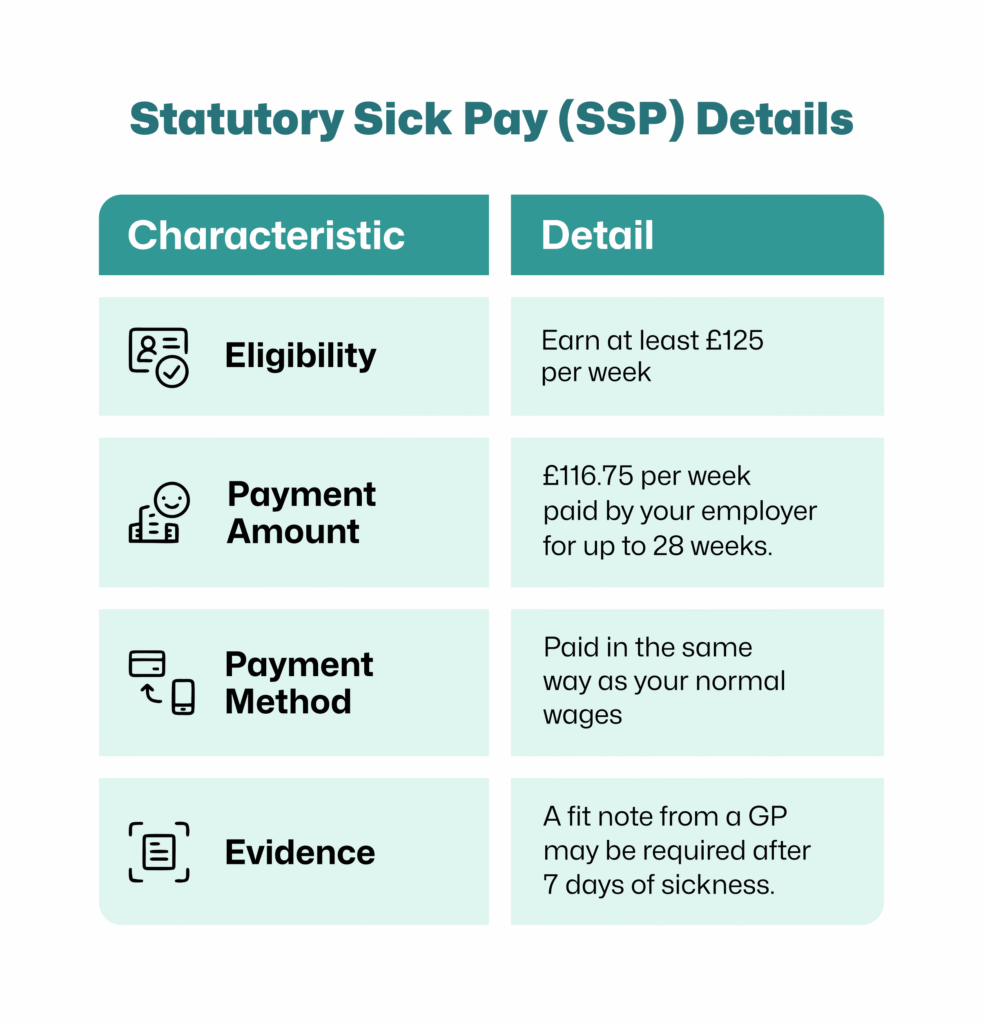

The SSP rate (Statutory Sick Pay) in the UK is £123.25 per week as of 6 April 2026, or 80% of an employee’s average weekly earnings (whichever is lower). Employers must pay SSP for up to 28 weeks, starting from the first qualifying day of sickness absence.

In simple terms, if you’re asking “how much is statutory sick pay?” or “how much is SSP?”, the legal minimum most employers must pay eligible staff is £123.25 per week, processed through normal payroll with tax and National Insurance deductions.

