower entry into the sector

Care providers should balance:

Retaining experienced staff

Bringing in new talent

What smart care providers are doing

Forward-thinking providers are already:

Offering flexible shifts for older staff

Reducing physically demanding tasks

Encouraging staff to check their state pension forecast

Staying updated with pension news and DWP changes

The state pension age increase is not just a policy change, it is a workforce shift. Care providers who adapt early will maintain stability, reduce risk, and stay competitive.

Should Care Providers Adjust Workforce Planning Now?

UK Payroll Updates- 2026_27 Changes and Compliance

Yes, care providers should start adjusting workforce planning now. The state pension age increase 2026 will delay retirement for many employees, which changes how you manage staffing, scheduling, and long-term growth.

Care providers should adjust workforce planning now if they rely on older staff, because the state pension age increase will delay retirement and change workforce availability.

When you SHOULD adjust now

You should act immediately if:

A large portion of your workforce is aged 55+

You rely heavily on experienced caregivers

You expect staff to retire soon based on old assumptions

In these cases, the state pension age increase will directly affect your staffing timeline.

When adjustment is less urgent

You may not need immediate changes if:

Your workforce is mostly younger (under 50)

You already have strong recruitment pipelines

You use flexible or agency staffing models

Practical steps care providers should take

To adapt effectively:

Review staff age profiles and expected retire at age timelines

Encourage employees to check when can I retire using official tools

Offer flexible roles for older staff

Introduce succession planning early

Train younger staff to prepare for future leadership roles

The risk of doing nothing

If you ignore the state pension age increase 2026, you may face:

Unexpected staff shortages

Burnout among older employees

Poor workforce planning decisions

The state pension age increase is already underway. Care providers who respond early will maintain stability, support their staff better, and avoid operational disruptions.

Future Pension Changes You Should Watch (2025–2046)

The state pension age increase 2026 is only one part of a wider shift in UK pension policy. Care providers should stay informed about upcoming changes, because these updates will continue to affect workforce planning and staff expectations.

Quick Insight:

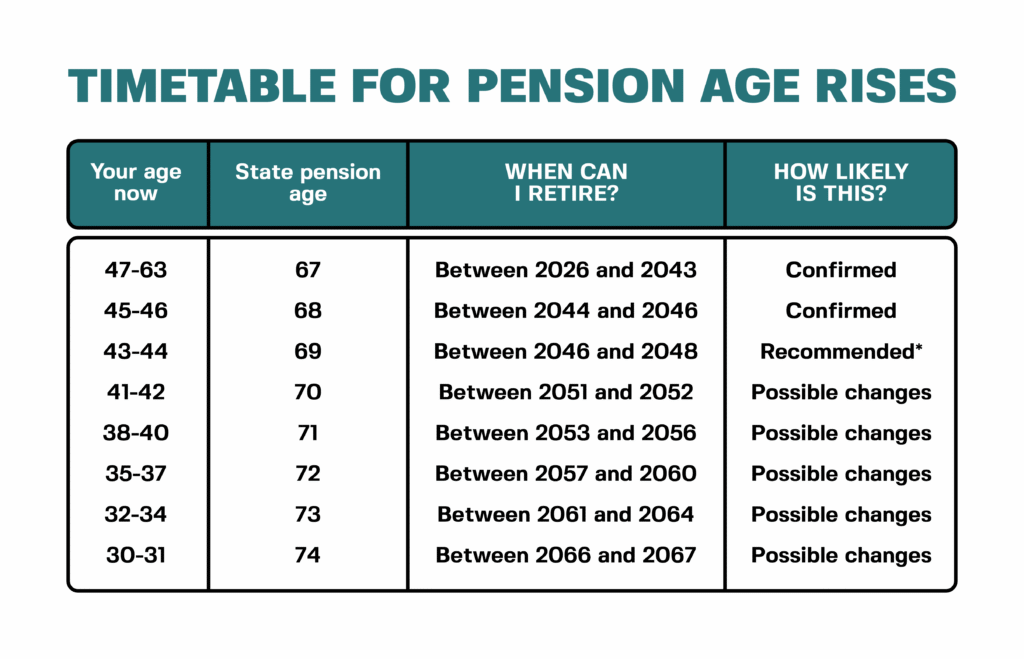

The UK government plans to increase the State Pension age to 68 in the future, and ongoing policy reviews could bring further changes.

1. Planned Increase to Age 68

The government has already scheduled another state pension age increase:

Age 68 is expected between 2044 and 2046

Future reviews may bring this forward depending on life expectancy and economic conditions

This means younger caregivers may need to work even longer before they retire at age.

2. Ongoing Reviews and DWP Updates

The Department for Work and Pensions (DWP) regularly reviews pension policy. Recent pension news highlights:

Potential adjustments based on life expectancy trends

Discussions around affordability and sustainability

Occasional DWP state pension warnings about planning ahead

Care providers should monitor these updates to avoid being caught off guard.

3. Other Pension Changes to Watch

Several related updates may also impact your staff:

UK pensioner cash withdrawal changes 2025 – potential changes in how pension funds are accessed

UK state pension reduction 2025 – concerns around reduced real value due to inflation or policy shifts

September 2025 state pension updates – periodic policy announcements affecting benefits

These changes may influence how employees view retirement and financial security.

Understanding future pension trends helps you:

Prepare for long-term workforce changes

Support staff with realistic retirement expectations

Stay aligned with UK pension age reform impact

The UK state pension age increase will continue evolving. Care providers who stay informed and adapt early will remain stable, competitive, and better prepared for future workforce challenges.

Common Questions About the UK State Pension Age Increase 2026

uk state pension age increase 2026

When will the State Pension age reach 67?

The state pension age increase 2026 will raise the retirement age from 66 to 67 between April 2026 and April 2028. The change happens gradually, so not everyone reaches 67 at the same time.

Can I still retire at 66?

Yes, you can still retire at 66, but you may not receive your State Pension yet. If you fall under the UK state pension age increase, you will need to wait until your official pension age before receiving payments.

How do I check when I can retire?

You should use the official UK State Pension age calculator.

Your exact retirement age depends on your date of birth, and the calculator provides the most accurate answer.

You can also check your state pension forecast to understand how much you’ll receive.

Will the State Pension age increase again?

Yes. The government has already planned another state pension age increase to 68 between 2044 and 2046, although future reviews may change this timeline.

What happens if I don’t have enough National Insurance contributions?

You may receive less than the full New State Pension 2026 amount. To qualify for the full payment, you typically need 35 years of contributions. If you have gaps, you may still qualify for a partial pension.

Does the State Pension amount differ for men and women?

No. The amount is the same for both. The key factor is your National Insurance record, not gender.

If you’re wondering how much is the state pension for a woman, the answer is the same as for men under the current system.

These questions reflect the most common concerns around the UK state pension age increase 2026. Clear answers help both individuals and care providers plan more effectively.

Conclusion

The UK state pension age increase 2026 is more than a policy update—it’s a workforce shift that care providers must manage proactively.

What you should do now:

Expect staff to retire at age 67, not 66

Encourage employees to check when can I retire using the UK State Pension age calculator

Support staff in reviewing their state pension forecast

Adjust workforce planning to reflect delayed retirement

Introduce flexible roles to reduce burnout among older caregivers

Stay updated with pension news and DWP state pension age change 2026 developments

Care providers who understand the state pension age increase early will manage staffing better, retain experienced workers, and avoid sudden workforce gaps.

The state pension age increase 2026 is already shaping the future of the care sector. By acting now, you can protect your workforce, support your staff, and keep your operations stable in a changing environment.

Need Support Managing Workforce Changes from the State Pension Age Increase?

The UK state pension age increase 2026 can disrupt staffing plans, delay retirements, and increase pressure on your existing team if not managed early.

Care Sync Experts helps you:

Plan for delayed retirement and workforce shifts

Retain experienced caregivers without increasing burnout

Build flexible staffing models that support older employees

Improve workforce stability and reduce sudden staff shortages

Stay aligned with regulatory expectations and long-term care demands

Get practical, expert guidance to adapt your care service, support your staff, and stay ahead of pension-related workforce changes.

FAQ

Do I get my husband’s State Pension if he dies?

You may be able to receive part of your husband’s State Pension, depending on your circumstances. This is usually called inheriting State Pension or qualifying for bereavement benefits. – If you reached State Pension age before April 2016, you may inherit some of your partner’s pension based on their National Insurance record. – If you’re under the new State Pension system (after April 2016), inheritance is more limited, but you may still qualify for Bereavement Support Payment (BSP).

The exact amount depends on contributions, age, and marital status.

How long is pension paid after death in the UK?

State Pension payments stop shortly after death. However: – Payments may continue briefly if they were already issued before the death was reported – Any overpayments must usually be returned – A surviving spouse or partner may qualify for bereavement benefits instead

You should report a death to the DWP immediately to avoid complications.

Can I pass my pension to my children?

You cannot pass your State Pension directly to your children. The State Pension is not treated as a transferable asset. However: – Private or workplace pensions can often be passed on, depending on the scheme – Beneficiaries may receive lump sums or ongoing payments

Always check the specific rules of your pension provider.

What is the minimum salary to qualify for State Pension in the UK?

There is no fixed minimum salary to qualify for the State Pension. Instead, eligibility depends on National Insurance (NI) contributions. – You typically need at least 10 qualifying years to receive any pension – You need 35 years to receive the full New State Pension 2026

You earn qualifying years by: – Working and paying NI contributions – Receiving NI credits (e.g., for caregiving, unemployment, or illness)

Even low earners can qualify, as long as they meet the contribution requirements.

