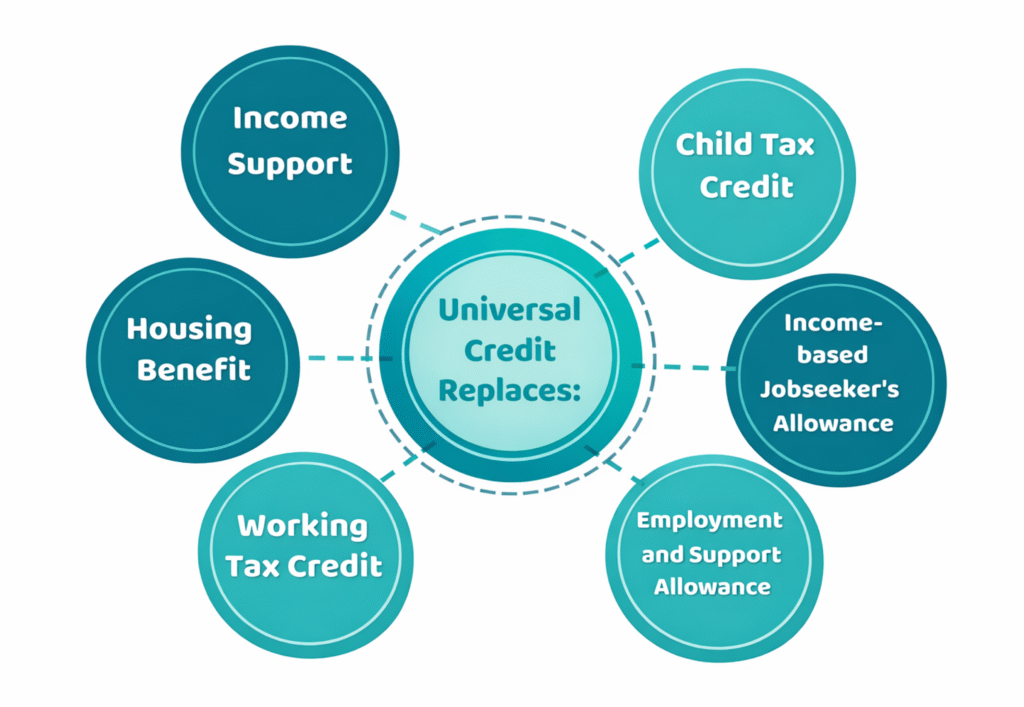

The carers element Universal Credit is an extra monthly payment added to your Universal Credit award if you spend at least 35 hours a week caring for a disabled person. For the 2025–2026 financial year, the universal credit carer element is worth £201.68 per month and is paid as part of your regular Universal Credit calculation.

You do not need to claim Carer’s Allowance to receive the carers element, and there is no specific earnings limit attached to it. However, because it forms part of Universal Credit, the final amount you receive will still depend on your household income and other elements included in your claim.

To qualify for the carers element Universal Credit 2026, the person you care for must receive a qualifying disability benefit, such as the daily living component of Personal Independence Payment (PIP), Disability Living Allowance care component, Attendance Allowance, or Armed Forces Independence Payment.

If you meet the caring requirements and report your role to the Department for Work and Pensions (DWP), the payment can be added to your Universal Credit award to provide extra financial support for your caring responsibilities.

Carers Element Universal Credit Eligibility: Who Can Claim?

You may qualify for the carers element Universal Credit if you have regular and substantial caring responsibilities for someone with a disability. The Department for Work and Pensions (DWP) adds this carers element to your Universal Credit award when you meet several key conditions.

To meet the Carers Element Universal Credit eligibility rules, you must:

- Be 16 years old or over

- Provide at least 35 hours of care each week

- Care for someone who receives a qualifying disability benefit

- Be claiming Universal Credit

- Not be in full-time education

You do not need to live with the person you care for, but you must show that your caring role is genuine and consistent.

Once you report your caring responsibilities, the DWP may also change your work requirements under Universal Credit. Many carers move into a “no work-related requirements” group, meaning the Jobcentre will not expect them to search for work while they provide significant care.

Because the carers element Universal Credit forms part of your overall claim, your Universal Credit work allowance and household income can still affect the final amount you receive each month.

RELATED: Attendance Allowance Pitfalls (2026): Best Guide to Claim AA Successfully

Which Disability Benefits Qualify for the Carers Element?

To receive the universal credit carer element, the person you care for must already receive a qualifying disability benefit. The Department for Work and Pensions uses these benefits as proof that the person needs substantial care.

The Carers Element Universal Credit eligibility usually requires the person you support to receive one of the following:

- Personal Independence Payment (PIP) – daily living component

- Disability Living Allowance (DLA) – middle or highest rate care component

- Attendance Allowance

- Armed Forces Independence Payment

If the person you care for receives one of these benefits, you can report your caring responsibilities in your Universal Credit account so the carers element Universal Credit can be added to your claim.