Key Takeaways

- The SSP rate in 2026 is £123.25 per week (or 80% of earnings if lower)

- Employers pay SSP for up to 28 weeks

- SSP now starts from the first qualifying day (no waiting days)

- There is no minimum earnings threshold after April 2026

- SSP forms part of the UK’s minimum sick pay entitlement

- Employers can offer more through private sick pay or enhanced schemes

Why SSP Is Important for Caregiver Businesses

SSP directly affects how you run and sustain a caregiver business. If you manage a domiciliary care agency or care home, staff absence is not just an HR issue, it impacts service delivery, compliance, and profitability.

Care work depends heavily on consistent staffing. When a caregiver calls in sick, you must:

- find cover quickly

- maintain safe staffing ratios

- continue delivering care without disruption

That creates immediate pressure on your team and your margins.

Staffing Pressure and Cost Impact

From April 2026, SSP starts from the first day of sickness absence, which means costs begin immediately. For caregiver businesses with:

- part-time workers

- zero-hour contracts

- high staff turnover

SSP payments will occur more frequently than before. This makes long-term sick pay planning essential, especially if multiple staff members are off at the same time.

Compliance Risk for Care Providers

Care businesses operate in a regulated environment. If you fail to meet sick pay entitlement rules, you risk:

- payroll errors

- HMRC penalties

- reputational damage

You must apply SSP correctly and consistently across your workforce.

Real Impact on Care Delivery

Unlike many industries, you cannot “pause” operations. If a caregiver is absent:

- clients still need support

- visits must continue

- regulators expect continuity of care

This makes SSP more than just a payroll obligation; it becomes part of your operational strategy.

In short, understanding SSP is not optional for care providers. It directly affects staff stability, compliance, and business performance.

RELATED: Earned Income Disallowance: Benefits & Allowances (2026 Guide)

SSP Rate UK: How Much Is Statutory Sick Pay in 2026?

The SSP rate UK for the 2026/27 tax year is £123.25 per week, or 80% of an employee’s average weekly earnings, whichever is lower.

If you’re asking “how much is SSP?” or “how much is statutory sick pay?”, this is the legal minimum you must pay eligible employees when they are off sick.

What Employers Must Know

- Weekly SSP rate: £123.25

- Alternative calculation: 80% of average weekly earnings (if lower than £123.25)

- Maximum duration: 28 weeks per period of sickness

- Payment method: Through payroll, with tax and National Insurance deducted

You must pay SSP in the same way you pay wages, on your employee’s normal payday.

What This Means for Caregiver Businesses

For care providers, the SSP rate sets the baseline cost of staff absence. Even if a caregiver works limited hours, you must still calculate SSP correctly based on their average earnings and qualifying days.

Most employees will receive the full £123.25 per week, but lower-paid or part-time staff may receive less if 80% of their earnings falls below the standard SSP rate.

This makes it critical to understand not just the headline number, but how SSP applies across different types of care staff in your workforce.

READ MORE: Scotland PIP ADP Update 2026: What Care Businesses and Claimants Must Know

How Much Is SSP Per Day? (With Example)

SSP is not paid as a flat daily amount. You must calculate the daily rate based on how many qualifying days an employee usually works each week.

If you’re asking “how much is SSP per day?” or “how much is statutory sick pay per day?”, the answer depends on the employee’s work pattern.

How Daily SSP Is Calculated

You calculate the daily rate using this formula:

Daily SSP = Weekly SSP rate ÷ Number of qualifying days

- Weekly SSP rate (2026): £123.25

- Qualifying days: the days the employee normally works

Example (Caregiver Working 5 Days a Week)

- Weekly SSP: £123.25

- Qualifying days: 5

£123.25 ÷ 5 = £24.65 per day

So, you would pay £24.65 for each sick day the employee qualifies for.

Why This Matters for Care Providers

Caregiver schedules vary widely:

- some staff work 2–3 days per week

- others work full-time shifts

- some work rotating or weekend patterns

This means SSP daily rates will differ across your workforce.

You must calculate SSP individually for each employee based on:

- their contract

- their working pattern

- their qualifying days

Getting this wrong can lead to underpayment, disputes, or compliance issues.

Always base your calculation on the employee’s actual working schedule, not a standard 5-day assumption.