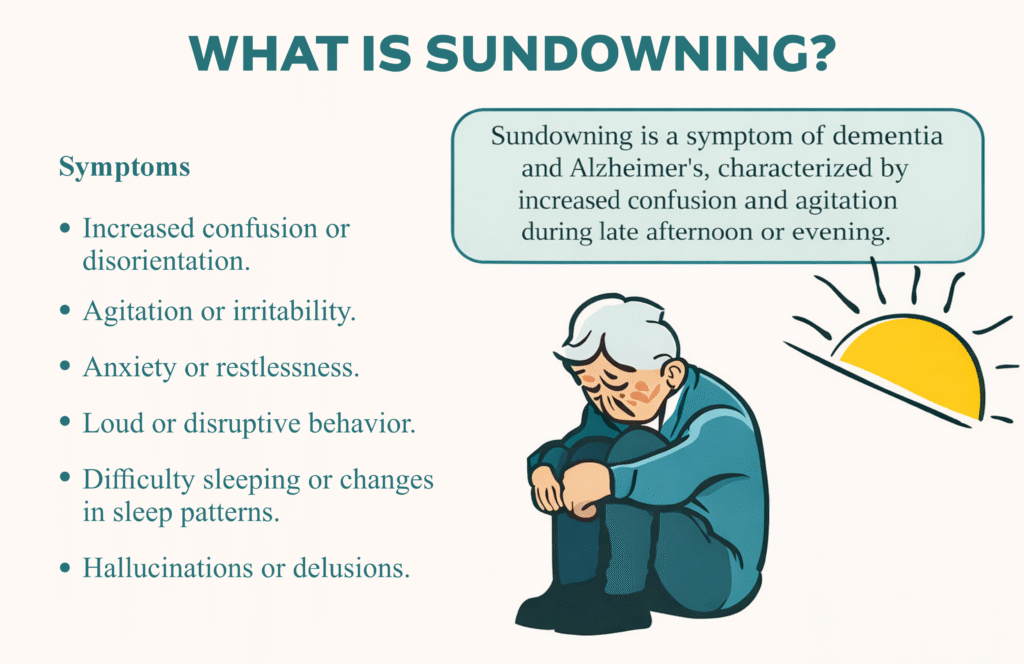

Sundowning typically starts in the late afternoon, usually between 3 p.m. and 5 p.m., and continues into the evening and night. This pattern often aligns with the time the sun begins to set, so changes in light, like knowing what time is sundown today UK, can influence when symptoms begin.

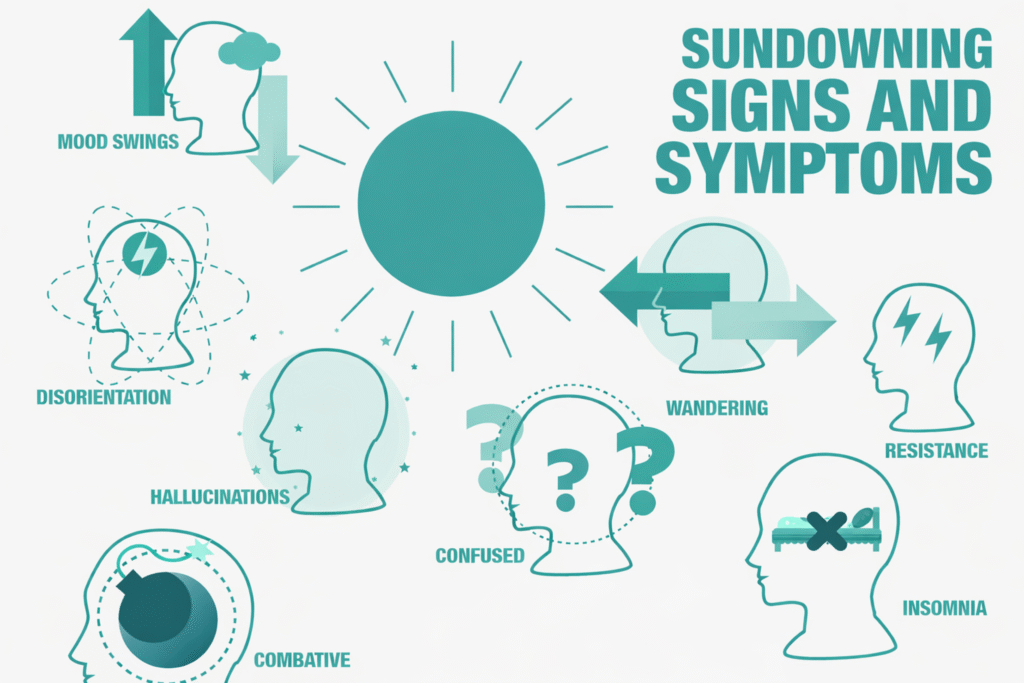

Sundowning dementia refers to a group of behaviors, such as confusion, agitation, and restlessness, that worsen as daylight fades. While most caregivers notice symptoms in the evening, some individuals may also experience sundowning in the morning, especially when sleep patterns are disrupted.

For caregivers, understanding what time is sundowning helps you anticipate changes in behavior and prepare the environment before symptoms escalate.

What time is sundowning? It usually starts between 3 p.m. and 5 p.m. and can continue into the night.

Sundowning dementia is not a disease. It is a pattern of symptoms like confusion, anxiety, and agitation that worsen later in the day.

Symptoms often peak around sunset, especially as lighting changes and fatigue builds.

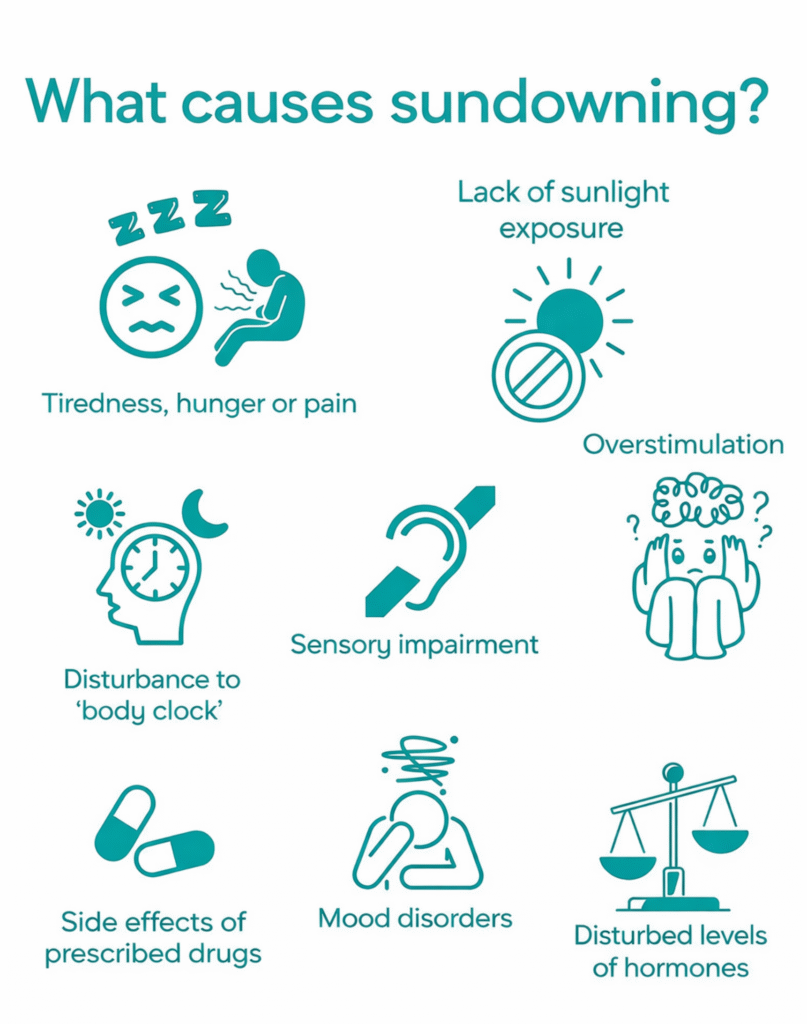

What triggers sundowning? Common triggers include tiredness, low lighting (sometimes called night shading), hunger, and disrupted routines.

Behaviour can become challenging, including restlessness, wandering, or even aggressive dementia episodes in some individuals.

Early preparation helps. Adjusting lighting, reducing noise, and maintaining a calm routine can reduce symptoms.

Each person is different. While evening is most common, some people may show symptoms at other times of the day.

What Is Sundowning in Dementia and Why It Happens

Sundowning in dementia is a pattern of increased confusion, agitation, and behavioral changes that appear later in the day, typically as daylight fades. It is not a disease on its own; it is a symptom seen in people living with conditions like Alzheimer’s or vascular dementia. Many caregivers also hear it described as “sundowner syndrome,” which reflects the same late-day changes.

You may notice that a calm loved one suddenly becomes restless, anxious, or even upset without a clear reason. In some cases, dementia and being mean to family can become more noticeable during these hours, not because the person intends harm, but because their brain struggles to process reality, emotions, and surroundings.

Why does sundowning happen?

Sundowning happens due to a combination of physical and environmental factors:

Brain changes from dementia disrupt the body’s internal clock (circadian rhythm)

Fatigue builds up after a full day of activity

Reduced daylight and increasing shadows (sometimes called night shading) create confusion

Difficulty distinguishing reality from imagination may lead to fear or suspicion

In some cases, these changes can lead to aggressive dementia behaviors, including shouting, pacing, or resisting care. This can feel overwhelming for caregivers, especially when it happens suddenly or daily.