If you care for a disabled child, your Universal Credit award may already include the child element Universal Credit or the disabled child element Universal Credit. In this situation, you may still qualify for the carers element if you personally provide at least 35 hours of care each week.

Many families caring for disabled children receive multiple Universal Credit elements, which can significantly increase the total support available each month.

How to Apply for Carers Element of Universal Credit

You do not submit a separate application to receive the carers element Universal Credit. Instead, you must report your caring responsibilities directly in your Universal Credit account.

To apply for carers element of Universal Credit, follow these steps:

- Log in to your Universal Credit online account.

- Open your journal and report that you provide care for someone.

- Provide details about the person you care for, including:

- Their name and date of birth

- Their National Insurance number (if known)

- The disability benefit they receive

- The number of hours you provide care each week

Once you report this information, the Department for Work and Pensions (DWP) will review your circumstances. If you meet the conditions, they will add the carers element to your Universal Credit award during your next assessment period.

It is important to report your caring role as soon as possible. The DWP does not automatically know you are a carer, even if you receive other benefits such as Carer’s Allowance, so your Universal Credit payment may stay lower until you update your claim.

READ MORE: What Is Person Centred Care? 2026 Guide

How Much Is the Universal Credit Carer Element in 2026?

The carers element Universal Credit 2026 is worth £201.68 per month for the 2025–2026 financial year. The Department for Work and Pensions (DWP) adds this amount to your Universal Credit payment if you meet the caring requirements.

This payment forms part of your maximum Universal Credit award, which includes the standard allowance and any additional elements you qualify for, such as the child element Universal Credit, housing costs element, or childcare support.

Unlike Carer’s Allowance, the universal credit carer element does not have a strict earnings limit. However, because Universal Credit is a means-tested benefit, your total household income will still affect the final amount you receive each month.

The carers element is designed to act as an extra DWP payment for low-income carers, helping support people who provide regular care while managing work or other responsibilities.

Carers Element Universal Credit and Carers Allowance: What’s the Difference?

Many carers confuse the carers element Universal Credit with Carer’s Allowance, but they are two different types of support.

The carers element Universal Credit is an extra amount added to your Universal Credit payment if you provide at least 35 hours of care each week for someone receiving a qualifying disability benefit. It does not have a fixed earnings limit, although your overall Universal Credit award will still depend on your household income.

Carer’s Allowance, on the other hand, is a separate benefit paid directly to carers. It does have an earnings limit, and the government reviews this limit each year. This often leads people to ask questions like “is Carer’s Allowance means tested?” While it is not strictly means-tested, your earnings must stay below the allowed threshold to receive it.

You can receive both the carers element Universal Credit and Carer’s Allowance at the same time. However, if you claim Carer’s Allowance, the payment will usually count as income when the DWP calculates your Universal Credit award. In practice, this means your Universal Credit may reduce slightly, but most carers still end up better off overall.

In Scotland, carers may also receive additional support through Carer’s Allowance Supplement, which increases the total support available for eligible carers.

LCWRA and Carers Element: Can You Receive Both?

You cannot receive both the carers element Universal Credit and the Limited Capability for Work and Work-Related Activity (LCWRA) element at the same time.

The LCWRA payment supports people whose health condition or disability prevents them from working. If you qualify for LCWRA, Universal Credit will normally award this element instead of the carers element, because the system only pays one of these elements at a time.

In most cases, the LCWRA rates are higher than the carers element. When someone qualifies for both, the Department for Work and Pensions automatically applies the higher payment to your claim.

Recent Universal Credit LCWRA changes have not altered this rule. The system still prioritises the higher element when calculating your final Universal Credit award.

SEE ALSO: First Person vs Third Person Care Plan: CQC and the Mental Capacity Act Expectation in 2026

Can Couples Claim the Carer Element?

Yes, couples can claim the Carer’s Element Universal Credit joint claim in certain situations. Universal Credit assesses couples as a single household, but both partners may still qualify for the carers element if they each care for a different disabled person.

For example, one partner may care for a disabled parent while the other provides support for a disabled child. If both partners provide at least 35 hours of care per week, Universal Credit can include two carers elements in the same claim.

This situation can also arise in families caring for more than one child with additional needs. If both parents provide substantial care, the claim may include both the child element Universal Credit and the carers element Universal Credit for 2 children, where the caring responsibilities apply separately.

Because Universal Credit calculates payments at the household level, the Department for Work and Pensions will review the full claim to confirm that each partner meets the caring requirements.

Can the Carers Element Universal Credit Be Backdated?

In some situations, the carers element Universal Credit backdated payment may apply if you started caring earlier but did not report it straight away.