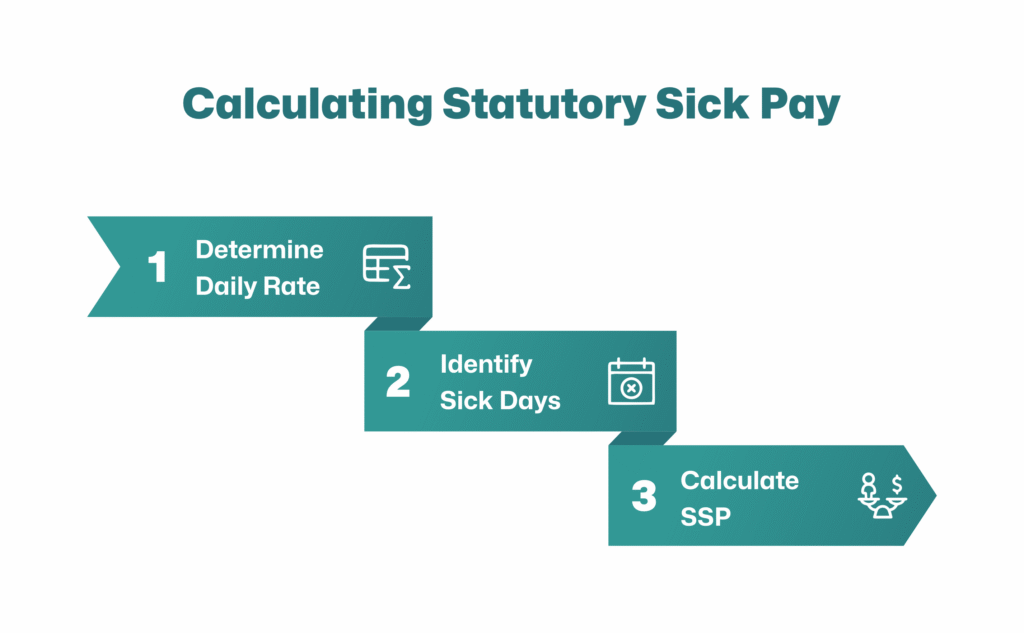

SSP Calculator UK: How to Calculate Sick Pay

You don’t need complex software to calculate SSP correctly. You can follow a simple process or use an SSP calculator UK tool to speed things up.

If you’re managing multiple caregivers, using a statutory sick pay calculator or sick pay calculator helps reduce errors and saves time.

Simple Step-by-Step Method

Use this method for every employee:

- Confirm eligibility

Check that the employee qualifies for SSP (employed, reported sickness, at least one full working day off). - Work out average weekly earnings

Calculate earnings over the relevant period (usually 8 weeks). - Apply the SSP rate

Use:- £123.25 per week, or

- 80% of average weekly earnings (whichever is lower)

- Identify qualifying days

Count how many days the employee normally works each week. - Calculate daily rate

Divide the weekly amount by qualifying days. - Pay through payroll

Process SSP like wages, including tax and National Insurance.

When to Use an SSP Calculator

An SSP calculator becomes useful when:

- staff work irregular shifts

- earnings vary week to week

- you manage a large care team

Many employers search for:

- SSP calculator UK

- ssp rate uk calculator

- statutory sick pay calculator

These tools help you avoid manual errors, especially in busy care environments.

Practical Tip for Caregiver Businesses

Do not rely on assumptions. Always calculate SSP based on:

- actual earnings

- real working patterns

Even small mistakes, especially across multiple staff, can lead to payroll inaccuracies and compliance risks.

If you run a care agency, standardising your calculation process (or using a calculator tool) will save time and protect your business.