Understanding what is sundowning in dementia helps you recognize that these behaviors are not personal, they are part of how the condition affects the brain.

What Time Does Sundowning Start, and How Long Does It Last?

How to Manage Sundowning in 2026

Sundowning usually begins in the late afternoon, around 3 p.m. to 5 p.m., and can continue into the evening and night. For many caregivers, the timing closely follows sunset, so checking what time is sundown today or what time is sundown tonight can help you anticipate when symptoms may begin.

When does it peak?

Symptoms often peak around sunset, when natural light fades, and shadows increase. During this period, you may notice:

Increased confusion

Restlessness or pacing

Anxiety or irritability

How long does sundowning last?

Sundowning can last for several hours, sometimes easing once the person settles into nighttime routines or sleep. However, the duration varies:

Some individuals calm down after a few hours

Others may remain unsettled late into the night

Does it always happen in the evening?

Not always. While evening is most common:

Some people experience sundowning in the morning, especially if their sleep cycle is disrupted

Others may have irregular patterns depending on fatigue, environment, or health changes

Is sundowning linked to life expectancy?

Many caregivers ask about life expectancy with sundowners, but sundowning itself does not determine lifespan. It reflects how dementia affects brain function and daily rhythms, not how long someone will live.

Understanding what time is sundowning allows you to prepare ahead, adjust lighting, reduce stimulation, and create a calm routine before symptoms escalate.

What Triggers Sundowning in Dementia Patients?

Sundowning does not happen randomly. Certain factors increase confusion and agitation, especially later in the day. When caregivers understand what triggers sundowning, they can prevent or reduce many episodes before they escalate.

Common triggers of sundowning

Fatigue after a long day

The brain becomes more overwhelmed as energy levels drop.

Low lighting and shadows (night shading)

Dim environments can distort perception and increase fear or confusion.

Disrupted body clock (circadian rhythm)

Dementia affects the brain’s ability to regulate sleep and wake cycles.

Hunger, dehydration, or discomfort

Unmet physical needs can quickly turn into agitation.

Unfamiliar environments or changes in routine

New settings or unexpected changes can increase anxiety.

Medications that cause sundowning

Some drugs, especially sedatives or medications affecting sleep, may worsen confusion or agitation.

Underlying medical issues

Infections, pain, or conditions like urinary tract infections can intensify symptoms.

Does the type of dementia matter?

Yes. For example, vascular dementia sundowning may present differently depending on how blood flow changes affect the brain. Some individuals may experience more sudden mood shifts or confusion compared to other types of dementia.

Caregiver insight

You may notice patterns over time. For example:

Agitation increases after poor sleep

Confusion worsens in dim lighting

Behavior changes after certain medications

Tracking these patterns helps you identify what triggers sundowning for your loved one specifically, and respond more effectively.

Is Sundowning a Sign of Death or Disease Progression?

Sundowning Signs and Symbols

No, sundowning is not a sign of death. It does not mean that a person is nearing the end of life. Instead, sundowning reflects how dementia affects the brain’s ability to regulate behavior, light perception, and daily rhythms.

What sundowning actually indicates

Sundowning usually signals:

Changes in brain function caused by dementia

Increased sensitivity to fatigue and environmental changes

Disruption in the body’s internal clock (sleep–wake cycle)

As dementia progresses, these symptoms may become more noticeable, but they do not directly predict how long someone will live.

Understanding the confusion around life expectancy

Many caregivers search for life expectancy with sundowners, but it’s important to separate the two:

Sundowning is a behavioral pattern, not a disease stage

Life expectancy depends on the type and progression of dementia, overall health, and care quality

Some individuals experience sundowning early, while others develop it later

When should you be concerned?

While sundowning itself is not a sign of death, you should seek medical advice if:

Symptoms suddenly worsen

Behavior changes become extreme or unsafe

There are signs of infection, pain, or medication side effects

In some cases, medications that cause sundowning or untreated health issues can make symptoms appear more severe than they actually are.

Caregiver reassurance

It can feel alarming when a loved one becomes confused or agitated every evening. However, understanding that sundowning is a manageable symptom, not a terminal signal, helps you respond with clarity and confidence.

Yes, sundowning without dementia can happen, but it is less common. In most cases, sundowning is strongly linked to dementia, especially Alzheimer’s disease. However, similar late-day confusion or agitation can appear in people without a formal dementia diagnosis.

When sundowning happens without dementia

You may notice sundowning-like symptoms in situations such as:

Delirium (sudden confusion)

Often caused by infections, medication changes, or hospitalization

Severe sleep disruption

Poor sleep can confuse the brain’s internal clock and mimic sundowning patterns

Stress or anxiety

Emotional strain can increase restlessness or irritability later in the day

Medication side effects

Some medications that cause sundowning, such as sedatives or drugs affecting the nervous system, can trigger confusion even without dementia

How to tell the difference

Dementia-related sundowning tends to be consistent and progressive

Non-dementia cases are often sudden and reversible once the underlying cause is treated

For example, if confusion appears quickly and worsens over a few days, a medical issue like an infection may be the cause, not dementia.

Caregiver guidance

If you notice sundowning behaviors in someone without a dementia diagnosis:

Seek medical evaluation promptly

Review recent medication changes

Monitor sleep patterns and daily routines

Understanding whether symptoms are due to sundowning dementia or another condition helps you take the right action early.

How to Deal With Aggressive Dementia and Sundowning Behaviour

Sundowning can sometimes lead to aggressive dementia behaviors, including shouting, resistance to care, or even physical actions. As a caregiver, these moments can feel overwhelming, but your response can either calm or escalate the situation.

Why aggression happens during sundowning

Aggression often comes from:

Fear and confusion as surroundings become harder to recognize

Frustration from not being understood

Overstimulation or fatigue late in the day

Misinterpretation of people or shadows (especially with low lighting)

In many cases, what looks like anger is actually distress.

What to do with a violent dementia patient

If behavior becomes intense or unsafe:

Stay calm and keep your voice steady

Your tone directly affects their reaction

Give space and avoid confrontation

Do not try to physically restrain unless absolutely necessary

Redirect attention

Shift focus to a calming activity like music or a familiar object

Remove triggers

Reduce noise, dim harsh lighting, and create a quiet environment

Ensure safety first

Move sharp objects away and position yourself safely

How to deal with dementia patients who is aggressive

Use these daily strategies to reduce escalation:

Keep a consistent routine

Predictability reduces anxiety

Use simple, clear communication

Avoid long explanations or arguments

Validate their feelings

Instead of correcting them, respond with reassurance

Watch for patterns

Identify what triggers sundowning and act early

Stay patient, even when it’s difficult

Remember, the behavior is caused by the condition—not intent

Caregiver reality

Many caregivers struggle with dementia and being mean to family, especially during sundowning hours. It can feel personal, but it isn’t. The brain can no longer process emotions and reality correctly, which leads to reactions that seem out of character.

Understanding this helps you respond with empathy instead of frustration, and that alone can reduce how often aggressive episodes occur.

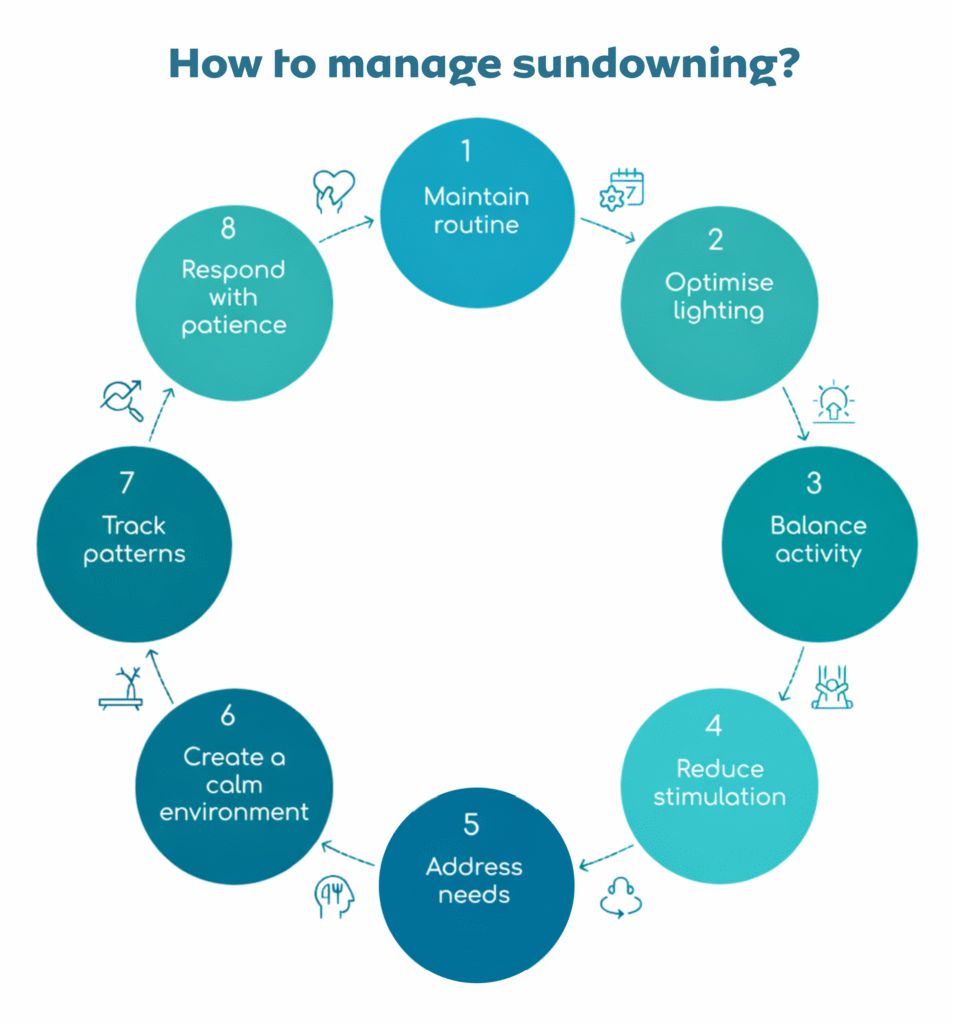

You cannot completely eliminate sundowning, but you can reduce how often it happens and how intense it becomes. Small changes in routine and environment make a big difference, especially when you apply them before symptoms start.