Universal Credit usually adds the carers element from the date you report your caring responsibilities in your online journal. However, the Department for Work and Pensions may allow backdating if the person you care for only recently received their qualifying disability benefit, such as Personal Independence Payment or Attendance Allowance.

For example, if the disabled person’s benefit award is backdated, you may also be able to request that the carers element Universal Credit applies from the same date.

To avoid losing payments, carers should report their caring role as soon as possible in their Universal Credit account. This ensures the Department for Work and Pensions can assess the claim and include the additional support in the next assessment period.

MORE: Do Dementia Sufferers Have to Pay Care Home Fees in the UK? (2026 Guide)

Additional Universal Credit Payments Carers Should Know About

Carers receiving the carers element Universal Credit may also qualify for other payments depending on their household circumstances. Universal Credit combines several elements to calculate the final monthly award.

For example, families with children may receive the child element Universal Credit, while households caring for a disabled child can receive the disabled child element Universal Credit. These additional elements increase the maximum Universal Credit amount before income deductions apply.

Carers should also watch for temporary government support such as the cost of living payment 2024/25 Universal Credit, which the government provides to many low-income households during periods of rising living costs. In previous years, the government also issued one-off payments like the Universal Credit £325 payment to support claimants.

Your Universal Credit work allowance may also apply if you work while claiming Universal Credit. This allowance lets you earn a certain amount before your Universal Credit payment starts to reduce.

Together, these elements and temporary payments can significantly increase the overall support available to low-income households caring for someone with a disability.

Key Takeaways for Carers Claiming Universal Credit

- The carers element Universal Credit provides an extra £201.68 per month for people who care for someone for at least 35 hours a week.

- You do not need to claim Carer’s Allowance to receive the universal credit carer element.

- The person you care for must receive a qualifying disability benefit such as PIP daily living, DLA care component, or Attendance Allowance.

- You must report your caring responsibilities in your Universal Credit journal for the payment to be added to your claim.

- You cannot receive both the carers element and the LCWRA element at the same time — Universal Credit will apply the higher payment.

- In some cases, the carers element Universal Credit backdated payment may apply if the disabled person’s benefit is awarded retrospectively.

- Couples may both receive the carer’s element Universal Credit joint claim if each partner cares for a different disabled person.

Final Thoughts…

Providing regular care for someone with a disability can be demanding, both emotionally and financially. The carers element Universal Credit exists to recognise that commitment and provide additional support to people who dedicate significant time to caring for others.

However, many carers miss out on this payment simply because they do not realise they qualify or they do not report their caring responsibilities correctly in their Universal Credit claim. Understanding the rules around eligibility, backdating, and how the carers element interacts with other benefits can make a real difference to the amount of support you receive.

If you are supporting someone with a disability and feel unsure about Universal Credit elements, caring requirements, or how to report your role correctly, Care Sync Experts can help.

We work with carers and families to clarify benefit eligibility, explain Universal Credit rules in plain language, and help you understand the support available so you can avoid common mistakes that delay payments or reduce the financial help you may be entitled to.

FAQ

What can I claim if I am a carer?

If you care for someone with a disability, you may qualify for several types of financial support depending on your circumstances. Many carers receive the carers element Universal Credit, which adds an extra monthly amount to their Universal Credit payment if they provide at least 35 hours of care per week.

You may also qualify for Carer’s Allowance, which is a separate benefit paid to carers who meet the earnings and caring requirements. Some carers can receive both benefits at the same time, although Carer’s Allowance usually counts as income when Universal Credit is calculated.

Other support may include the child element Universal Credit, the disabled child element Universal Credit, housing support, and occasional government payments for low-income households.

Is carers element extra money?

Yes. The carers element is extra money added to your Universal Credit payment if you provide substantial care for someone with a disability.

It increases the maximum Universal Credit amount your household can receive before income deductions apply.

The Department for Work and Pensions includes this element alongside other Universal Credit components such as the standard allowance, child element, or housing costs element.

Because Universal Credit is means-tested, the final amount you receive will still depend on your income, savings, and household circumstances.

How many people can claim the carers element?

More than one person can receive the carers element Universal Credit, but each person must care for a different disabled individual.

For example, in a couple’s Universal Credit claim, both partners may qualify for the carer’s element Universal Credit joint claim if they each provide at least 35 hours of care per week for separate people who receive qualifying disability benefits.

However, only one person can claim caring support for the same disabled person at a time.

Will claiming carers element affect my Universal Credit?

Claiming the carers element Universal Credit usually increases the maximum amount you can receive each month because it adds an additional element to your claim.

However, your total Universal Credit payment still depends on factors such as household income, savings, and other elements included in your award. If you already receive certain elements, such as LCWRA, the system may apply the higher element instead of the carers element when calculating your payment.

In most cases, adding the carers element results in more financial support for people with significant caring responsibilities.