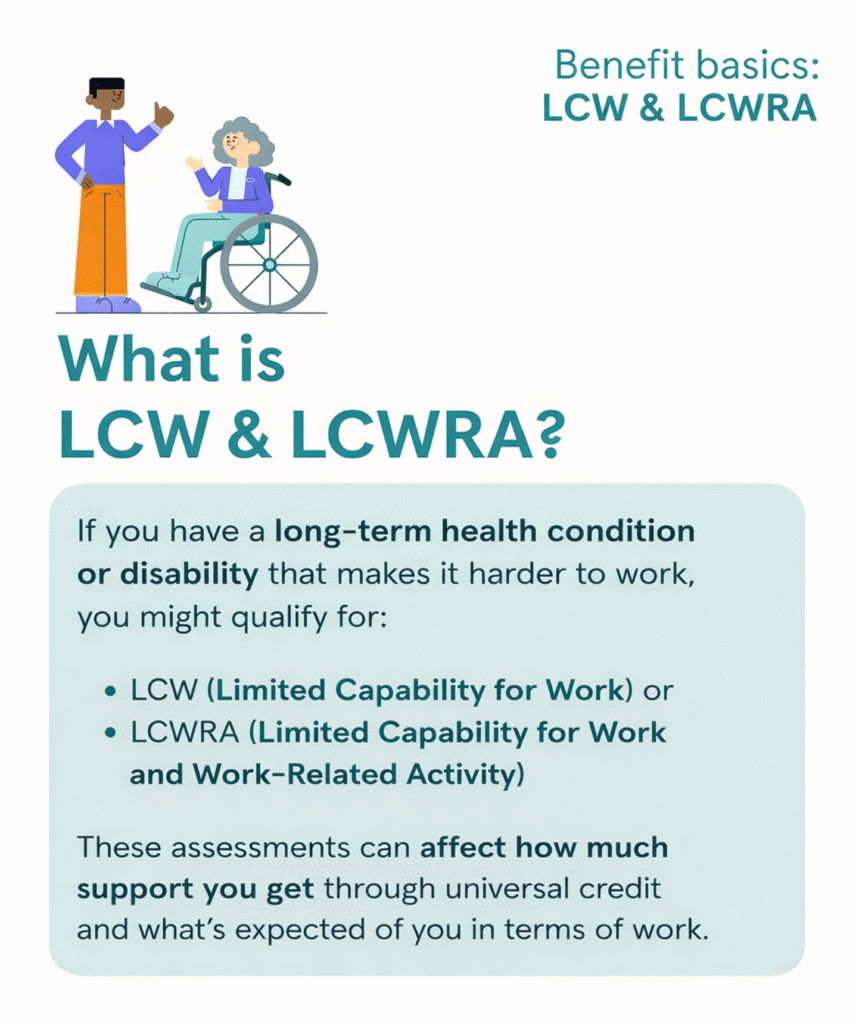

SEE ALSO: What is the Work Capability Assessment? 2026 Update for Care Businesses