Create a calm, predictable routine

Keep consistent times for waking, meals, and bedtime

Schedule demanding activities earlier in the day

Avoid sudden changes in routine

A stable routine helps regulate the brain and reduces confusion later in the day.

Manage light and environment

Turn on lights before it gets dark to reduce shadows (night shading)

Keep rooms well-lit and familiar

Reduce background noise (TV, loud conversations)

Matching your environment to what time is sundown today UK can help you act early, before agitation begins.

Reduce physical and mental triggers

Offer meals and fluids regularly to avoid hunger or dehydration

Limit caffeine, especially in the afternoon

Encourage short rest periods, but avoid long daytime naps

Also review any medications that cause sundowning, especially if symptoms suddenly worsen.

Use calming activities

Play familiar, gentle music

Look through family photos

Take a short walk during daylight hours

These activities help shift focus and reduce anxiety.

Monitor patterns and act early

Track:

When symptoms start (based on what time is sundowning)

What happened earlier in the day

Environmental changes (lighting, noise, visitors)

Over time, you’ll identify patterns and prevent triggers before they escalate.

Caregiver reminder

Sundowning can be exhausting, especially when it happens daily. But early preparation, calm responses, and small adjustments can significantly reduce stress for both you and your loved one.

Final Thoughts…

Sundowning can feel unpredictable and exhausting, especially when behavior changes happen at the same time every day. But once you understand what time is sundowning and what drives it, you gain something powerful, control through preparation.

You are not dealing with intentional behavior. You are responding to how dementia changes the brain’s ability to process light, time, and surroundings. That’s why simple steps, like adjusting lighting, maintaining routines, and staying calm, can make a meaningful difference.

Focus on what you can control:

Prepare before late afternoon

Reduce known triggers

Respond with patience, not confrontation

Over time, you will begin to recognize patterns, anticipate changes, and handle even difficult moments, like aggressive dementia behaviors, with more confidence.

Most importantly, take care of yourself too. Supporting someone with sundowning dementia is demanding, and your well-being matters just as much as theirs.

Need Support Managing Sundowning in Your Care Service?

Sundowning can quickly lead to distress, aggression, and unsafe situations if not managed early.

Care Sync Experts helps you:

Reduce agitation and aggressive dementia episodes

Train staff to handle difficult behaviours confidently

Get practical, expert guidance to improve care outcomes and reduce daily stress for your team.

FAQ

Why is sundowning worse at night?

Sundowning becomes worse at night because the brain struggles more with fatigue, low lighting, and disrupted internal rhythms. As daylight fades, shadows increase and visibility drops, which can confuse a person with dementia. Combined with a full day of mental activity, this often leads to heightened agitation, anxiety, and disorientation in the evening.

Can sundowning happen after midnight?

Yes, sundowning can continue after midnight, especially if the person has not settled or has disrupted sleep. While symptoms usually begin in the late afternoon, some individuals remain restless, confused, or awake throughout the night. Poor sleep patterns can extend or worsen these behaviors.

What is the morning version of sundowning?

Some caregivers notice similar symptoms earlier in the day, often called “morning confusion” or reversed sundowning.” This can happen when sleep cycles are severely disrupted. Instead of worsening in the evening, the person may wake up confused, agitated, or disoriented in the morning.

How to respond to sundowning?

Responding effectively requires calm, proactive care: – Stay calm and speak in a reassuring tone – Avoid arguing or correcting the person – Redirect attention to a calming activity – Keep the environment quiet and well-lit – Maintain a consistent routine

The goal is not to “fix” the behavior instantly, but to reduce distress and create a sense of safety for the person.

Yes, a bladder infection can cause nausea, but it usually happens when the infection becomes more severe or spreads beyond the bladder. A simple lower urinary tract infection (UTI) typically causes urinary symptoms, but nausea often signals that the infection may have reached the kidneys or triggered a stronger body response.

This article will answer the popular question care workers mostly ask: will a bladder infection cause nausea. Caregivers should pay close attention when nausea appears alongside a UTI, as this may indicate a more serious condition that requires prompt medical treatment.

A urinary tract infection does not usually affect the stomach directly. However, certain changes in the body can trigger nausea, especially when the infection becomes more severe.

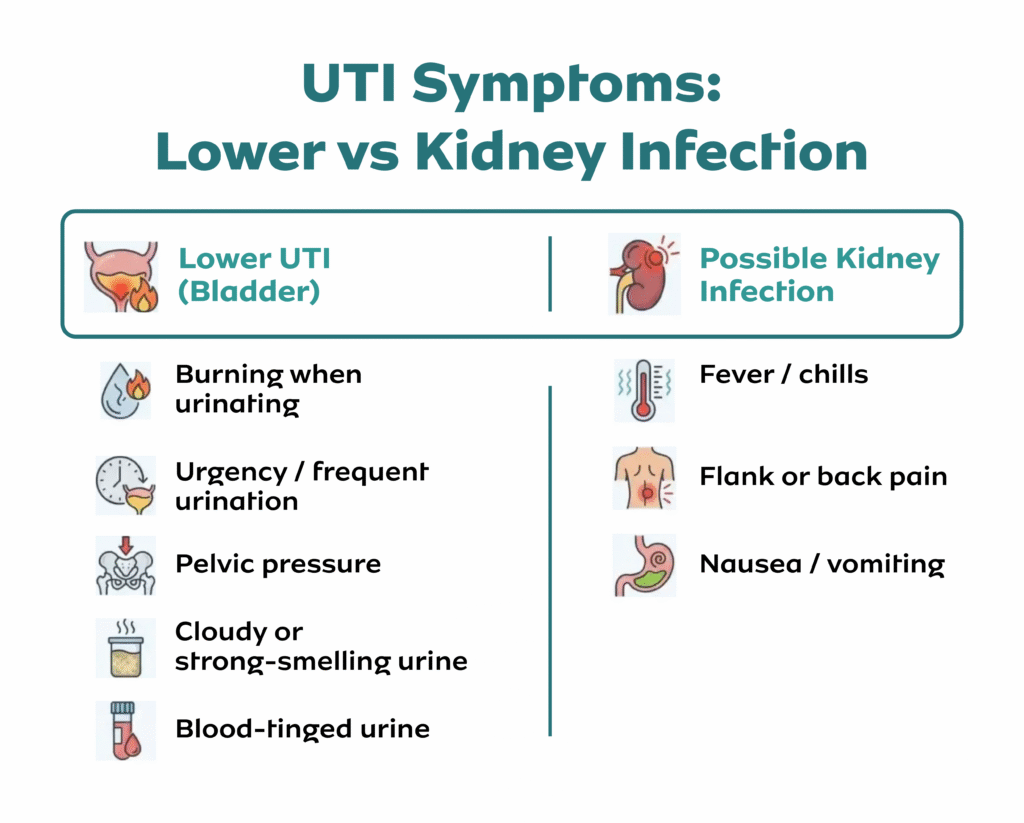

Infection Spreads to the Kidneys

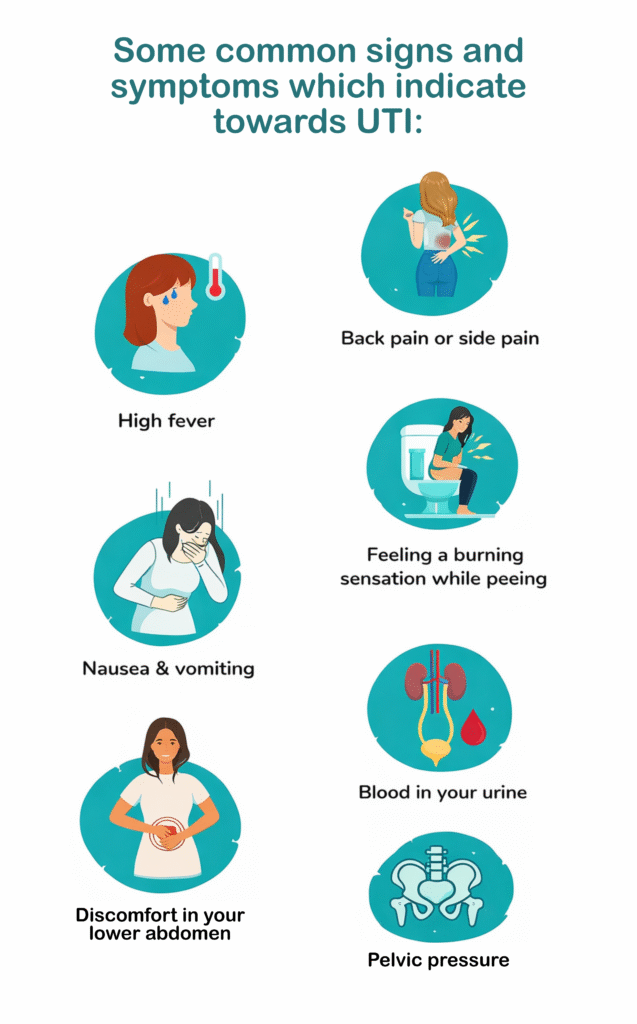

When bacteria move from the bladder to the kidneys, the infection becomes more serious (pyelonephritis). This stage often causes nausea, vomiting, fever, and back pain. Caregivers should treat this as urgent.