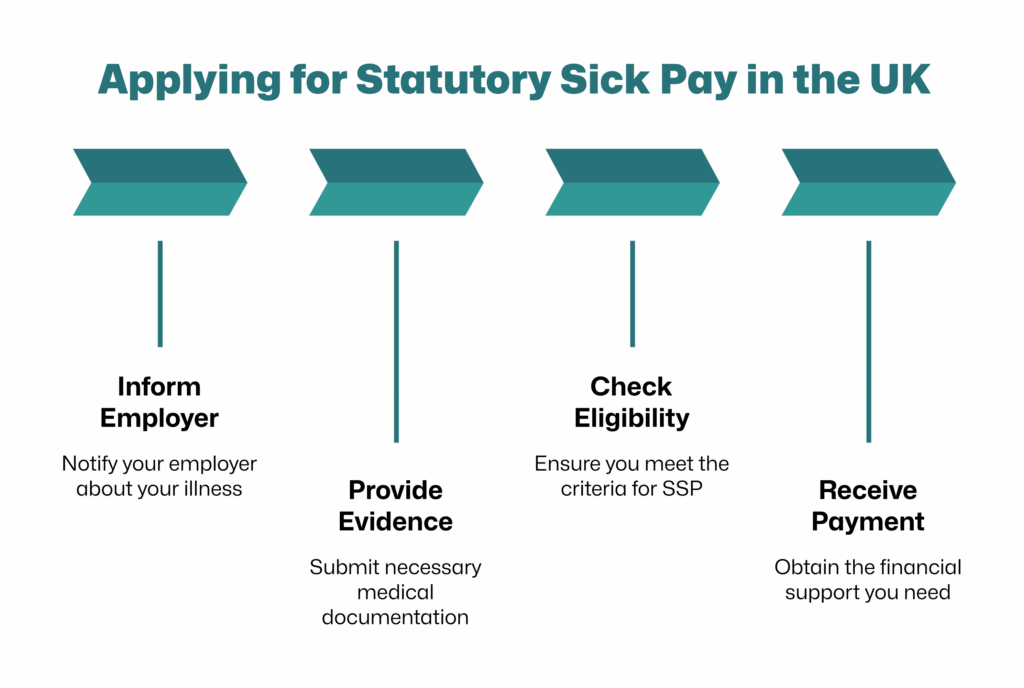

SSP Entitlement UK: Who Qualifies After April 2026 Changes

SSP entitlement UK rules expanded in April 2026, which means more care workers now qualify for statutory sick pay.

If you manage a caregiver workforce, you must understand exactly who qualifies to apply the correct sick pay entitlement.

Who Qualifies for SSP in 2026

An employee qualifies for SSP if they:

- Have an employment contract

- Have started work under that contract

- Are off sick for at least one full working day

- Follow your sickness reporting process (or notify within 7 days)

SSP now applies regardless of income level, following the removal of the Lower Earnings Limit.

What Changed in April 2026

Two major changes affect caregiver businesses:

- No minimum earnings threshold

Even low-paid or part-time care staff now qualify - No waiting days

SSP starts from the first qualifying day of sickness

This means more employees will receive SSP, more often

What This Means for Care Providers

In care settings, many staff:

- work part-time

- work flexible shifts

- earn variable income

Before 2026, some of these workers did not qualify. Now, most will qualify

This increases:

- your payroll exposure

- the importance of accurate absence tracking

Important Clarification

Not every absence automatically qualifies.

You must still confirm:

- the employee was scheduled to work that day

- they were fully absent (not partially worked)

SSP entitlement depends on actual working patterns, not assumptions.

Practical Tip

Create a clear internal checklist for SSP eligibility.

This helps your HR or admin team apply rules consistently across all caregivers.

In a care business, consistency protects you from disputes, errors, and compliance issues.