Strong Immune Response

The body reacts to infection by releasing inflammatory chemicals. This response can make a person feel unwell, tired, and nauseous. In some cases, the discomfort feels similar to flu symptoms.

Medication Side Effects

Some UTI antibiotics, such as nitrofurantoin, can cause nausea as a side effect. This does not always mean the infection is worsening, but caregivers should monitor symptoms closely.

Underlying Bladder Infection Causes

Different bladder infection causes, such as bacterial overgrowth, poor hygiene, or incomplete bladder emptying, can influence how severe the infection becomes. In women, understanding what causes a UTI in a woman (like shorter urethra or hormonal changes) helps explain why symptoms can escalate quickly.

For caregivers, the key takeaway is simple: nausea is not usually the first sign of a UTI, but when it appears, it often signals that the infection needs closer attention or medical review.

When Nausea Means Something Serious

Nausea alone does not always signal danger, but when it appears with certain symptoms, caregivers should act quickly. These combinations often point to a more serious infection, especially one affecting the kidneys.

Red Flags to Watch For

Fever and chills

Lower back or side pain

Vomiting or inability to keep fluids down

Severe fatigue or confusion (common in older adults)

Painful or frequent urination alongside worsening symptoms

These signs suggest the infection may have progressed beyond a simple bladder infection and now requires urgent treatment urinary tract infection care.

Special Situations Caregivers Must Not Ignore

UTI in pregnancy: Even mild symptoms can become serious quickly and require immediate medical attention.

Recurrent infections: If someone experiences repeated UTIs, caregivers may wonder, can recurrent UTIs be a sign of cancer? While this is rare, persistent infections should always be medically evaluated to rule out underlying conditions.

Caregiver Insight

Do not wait for symptoms to “settle.” If nausea appears alongside any of these warning signs, seek medical care immediately. Early intervention with proper urine infection treatment can prevent complications and speed up recovery.

A urinary tract infection often starts with mild, easy-to-miss symptoms. Caregivers should spot these early to prevent the infection from worsening.

General UTI Symptoms

Frequent urge to urinate

Burning sensation when urinating

Cloudy or strong-smelling urine

Lower abdominal or pelvic pain

Fatigue or general discomfort

These symptoms usually point to a lower UTI (bladder infection). When symptoms escalate, the risk of complications increases.

UTI Symptoms in Women

Women experience UTIs more often due to anatomy and hormonal factors. Many caregivers ask about the 10 causes of UTI in females, which commonly include poor hygiene, dehydration, sexual activity, and incomplete bladder emptying.

Understanding what causes a UTI in a woman helps caregivers act early and prevent recurrence. Women may also report pelvic pressure and a constant urge to urinate, even after emptying the bladder.

UTI Symptoms in Men

Although less common, UTI in men can be more serious and often linked to underlying conditions.

Caregivers should watch for:

Painful urination

Lower abdominal or rectal discomfort

Weak urine flow

Fever in more advanced cases

Questions like can guys get urinary tract infections, do males get UTIs, or does man get UTI come up often, the answer is yes, and when they do occur, they require careful attention.

Understanding male UTI symptoms and how a man gets a urinary tract infection (such as through prostate issues or urinary blockages) helps caregivers respond appropriately and seek timely care.

How to Treat a UTI (Caregiver Action Plan)

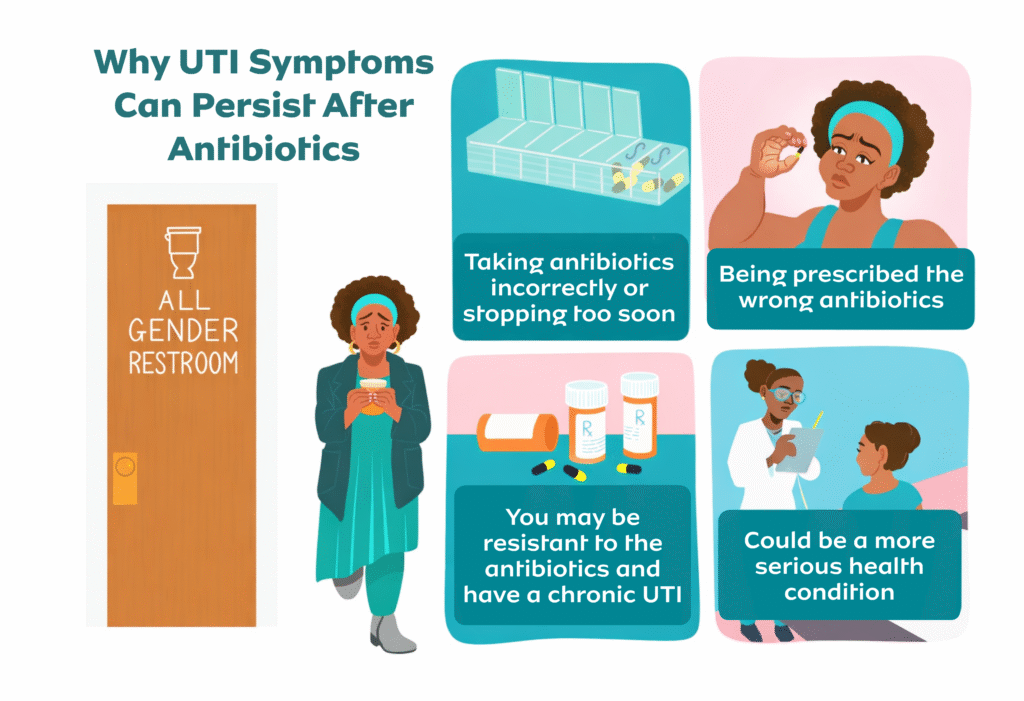

Why UTI Can Persist After Antibiotics

Caregivers play a key role in getting fast, effective treatment. Early action prevents complications and speeds up recovery.

Medical Treatment (First-Line Care)

Doctors treat most UTIs with antibiotics. Start treatment as soon as symptoms appear and follow the full course.

Common options include nitrofurantoin, trimethoprim, and cephalexin

Many people ask, what is best antibiotic for urinary tract infection, the best choice depends on the bacteria and the patient’s history

UTI antibiotics usually begin to relieve symptoms within 24–72 hours

If you’re wondering how long does nitrofurantoin take to work on a UTI, most patients feel improvement within 2–3 days

Caregivers should ensure the patient:

Takes medication exactly as prescribed

Finishes the full course, even if symptoms improve

Reports worsening symptoms immediately

This is the most reliable treatment urinary tract infection approach.

UTI Treatment at Home (Supportive Care)

Home care supports recovery but does not replace antibiotics for most infections.

Encourage plenty of fluids (water helps flush bacteria)

Promote regular urination (do not hold urine)

Maintain proper hygiene

Ensure adequate rest

Many caregivers search for UTI treatment at home or how to treat a UTI naturally. While these steps help, they do not cure most infections alone.

Common Questions Caregivers Ask

Can a UTI heal on its own?

Mild cases may improve, but most require antibiotics to prevent complications

How to get rid of a UTI in 24 hours?

There is no guaranteed way, fast treatment reduces symptoms, but full recovery takes a few days

How to get rid of cystitis fast?

Start antibiotics early, stay hydrated, and rest

Water infection tablets:

Over-the-counter products may relieve symptoms, but do not replace proper urine infection treatment

Caregivers should always prioritize early medical care. Quick action reduces the risk of the infection spreading and helps patients recover safely.

Some patients face a higher risk of complications from a urinary tract infection. Caregivers must act faster and monitor symptoms more closely in these situations.

Elderly Patients

Older adults may not show typical UTI symptoms. Instead, they may develop:

Confusion or sudden changes in behavior

Increased weakness or falls

Loss of appetite

Do not assume these signs are “normal aging.” A UTI can quickly worsen without obvious urinary symptoms.

UTI in Pregnancy

A UTI in pregnancy requires immediate attention. Even mild symptoms can lead to serious complications, including kidney infection or premature labor.

Caregivers should:

Encourage early testing

Ensure prompt treatment

Never delay medical care

Recurrent UTIs

Frequent infections should not be ignored. Many caregivers ask, can recurrent UTIs be a sign of cancer? While this is uncommon, repeated infections can signal underlying issues such as:

Kidney stones

Structural problems in the urinary tract

Chronic bladder conditions

A healthcare provider should always investigate persistent or recurring UTIs.

UTIs in Men

Although less common, male UTI cases often indicate an underlying condition such as prostate enlargement or urinary blockage.

Caregivers should pay attention to:

Persistent symptoms

Difficulty urinating

Recurrent infections

Understanding 10 causes of UTI male (such as poor bladder emptying, catheter use, or prostate issues) helps caregivers recognize when further evaluation is needed.

In all these cases, do not rely on home remedies alone. Early diagnosis, proper treatment urinary tract infection, and close monitoring can prevent serious complications.

Caregivers should not wait when symptoms worsen. A urinary tract infection can escalate quickly, especially when nausea is involved.

Seek urgent care if the person has:

Nausea with vomiting

Fever or chills

Lower back or side pain

Severe weakness or confusion

Inability to keep fluids or medication down

Symptoms that do not improve after starting UTI antibiotics

These signs often indicate a kidney infection or a more serious complication.

Delaying care can allow the infection to spread into the bloodstream (sepsis), which can become life-threatening. Early treatment urinary tract infection reduces this risk and improves recovery outcomes.

Caregiver Tip

If you are unsure, do not guess; get a UTI test done as soon as possible. Testing confirms the infection and helps doctors choose the right urine infection treatment quickly.

Final Thoughts…

So, will a bladder infection cause nausea? Yes, but it often signals that the infection has become more serious or is affecting the kidneys. Caregivers should never ignore this symptom, especially when it appears with fever, vomiting, or back pain.

The key to managing any UTI is early action. Start proper urine infection treatment quickly, monitor symptoms closely, and seek medical care when warning signs appear. While UTI treatment at home can support recovery, it should never replace medical care when symptoms worsen.

Stay alert, act early, and always prioritize safety. Quick decisions and proper care can prevent complications and help patients recover faster.

Need Help Managing UTIs in Your Care Service?

If you want to avoid delayed treatment, worsening symptoms, and preventable complications, expert guidance can make a real difference in how you manage infections like UTIs.

Care Sync Experts supports care providers and caregivers with:

practical guidance on recognising early UTI symptoms

support with infection prevention and care protocols

staff training on managing common conditions like UTIs

clear escalation pathways for high-risk cases

ongoing compliance support aligned with current care standards

We understand how quickly a simple infection can escalate, especially in vulnerable patients, and we help you stay prepared with the right systems and knowledge.

If you want to strengthen your care processes or improve how your team handles infections, speak to our team today.

This guide was prepared by Care Sync Experts and reflects best practices as of 2026. Always seek medical advice from a qualified healthcare professional for diagnosis and treatment.

FAQ

What can be mistaken for a bladder infection?

Several conditions can feel like a bladder infection, including vaginal infections (like yeast infections), sexually transmitted infections (STIs), kidney stones, or interstitial cystitis (a chronic bladder condition). Caregivers should not assume; it’s best to confirm with a proper UTI test to avoid treating the wrong condition.

What is the first stage of a UTI?

The first stage usually begins in the lower urinary tract (bladder or urethra). Early signs include a frequent urge to urinate, mild burning, and discomfort in the lower abdomen. Acting at this stage makes treatment urinary tract infection easier and prevents the infection from spreading.

What not to drink when having a UTI?

Avoid drinks that irritate the bladder, such as caffeine (coffee, tea), alcohol, and sugary or fizzy drinks. These can worsen symptoms and delay recovery. Caregivers should encourage water, which supports effective urine infection treatment.

Can you have a UTI without burning during urination?

Yes, not everyone experiences burning. Some people, especially older adults, may only show symptoms like fatigue, confusion, nausea, or general discomfort. Caregivers should stay alert, as UTIs can present differently depending on the individual.

The Care Quality Commission (CQC) has, since July 1st, 2025, changed how it handles new homecare applications, and the impact has been brutal for unprepared providers.

CQC now routinely returns and rejects incomplete or inaccurate domiciliary care applications at the point of receipt. When that happens, any resubmission counts as a brand-new application. You lose your place in the queue. You start again from the back. In some cases, that mistake adds months to your launch timeline.

This single procedural change in CQC registration for domiciliary care providers explains why so many new CQC domiciliary care applications are failing right now.

The rules did not get easier. CQC raised the bar, deliberately.

Most online guides still teach the old approach:

“Submit what you have and fix issues later.”

“CQC will come back with questions.”

“Minor errors won’t matter.”

That advice is now dangerous.

CQC no longer treats missing documents, outdated forms, or vague answers as fixable issues. They treat them as grounds for immediate rejection.

If your application fails at intake:

CQC does not correct it with you

CQC does not hold your place

CQC applies whatever new requirements exist at resubmission

That last point matters more than people realise. Requirements continue to evolve. A delay today can mean more documents, more scrutiny, and more cost tomorrow.

Why CQC Tightened the Process

Do You Really Need CQC Registration for Supported Living? | 2026 Guide for Providers

CQC did not make this change randomly.

An independent operational review (the Dash review) exposed severe backlogs and inefficiencies. More than half of new provider applications were missing basic information. Some sat unresolved for months. Instead of absorbing that burden, CQC redesigned the process to filter weak applications immediately.

The result is a strict two-stage system:

Initial checks that act as a hard gate

Full assessment only for applications that pass cleanly

We’ll break both stages down in detail later in this guide.

What This Guide Does Differently

This is not a generic overview of CQC registration for domiciliary care providers.

This guide focuses on:

How CQC actually assesses applications today

Where applications fail before assessment even begins

The exact submission mechanics that cause avoidable rejection

The documents, detail, and consistency CQC now expects from day one

If you plan to apply for CQC registration in 2026, read this guide carefully and follow it in order.

Who Needs to Register With CQC for Domiciliary Care?

If you plan to deliver personal care in people’s own homes, the law leaves no room for interpretation. You must register with the Care Quality Commission before you provide any care.

CQC does not assess intentions. They assess what you actually do.

What Counts as Domiciliary Care?

Domiciliary care (also called homecare) involves supporting people in their own homes with tasks they cannot safely do alone. This includes:

Helping with washing or bathing

Assisting with dressing

Supporting eating and drinking

Helping people take medication

Providing personal hygiene support

If your service includes any of these activities, CQC classifies it as personal care, which is a regulated activity under the Health and Social Care Act 2008.

Who Is Legally Required to Register?

You must register if you provide personal care as:

A limited company

A partnership

A sole trader/individual

A charity or non-profit organisation

CQC does not care about your business size. A one-person homecare startup must meet the same registration standard as a multi-branch provider.

Who Does Not Need to Register?

Some providers assume they need registration when they don’t, while others assume the opposite and get it wrong.

You do not need to register with CQC if you only provide:

Domestic help (cleaning, shopping, laundry)

Companionship or social support without personal care

Administrative or care coordination services only

The moment you cross into hands-on personal care, registration becomes mandatory.

What About Managers and Individuals?

CQC registration applies at two levels:

The provider organisation or individual

The registered manager (a separate regulated role)

If you operate alone, you may act as:

the provider

the nominated individual

the registered manager

CQC allows this, but it increases scrutiny. You must clearly explain how you manage governance, accountability, and complaints when one person holds multiple roles. We’ll cover this in detail later.

Operating Without Registration Is an Offence

Providing regulated care without registration is not a minor breach. It is a criminal offence.

CQC has enforcement powers that include:

prosecution

fines

enforcement notices

long-term impact on future registration attempts

If you plan to offer personal care, you should not market, recruit staff, or accept clients until CQC confirms your registration.

Quick Self-Check: Do You Need to Register?

You need CQC registration now if:

You will help people wash, dress, eat, or take medication

You advertise personal care services

You employ or plan to employ care workers for personal care

If any of these apply, registration is not optional.

Registering With CQC as an Individual (Sole Trader)

Registering with the Care Quality Commission as an individual is legal, common, and fully permitted. However, it is not the easier option, despite what many people assume.

CQC applies the same regulatory standards to individual providers as it does to limited companies. In practice, individual applicants often face closer questioning, not less.

What Stays the Same

If you register as an individual rather than a company, these requirements do not change:

Personal care remains a regulated activity

You must meet all fundamental standards

You must submit the same core supporting documents

You must demonstrate safe care, governance, and financial sustainability

CQC does not lower expectations because you are a sole trader.

What Changes for Individual Providers

Where things differ is how CQC evaluates responsibility and oversight.

When you register as an individual:

You become the legal provider

You carry personal accountability for compliance

CQC expects clear evidence of how you manage risk, quality, and decision-making

If you also act as the registered manager, CQC will examine how you separate:

operational delivery

governance oversight

complaints handling

You must show that one person can realistically manage all three without conflicts of interest.

The Governance Challenge (Where Many Applications Fail)

CQC often rejects individual applications because governance is poorly explained.

Common weak answers include:

“I will manage everything myself”

“I will deal with complaints if they arise”

“I will monitor quality regularly”

These statements say nothing about how you will do those things.

As an individual provider, CQC expects you to explain:

how you audit care quality

how you identify risks

how you act on feedback

how complaints about you are handled independently

If you cannot show this clearly in your governance and complaints policies, your application is unlikely to pass.

Individual vs Limited Company: Practical Differences

Choosing to register as an individual affects more than paperwork.

Individual registration means:

You carry personal liability

You rely heavily on your own experience and competence

You must demonstrate credibility without a wider management structure

Limited company registration allows:

clearer separation of governance and operations

easier delegation as the service grows

stronger perception of sustainability for CQC assessors

CQC does not tell you which route to choose, but it does assess whether your chosen structure makes sense for the service you propose.

When Individual Registration Makes Sense

Registering as an individual may be appropriate if:

You have strong prior care management experience

You plan to run a small, local service initially

You fully understand the compliance burden

You can clearly explain governance arrangements

If you lack experience or plan rapid growth, individual registration often creates avoidable risk.

How CQC Processes New Domiciliary Care Applications in 2026

The biggest mistake new providers make is assuming CQC registration works the way it did a few years ago.

It doesn’t.

On 1 July 2025, the Care Quality Commission fundamentally changed how it processes new domiciliary care applications. That change still governs approvals in 2026.

The Old Assumption (Now Wrong)

Before mid-2025, many applicants believed:

CQC would flag missing documents later

Minor errors could be corrected during assessment

Applications stayed in the queue while issues were fixed

That approach no longer applies.

The New Reality

CQC now applies strict intake controls.