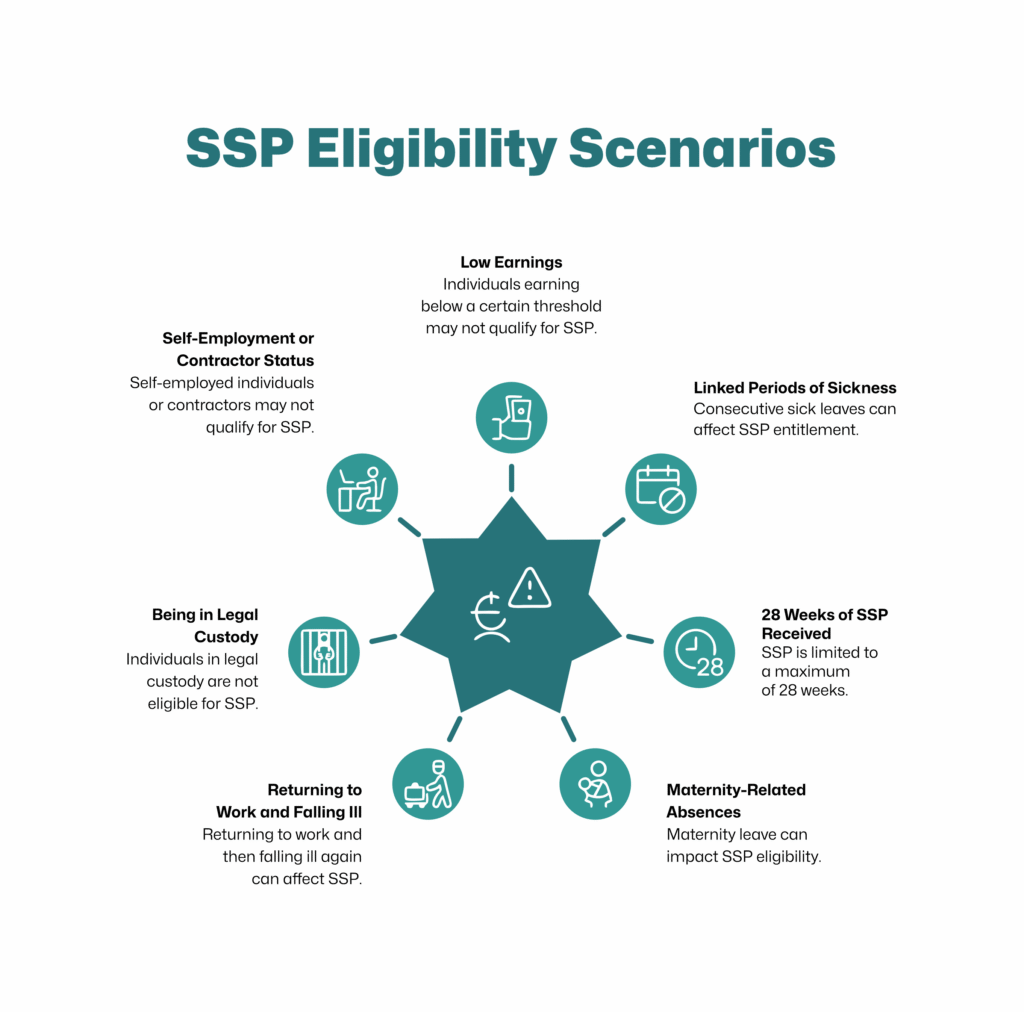

Who Does NOT Qualify for SSP

Not every worker qualifies for Statutory Sick Pay. As a caregiver business, you must identify non-eligible cases early to avoid overpaying or making incorrect payroll decisions.

Employees Who Do Not Qualify

An employee does not qualify for SSP if they:

- Have already received the maximum 28 weeks of SSP

- Are receiving Statutory Maternity Pay or Maternity Allowance

- Are off sick due to a pregnancy-related illness in the 4 weeks before the due date

- Were in custody or on strike on the first day of sickness

- Work outside the UK and are not liable for UK National Insurance

- Recently received Employment and Support Allowance (ESA) within certain conditions

These rules still apply even after the 2026 changes.

What About Self-Employed Workers?

Self-employed individuals do not qualify for SSP.

If you’re wondering about:

- self employed sick pay

- sick pay for self employed

The answer is simple: SSP only applies to employees, not self-employed contractors.

Self-employed caregivers must rely on:

- personal savings

- insurance

- government benefits (e.g., Universal Credit or ESA, if eligible)

Common Mistake Care Providers Make

Some care businesses incorrectly assume all staff qualify, especially when using:

- agency workers

- freelance caregivers

- zero-hour arrangements

Always confirm employment status before applying SSP.

Practical Tip for Care Businesses

Before paying SSP, check:

- employment status

- SSP already paid (28-week limit)

- reason for absence

A quick check upfront prevents overpayment, payroll errors, and compliance issues later.

MORE: What is a Discretionary Housing Payment? 2026 Update for Care Business

SSP1 Form Explained: When You Must Give It to Employees

The SSP1 form is a legal document you must provide when an employee cannot receive SSP or when their SSP is about to end.

As a caregiver business, issuing this form at the right time is critical. It allows your employee to apply for alternative financial support.

When You Must Issue an SSP1 Form

You must give an employee an SSP1 form if:

- They do not qualify for SSP

- Their SSP is about to end before they return to work

- Their SSP has ended unexpectedly while still sick

Deadlines You Must Follow

- If SSP ends unexpectedly → within 7 days

- If SSP is expected to end → by week 23 of absence

- If employee never qualified → within 7 days of first sick day

Missing these deadlines can lead to compliance issues and employee complaints

Why the SSP1 Form Matters

The SSP1 form allows employees to apply for:

- Employment and Support Allowance (ESA)

- Universal Credit

Without it, they may face delays in receiving financial support.

What This Means for Care Providers

In caregiving businesses:

- long-term sickness is common

- staff may reach the 28-week SSP limit

You must track absence carefully so you can issue the SSP1 form on time.