When your application arrives, CQC first checks whether:

every required document is present

all forms are current and fully completed

the information is accurate and internally consistent

If anything fails at this point, CQC returns or rejects the application immediately.

There is no partial acceptance. There is no “we’ll fix this later.”

Why Resubmission Is So Risky

If CQC rejects your application at intake:

you must correct the issues

you must resubmit everything

CQC treats the resubmission as a new application

That means:

you lose your original place in the queue

your timelines reset

any new requirements introduced meanwhile apply to you

In practical terms, one missing document can delay your launch by months.

Why CQC Made the Process Stricter

CQC tightened the system after an operational review revealed widespread problems:

high volumes of incomplete applications

long processing delays

assessors spending time chasing basic information

Instead of absorbing that inefficiency, CQC redesigned the process to filter out weak or unprepared applications immediately.

This protects their resources, and shifts the burden onto providers to submit complete, assessment-ready packs from day one.

What This Means for You

CQC no longer rewards “good enough” submissions.

To succeed in 2026, your CQC domiciliary care application must:

arrive complete

follow current guidance exactly

include documents that meet minimum requirements

show consistency across every form and policy

If your pack does not meet those standards at intake, CQC will not progress it.

That is why preparation now matters more than speed.

The Two-Stage CQC Domiciliary Care Application Process

Every CQC domiciliary care application now passes through two distinct stages. Each stage has a different purpose, and a different failure risk.

Understanding the difference is essential if you want to register successfully.

1. Stage One: Initial Checks (Where Most Applications Fail)

Stage One is not an assessment of care quality. It is a gatekeeping exercise.

When the Care Quality Commission receives your application, they first check whether it is complete, current, and assessable.

At this stage, CQC looks for one thing only: Can this application move forward without further clarification?

What CQC Checks at Stage One

CQC will confirm that:

All required application forms are included

Every form uses the latest version

All sections of every form are fully completed

All required supporting documents are attached

Documents meet minimum content requirements

Information is consistent across forms and policies

This is a strict yes-or-no decision.

If even one required document is missing, or one form uses an outdated version, CQC will reject the application.

What Stage One Is Not

CQC does not:

review care quality in depth

interview your manager

assess how well your policies work in practice

That comes later.

Stage One exists to filter out incomplete or poorly prepared submissions.

Why Applications Fail at Stage One

Most rejections at this stage happen because of:

Missing supporting documents

Incorrect or outdated forms

Blank fields or vague answers

Generic policies that lack required detail

Contradictions between documents

Email submission errors

CQC will usually email you to explain why your application was rejected, but by then the damage is done.

If you resubmit, CQC treats it as a new application.

Stage One Pass Checklist (Use This Before You Submit)

Your application should pass Stage One if:

Every required document is included

Every form is current and fully completed

No answers are left blank

Policies reflect your actual service model

Your Statement of Purpose, business plan, and policies align

File names are clear and organised

All documents are submitted together

If you cannot confidently tick all of these, do not submit yet.

2. Stage Two: Full Assessment (Where CQC Tests Your Readiness)

Only applications that pass Stage One move to Stage Two.

Stage Two is where CQC evaluates whether you are fit to provide safe, effective, and well-led care.

This is a detailed assessment, not a tick-box exercise.

What CQC Assesses at Stage Two

During full assessment, CQC will review:

Your supporting documents in detail

Your understanding of the fundamental standards

Your governance and quality assurance systems

Your safeguarding arrangements

Your recruitment and training processes

Your financial sustainability

Your ability to manage risk and respond to incidents

CQC may also:

request additional information

conduct a registration interview

arrange a premises visit to your office base

The Registration Interview

CQC often interviews the registered manager and sometimes the nominated individual.

They expect you to:

explain how your policies work in practice

demonstrate understanding of safeguarding and medicines management

show how you monitor quality and learn from issues

answer confidently without contradicting your documents

CQC does not expect perfection, but they do expect competence and honesty.

Premises Visits for Homecare Providers

Even though care takes place in people’s homes, CQC may visit your registered office base.

They will check:

health and safety arrangements

secure storage of records

readiness to operate

evidence of legal occupancy

If your premises are not ready when visited, CQC may refuse your application.

Why Stage Two Takes Time

Stage Two can take several months. CQC assesses risk carefully and may handle many applications at once.

You must:

respond quickly to information requests

monitor your email daily

keep your documents consistent

CQC may give you only a few days to respond to requests. Delays or incomplete responses can stall or damage your application.

In Short…

Stage One decides whether CQC will even assess you. Stage Two decides whether you are fit to provide care.

Most providers focus too much on Stage Two and underestimate Stage One. In 2026, Stage One is where most applications fail.

Documents Required for CQC Registration (2026 Homecare Pack)

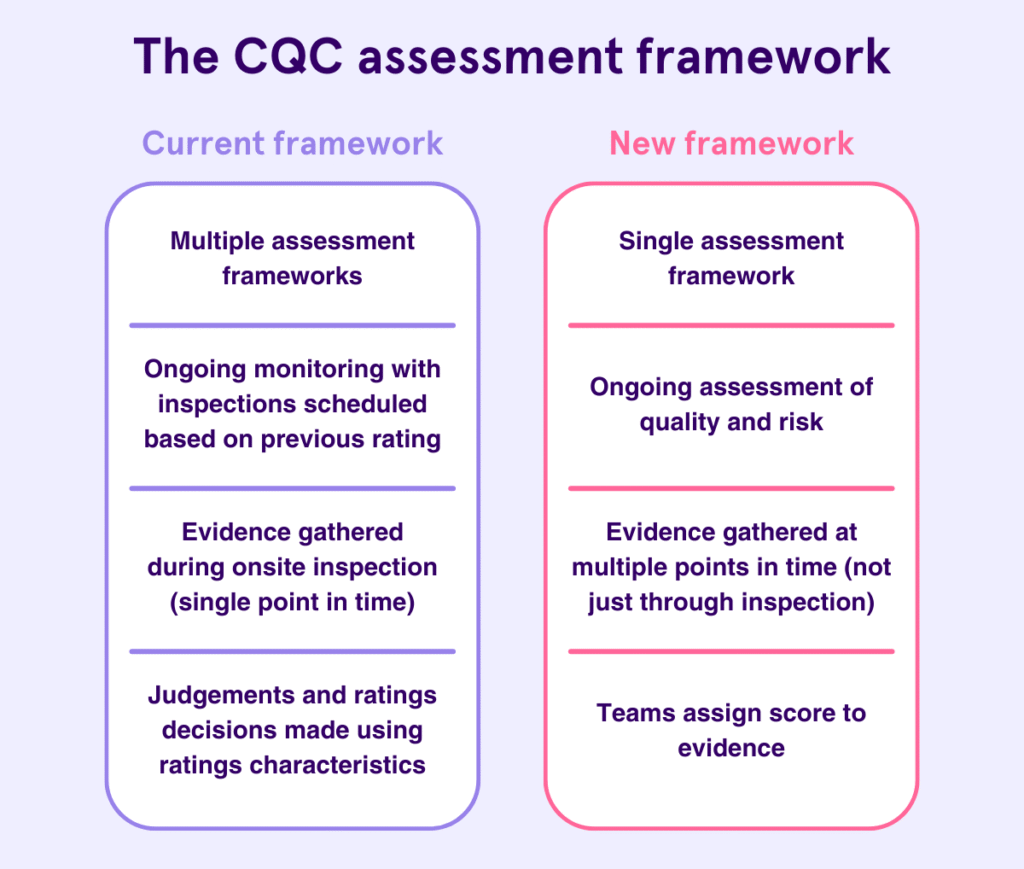

CQC Assessment Framework

CQC does not reject domiciliary care applications because providers lack good intentions. They reject them because documents are missing, weak, inconsistent, or unassessable.

If your document pack does not meet minimum requirements, the Care Quality Commission will return your application before assessment begins.

This section explains exactly what you must submit, and what CQC expects to see inside each document.

Core Documents Required for All Providers

Every provider applying for CQC registration must submit the following. There are no exceptions.

Statement of Purpose

Your Statement of Purpose defines your service. CQC cross-checks it against every other document.

It must clearly explain:

the regulated activities you will provide

who you will support

where services will be delivered

how care will be delivered

CQC expects this document to be:

service-specific

current

consistent with your business plan and policies

If your Statement of Purpose describes services your policies do not support, your application will fail.

DBS Checks

You must provide enhanced DBS checks for:

the provider (if an individual)

the nominated individual

the registered manager

DBS certificates must:

be countersigned where required

be less than 12 months old at submission

Start DBS applications early. Delays here stall entire applications.

Insurance Evidence

You must submit evidence of:

public liability insurance

employer liability insurance (if you will employ staff)

CQC only accepts one insurance document. If you require both types, you must complete the CQC liability insurance supporting information form and include your certificates.

Expired or incorrect insurance evidence leads to rejection.

Additional Documents Required for Domiciliary Care Providers

If you are registering to provide personal care, CQC requires additional service-specific documents.

These are non-negotiable.

Additional Information for Providers of Personal Care (Form)

This form is mandatory for homecare providers.

CQC uses it to assess:

how you recruited key personnel

how you assessed competence

whether genuine local demand exists for your service

Weak answers here often expose:

lack of market research

unrealistic service plans

governance gaps

Treat this form as an assessment tool, not an admin exercise.

Business Plan (With Financial Forecast)

Your business plan must demonstrate that your service is viable and sustainable.

CQC expects:

clear service model explanation

evidence of local market demand

realistic staffing plans

a one-year financial forecast

a SWOT analysis

Vague statements like “there is demand for care services” will not pass. CQC expects evidence, not assumptions.