Practical Tip

Set a reminder system for:

- week 20–23 of long-term sickness cases

This ensures your admin team:

- prepares the SSP1 form early

- avoids last-minute errors

Good tracking protects both your business and your employees.

Fit Notes and Sick Notes: What Employers Can Ask For

As a caregiver business, you must handle sickness evidence correctly. You cannot demand medical proof too early, and you must follow clear rules around fit notes (often called sick notes).

What Happens in the First 7 Days

For the first 7 calendar days of sickness:

- The employee can self-certify their illness

- You cannot require a fit note

- You should record the absence internally

Many people refer to this loosely as a “sick note” (ss note), but no formal medical note is required at this stage.

After 7 Days: Fit Notes Required

If the employee is off sick for more than 7 days:

- You can request a fit note

- It must come from an approved healthcare professional:

- GP or hospital doctor

- Registered nurse

- Pharmacist

- Physiotherapist

- Occupational therapist

Fit notes can be:

- digital

- printed

Types of Fit Notes

A fit note will usually state:

- “Not fit for work”

- or

- “May be fit for work” (with adjustments)

If it suggests adjustments (e.g. reduced hours or lighter duties), you should:

- discuss options with the employee

- consider a phased return to work

What This Means for Care Providers

In care settings:

- frequent short-term absences are common

- long-term absences require proper documentation

You must balance:

- compliance

- operational needs

You cannot withhold SSP just because a fit note arrives late, unless there is no valid reason for the delay.

Practical Tip

Create a simple policy:

- Day 1–7 → self-certification

- Day 8+ → fit note required

This keeps your process consistent across all caregivers and reduces disputes.

READ: What is the Health and Safety at Work Act 1974?

SSP vs NHS Sick Pay vs Private Sick Pay

Not all sick pay works the same. As a caregiver business, you must understand the difference between SSP, NHS sick pay, and private sick pay so you can set the right expectations for your staff.

What Is SSP?

Statutory Sick Pay (SSP) is the legal minimum you must pay eligible employees:

- £123.25 per week (2026 rate)

- Paid for up to 28 weeks

- Funded entirely by the employer

This applies to most private care providers.

What Is NHS Sick Pay?

NHS sick pay is a contractual scheme, not a legal minimum.

It typically offers:

- Full pay for a set period

- Then half pay

- Based on length of service

NHS staff receive significantly more support than SSP alone.

This creates a gap in expectations, especially when caregivers move from NHS roles into private care.

What Is Private Sick Pay?

Private sick pay (also called contractual or occupational sick pay) is:

- Set by the employer

- Defined in the employment contract

- Paid on top of, or instead of, SSP

Examples include:

- Full pay for 2–4 weeks

- Then SSP only

- Or tiered systems (full → half → SSP)

You can offer more than SSP—but never less.

Why This Matters for Caregiver Businesses

Many caregivers compare benefits across employers.

If you only offer SSP:

- staff may feel under-supported

- retention may suffer

If you offer private sick pay:

- you improve staff loyalty

- reduce presenteeism (working while sick)

- strengthen your employer brand

Practical Tip

Review your sick pay structure regularly.

Even a small top-up above SSP can:

- improve retention

- reduce burnout

- make your business more competitive

In a staffing-sensitive sector like care, this can make a real difference.

SEE MORE: What is an SR1 Form? 2026 Guide for UK Care Providers

Why Is SSP So Low?

Many care providers and caregivers ask the same question: why is SSP so low compared to real living costs?

The answer is simple, SSP is designed as a minimum legal safety net, not a full income replacement.

SSP Is a Baseline, Not Full Pay

The government sets SSP at a fixed rate to:

- ensure employers provide basic financial support

- keep costs predictable for businesses

- avoid placing full wage liability on employers

At £123.25 per week, SSP does not aim to cover normal living expenses.

Impact on Care Workers

For many caregivers:

- pay is already modest

- shifts vary

- overtime is common

When sickness occurs, income can drop sharply.