Evidence of Legal Occupancy

You must prove you have permission to operate from your registered address.

Acceptable evidence includes:

title deeds (if you own the property)

tenancy or licence agreement

written permission from landlord or mortgage provider

This applies even if you operate from home. Missing or unclear occupancy evidence is now a common rejection reason.

Staff Training Plan

CQC no longer accepts a simple training matrix.

Your training plan must explain:

induction training

mandatory training

refresher schedules

specialist training where required

support for overseas workers

who delivers the training

CQC wants to see how training works in practice, not just a list of topics.

Service User Guide

This document explains your service to people who use it.

It must cover:

what services you offer

pricing and charges

safeguarding information

how to raise concerns or complaints

If this document reads like marketing copy instead of practical guidance, CQC will challenge it.

Policies Required for All Home Care Providers

CQC requires a specific policy set. Each policy must reflect how your service actually operates.

You must submit policies covering:

consent

equality, diversity and human rights

governance

infection prevention and control

medicines management

recruitment

safeguarding

complaints

Generic templates often fail because they:

describe services you do not provide

contradict your Statement of Purpose

lack sufficient operational detail

CQC cross-checks policies line by line. Inconsistencies trigger rejection.

Minimum Requirements: What CQC Means by “Assessable”

CQC’s guidance is clear. Documents must include enough detail to be assessed.

That means:

no placeholders

no blank sections

no copied text that does not apply to your service

no contradictions between documents

If an assessor cannot understand how your service will operate, your application does not progress.

Final Document Pack Self-Check

Before submission, confirm that:

every required document is included

every document reflects your service model

all documents agree with each other

all documents use current terminology

nothing relies on “we will decide later”

If any document fails this test, fix it before you submit.

CQC Application Form for New Providers: What to Prepare Before You Fill It In

Many domiciliary care applications fail before CQC reads a single policy.

The problem is not the documents. The problem is the CQC application form for new providers.

The Care Quality Commission uses this form as the master reference point. Assessors cross-check everything else against it. If the form contains vague answers, missing detail, or contradictions, CQC rejects the application at Stage One.

Do Not Start the Form Until These Decisions Are Final

Before you touch the application form, you must lock down the following:

Regulated activity For homecare agencies, this is usually personal care. Do not list activities you are not ready to deliver.

Service model Who you will support, how you will deliver care, and what you will not provide.

Registered location Your office base address must be final and supported by legal occupancy evidence.

Key roles Who is the provider, nominated individual, and registered manager, and whether any roles overlap.

If any of these points remain undecided, stop. Incomplete thinking here leads to rejection later.

How CQC Reads Your Application Form

CQC does not read the form in isolation.

Assessors compare it against:

your Statement of Purpose

your business plan

your policies and procedures

the additional personal care form

If your form says one thing and your documents say another, CQC assumes you do not understand your own service.

That is a red flag.

Common Form Errors That Trigger Rejection

CQC regularly rejects applications because the form includes:

Blank fields Every question must be answered. If something does not apply, state “Not applicable” and explain why.

Vague language Phrases like “we will ensure”, “we plan to”, or “we intend to” without explanation show lack of readiness.

Overly broad services Listing services you cannot evidence through policies, training, or staffing.

Inconsistent answers For example, describing a small, local service in one section and a large multi-area operation in another.

Outdated assumptions Using terminology or processes that no longer reflect current CQC expectations.

Each of these issues can stop your application before assessment begins.

How to Write Strong Answers (What CQC Expects)

Strong answers are:

specific

consistent

evidence-backed

Instead of writing:

“We will provide high-quality care tailored to individual needs.”

Write:

“We will deliver personal care to adults in their own homes within [location], following care plans developed after initial assessment and reviewed monthly.”

Clarity beats ambition every time.

The “Cross-Check Rule” (Use This Before Submission)

Before you submit the application form, cross-check each answer against:

your Statement of Purpose

your business plan

your policies

If any answer cannot be supported by a document, revise it.

CQC assumes:

If it is written in the form, you must already be able to deliver it.

Final Form Readiness Checklist

Your application form is ready when:

every field is completed

no answers rely on future decisions

language matches your documents exactly

service scope is clear and realistic

roles and responsibilities are consistent

If you rush this stage, CQC will return your application, and you will lose your place in the queue.

How to Apply for CQC Registration (Submission Mechanics That Make or Break You)

What is CQC Registration?

Many providers prepare strong documents and still fail because they submit their CQC domiciliary care application incorrectly.

At this stage, CQC does not troubleshoot. If your submission does not meet their technical requirements, your application may never reach assessment.

You must email your complete application bundle to:

HSCA_Applications@cqc.org.uk

CQC requires email submission for new provider applications. This is not optional.

The 10MB Email Size Rule (Non-Negotiable)

CQC can only receive emails up to 10MB in size.

This includes:

all attachments

the email body

embedded signatures

If your email exceeds 10MB:

CQC may not receive it at all

you may not get a bounce-back warning

your application may be treated as missing

If your application exceeds 10MB, you must split it into multiple emails.

Correct Subject Line Format (Critical for Multi-Email Submissions)

When sending more than one email, CQC requires a specific subject line format so they can match your documents correctly.

Use this format exactly:

[Provider Name] new provider application 1/2 [Provider Name] new provider application 2/2

If you send three emails, use 1/3, 2/3, 3/3.

If you do not follow this format:

emails may not be linked together

CQC may treat your application as incomplete

your application may be rejected at intake

This is one of the most common and avoidable failures.

All Documents Must Arrive Together

CQC requires that all documents arrive at the same time.

You cannot:

send the application form today

send policies tomorrow

send missing documents next week

If anything is missing from the initial submission, CQC will return or reject the application.

When you resubmit, it counts as a new application.

File Naming and Organisation (Make Review Easy)

CQC assessors review large volumes of applications. Clear organisation helps your application move smoothly.

Use:

separate files for each document

clear, descriptive file names

consistent terminology across documents

Good example:

Statement of Purpose – Oxtown Care Ltd.pdf

Safeguarding Policy – Domiciliary Care.pdf

Business Plan – Homecare Services.pdf

Avoid:

vague names like “Policy 1”

merged documents containing multiple policies

zipped folders unless absolutely necessary

Assessors must be able to locate documents quickly.

What to Include in the Email Body

Keep the email body simple and factual.

Include:

provider name

confirmation that this is a new provider application

number of emails being sent (if applicable)

Do not include explanations, justifications, or attachments that are not required.

Submission Day Checklist (Use This Before You Click Send)

Before submitting, confirm that:

All required documents are attached

All forms use the latest versions

File names are clear and consistent

Total email size is under 10MB

Subject line format is correct

All emails are ready to send together

If any item is missing, stop and fix it first.

After You Submit: What to Do Next

After submission:

save sent emails and attachments

keep a copy of everything submitted

monitor your inbox daily

CQC may contact you quickly if there is an issue. Delayed responses can slow your application or affect assessment.

Note: Strong documents mean nothing if CQC cannot process your submission.

Follow the submission mechanics precisely. Treat this step with the same seriousness as the documents themselves.

Why CQC Rejects Domiciliary Care Applications (And How You Prevent It)

Most failed applications do not fail because providers lack experience or commitment. They fail because applicants underestimate how precise and unforgiving the Care Quality Commission has become.

Below are the rejection reasons we see most often, and exactly how to avoid each one.

Rejection Reason 1: Missing Documents

This is the single biggest cause of rejection. If even one required document is missing, CQC will return or reject your application at intake.

How to prevent it

Use a master document checklist before submission

Confirm every required document is attached

Do not assume CQC will “ask for it later”

CQC will not chase missing documents anymore.

Rejection Reason 2: Using Outdated Forms

CQC updates application forms periodically. Submitting an old version triggers immediate rejection.

This includes:

provider application forms

manager application forms

additional personal care forms

How to prevent it

Download every form directly from the CQC website immediately before completing it

Never reuse forms from old applications or third-party packs

If the form version is wrong, nothing else matters.

Rejection Reason 3: Incomplete or Vague Form Answers

Leaving fields blank or providing vague responses signals unreadiness.

CQC does not accept:

empty fields

“to be confirmed” answers

generic statements without explanation

How to prevent it

Answer every field

If something does not apply, state “Not applicable” and explain why

Replace vague language with specific operational detail

CQC interviews assess judgement, not just knowledge.

Interview Readiness Checklist

You are ready if you can:

explain your service model clearly

describe safeguarding processes confidently

walk through recruitment and training steps

explain how you monitor quality

discuss complaints handling realistically

If you cannot explain it verbally, CQC will question whether you can deliver it in practice.

After You Get Registered: What Happens Next (and How to Stay Inspection-Ready)

Once the Care Quality Commission grants registration, you can legally begin providing domiciliary care. But approval does not come with a grace period.

From day one, CQC expects you to operate exactly as described in your application.

What Changes Immediately After Registration

As soon as registration is confirmed:

You can start delivering regulated personal care

You become liable for annual CQC fees

You must comply fully with the regulations

Your service becomes eligible for inspection

CQC assumes that everything you described on paper is already in place and working.

Your First Inspection: What to Expect

CQC usually inspects new domiciliary care providers within the first 12 months of registration. However, inspections can happen sooner if CQC identifies risk.

Inspections focus on the five key questions:

Is the service safe?

Is it effective?

Is it caring?

Is it responsive?

Is it well-led?

Inspectors will test whether your service matches your registration documents in practice.

The First 30 Days: What You Should Do Immediately

The first month after registration sets the tone for inspection readiness.

You should:

implement all policies and procedures in real operations