This creates:

- financial stress

- pressure to return to work early

- higher risk of presenteeism (working while unwell)

Impact on Caregiver Businesses

Low SSP can also affect your business:

- Staff may return too early → quality of care risk

- Morale may drop → retention issues

- Absence patterns may become inconsistent

SSP levels indirectly influence staff behaviour and service delivery

Why Employers Often Top It Up

Many care providers introduce private sick pay to:

- support staff financially

- reduce early returns to work

- improve retention

Even a small enhancement can:

- stabilise your workforce

- improve care continuity

Practical Perspective

SSP works as a legal minimum, not a competitive benefit.

If you rely on SSP alone, you meet the law, but you may fall behind as an employer.

Caregiver businesses that understand this tend to:

- plan for absence costs

- design better sick pay policies

- build stronger, more reliable teams

Practical Tips for Care Providers

Managing SSP effectively is not just about compliance, it’s about protecting your operations, your staff, and your margins.

1. Standardise Your SSP Process

Create a simple, repeatable system:

- Track sickness from day one

- Confirm eligibility before payment

- Use a consistent SSP calculator UK method for all staff

This reduces errors, especially in large caregiver teams.

2. Plan for Long-Term Sick Pay

Care businesses often face extended absences.

- Monitor staff approaching 28 weeks of SSP

- Prepare to issue the SSP1 form early

- Plan cover for long-term cases

Proactive planning avoids disruption to client care.

3. Use Accurate Records

Keep clear records of:

- sickness dates

- qualifying days

- SSP payments

HMRC may request this if disputes arise.

4. Review Your Sick Pay Policy

Relying only on SSP may not be enough.

Consider:

- adding private sick pay

- offering short-term top-ups

Even small enhancements can improve retention and reduce absenteeism.

5. Train Your Admin or HR Team

Make sure your team understands:

- SSP entitlement rules

- calculation methods

- when to request fit notes

This ensures consistent application across all caregivers.

6. Think Operationally, Not Just Legally

In care, absence affects real people.

When a caregiver is off sick:

- clients still need support

- schedules must adjust quickly

Build a system that balances:

- compliance

- cost control

- continuity of care

Final Tip…

Do not treat SSP as just a payroll task. Treat it as part of your workforce strategy, because in a caregiver business, staffing stability directly affects care quality.

Here are stronger, higher-converting CTA options tailored to your article (SSP + caregiver business angle).

These are designed to feel less generic, more authoritative, and action-driven

Take control of sick pay, compliance, and staffing with confidence.

Care Sync Experts helps caregiver businesses simplify SSP calculations, stay compliant with 2026 regulations, and build stronger workforce systems that reduce risk and improve care delivery.

Speak to our team today and get your sick pay strategy right from day one.

FAQ

What is SSP in UK payroll?

SSP (Statutory Sick Pay) is the legal minimum sick pay employers must provide to eligible employees who are off work due to illness.

In UK payroll:

SSP is processed through PAYE, just like wages

Employers are responsible for paying it (not HMRC)

It is subject to tax and National Insurance deductions

For caregiver businesses, SSP becomes part of your regular payroll obligations, not a separate benefit system.

What is an example of SSP?

Here’s a simple example for a care worker:

Weekly SSP rate: £123.25

Employee works: 5 days per week

Daily SSP rate: £24.65

If the employee is off sick for 3 qualifying days, you pay:

£24.65 × 3 = £73.95 SSP

This amount is:

paid through payroll

taxed like normal earnings

How to calculate absence rate in the UK?

Caregiver businesses often track absence rates to manage staffing.

Use this simple formula: Absence Rate (%) = (Total days absent ÷ Total available working days) × 100

Example:

10 employees

Each works 5 days per week → 50 total working days

5 days lost to sickness

(5 ÷ 50) × 100 = 10% absence rate

Tracking this helps you:

identify trends

plan staffing

control long-term sick pay costs

How many sick days per year is acceptable in the UK?

There is no fixed legal limit on how many sick days are “acceptable” in the UK.

However, many employers use internal benchmarks:

Short-term absence: 3–5 days per year (typical range)

Trigger points: Often set around 3–4 separate absences

For care providers:

even a few sick days can disrupt service delivery

consistency matters more than averages

The best approach is to:

set clear absence policies

monitor patterns

support staff early to prevent long-term issues